重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

更多“When a business makes a profit as shown by the statement of profit or loss, the profit figure is deb…”相关的问题

更多“When a business makes a profit as shown by the statement of profit or loss, the profit figure is deb…”相关的问题

第2题

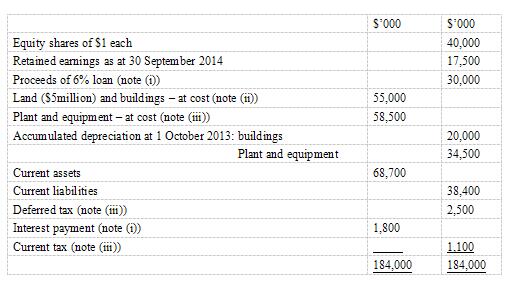

After preparing a draft statement of profit or loss for the year ended 30 September 2014 and adding the year’s profit (before any adjustments required by notes (i) to (iii) below) to retained earnings, Kandy as at 30 September 2014 is:

The following notes are relevant:

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(ii)Non-current assets: The price of property has increased significantly in recent years and on 1 October 2013, the directors decided to revalue the land and buildings. The directors accepted the report of an independent surveyor who valued the land at $8 million and the buildings at $39 million on that date. The remaining life of the buildings at 1 October 2013 was 15 years. Kandy does not make an annual transfer to retained profits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate of Kandy is 20%.

Plant and equipment is depreciated at 121?2% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current asset for the year ended 30 September 2014.

(iii)A provision of $2·4 million is required for current income tax on the profit of the year to 30 September 2014. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), Kandy has further taxable temporary differences of $10 million as at 30 September 2014.

Required:

(a) Prepare a schedule of adjustments required to the retained earnings of Kandy as at 30 September 2014 as a result of the information in notes (i) to (iii) above.

(b) Prepare the statement of financial position of Kandy as at 30 September 2014.

第3题

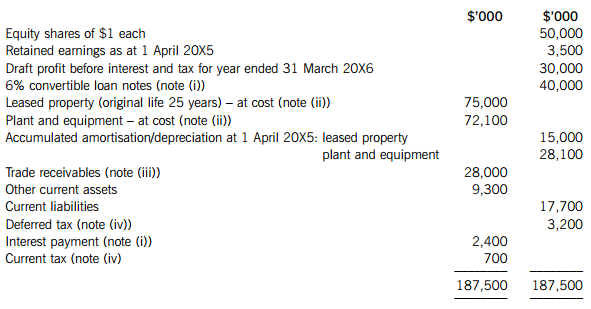

The following notes are relevant:

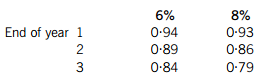

(i) Triage Co issued 400,000 $100 6% convertible loan notes on 1 April 20X5. Interest is payable annually in arrears on 31 March each year. The loans can be converted to equity shares on the basis of 20 shares for each $100 loan note on 31 March 20X8 or redeemed at par for cash on the same date. An equivalent loan without the conversion rights would have required an interest rate of 8%.

The present value of $1 receivable at the end of each year, based on discount rates of 6% and 8%, are:

(ii) Non-current assets:

The directors decided to revalue the leased property at $66·3m on 1 October 20X5. Triage Co does not make an annual transfer from the revaluation surplus to retained earnings to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability at the company’s tax rate of 20%.

The leased property is depreciated on a straight-line basis and plant and equipment at 15% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current assets for the year ended 31 March 20X6.

(iii) In September 20X5, the directors of Triage Co discovered a fraud. In total, $700,000 which had been included as receivables in the above trial balance had been stolen by an employee. $450,000 of this related to the year ended 31 March 20X5, the rest to the current year. The directors are hopeful that 50% of the losses can be recovered from the company’s insurers.

(iv) A provision of $2·7m is required for current income tax on the profit of the year to 31 March 20X6. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), at 31 March 20X6, the carrying amounts of Triage Co’s net assets are $12m more than their tax base.

Required:

(a) Prepare a schedule of adjustments required to the draft profit before interest and tax (in the above trial balance) to give the profit or loss of Triage Co for the year ended 31 March 20X6 as a result of the information in notes (i) to (iv) above.

(b) Prepare the statement of financial position of Triage Co as at 31 March 20X6.

(c) The issue of convertible loan notes can potentially dilute the basic earnings per share (EPS). Calculate the diluted earnings per share for Triage Co for the year ended 31 March 20X6 (there is no need to calculate the basic EPS).

Note: A statement of changes in equity and the notes to the statement of financial position are not required.

The following mark allocation is provided as guidance for this question:

(a) 5 marks

(b) 12 marks

(c) 3 marks

第4题

found that $18,000 paid for the purchase of a motor van had been debited to motor expenses account. It is the

company’s policy to depreciate motor vans at 25 per cent per year, with a full year’s charge in the year of acquisition.

What would the net profit be after adjusting for this error?

A $106,100

B $70,100

C $97,100

D $101,600

第5题

The trainee accountant at Judd Co has forgotten to make an accrual for rent for December in the financial statements for the year ended 31 December 20X2. Rent is charged in arrears at the end of February, May, August and November each year. The bill payable in February is expected to be $30,000. Judd Co’s draft statement of profit or loss shows a profit of $25,000 and draft statement of financial position shows net assets of $275,000. What is the profit or loss for the year and what is the net asset position after the accrual has been included in the financial statements?

A、Profit for the year Net asset position $15,000 $265,000

B、Profit for the year Net asset position $15,000 $285,000

C、Profit for the year Net asset position $35,000 $265,000

D、Profit for the year Net asset position $35,000 $285,000

第6题

Required:

(a) (i) Describe the current presentation requirements relating to the statement of profit or loss and other comprehensive income. (4 marks)

(ii) Discuss, with examples, the nature of a reclassification adjustment and the arguments for and against allowing reclassification of items to profit or loss. Note: A brief reference should be made in your answer to the IASB’s Discussion Paper on the Conceptual Framework. (5 marks)

(iii) Discuss the principles and key components of the IIRC’s Framework, and any concerns which could question the Framework’s suitability for assessing the prospects of an entity. (8 marks)

(b) Cloud, a public limited company, regularly purchases steel from a foreign supplier and designates a future purchase of steel as a hedged item in a cash flow hedge. The steel was purchased on 1 May 2014 and at that date, a cumulative gain on the hedging instrument of $3 million had been credited to other comprehensive income. At the year end of 30 April 2015, the carrying amount of the steel was $8 million and its net realisable value was $6 million. The steel was finally sold on 3 June 2015 for $6·2 million.

On a separate issue, Cloud purchased an item of property, plant and equipment for $10 million on 1 May 2013. The asset is depreciated over five years on the straight line basis with no residual value. At 30 April 2014, the asset was revalued to $12 million. At 30 April 2015, the asset’s value has fallen to $4 million. The entity makes a transfer from revaluation surplus to retained earnings for excess depreciation, as the asset is used.

Required:

Show how the above transactions would be dealt with in the financial statements of Cloud from the date of the purchase of the assets.

Note: Candidates should ignore any deferred taxation effects. (6 marks)

Professional marks will be awarded in question 4 for clarity and quality of presentation. (2 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!