重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

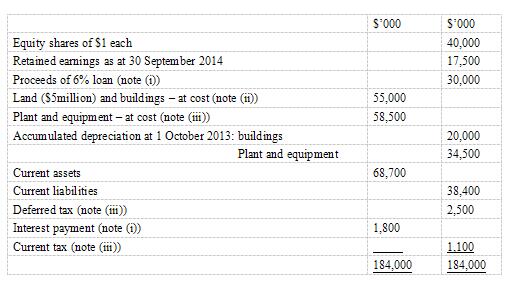

s for the year ended 30 September 2014 and adding the year’s profit (before any adjustments required by notes (i) to (iii) below) to retained earnings, Kandy as at 30 September 2014 is:

The following notes are relevant:

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(ii)Non-current assets: The price of property has increased significantly in recent years and on 1 October 2013, the directors decided to revalue the land and buildings. The directors accepted the report of an independent surveyor who valued the land at $8 million and the buildings at $39 million on that date. The remaining life of the buildings at 1 October 2013 was 15 years. Kandy does not make an annual transfer to retained profits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate of Kandy is 20%.

Plant and equipment is depreciated at 121⁄2% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current asset for the year ended 30 September 2014.

(iii)A provision of $2·4 million is required for current income tax on the profit of the year to 30 September 2014. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), Kandy has further taxable temporary differences of $10 million as at 30 September 2014.

Required:

(a) Prepare a schedule of adjustments required to the retained earnings of Kandy as at 30 September 2014 as a result of the information in notes (i) to (iii) above.

(b) Prepare the statement of financial position of Kandy as at 30 September 2014.

更多“After preparing a draft statement of profit or los”相关的问题

更多“After preparing a draft statement of profit or los”相关的问题

第1题

A.Innovation to improve network performance.

B.Ideas are brought from outside and integrated with the company's own advantage.

C.It is based on the ground that not all good ideas come from home.

D.It involves cultivating contacts with start-ups and academic researchers.

第2题

A. Company A will report higher asset balances related to the facilities under construction.

B. The companies will report the same asset balances related to the facilities under construction.

C. Company A’s interest coverage ratio will be lower than it would have been if the company had expensed all interest.

第3题

A.Company A will report higher asset balances related to the facilities under construction.

B.The companies will report the same asset balances related to the facilities under construction.

C.Company A’s interest coverage ratio will be lower than it would have been if the company had expensed all interest.

第4题

Which of the following accounting treatments would be an example of faithful representation?

A、Charging the rental payments for an item of plant to the statement of profit or loss where the rental agreement meets the criteria for a lease

B、Including a convertible loan note in equity on the basis that the holders are likely to choose the equity option on conversion

C、Treating redeemable preference shares as part of equity in the statement of financial position

D、Derecognising factored trade receivables sold without recourse to the seller

第5题

outcomes of the secrecy/licensing decision to shareholders. Once the board has decided which one to pursue,

the relevant draft will be included in a voluntary section of the next corporate annual report.

Required:

(i) Draft a statement in the event that the board chooses the secrecy option. It should make a convincing

business case and put forward ethical arguments for the secrecy option. The ethical arguments should

be made from the stockholder (or pristine capitalist) perspective. (8 marks)

(ii) Draft a statement in the event that the board chooses the licensing option. It should make a convincing

business case and put forward ethical arguments for the licensing option. The ethical arguments should

be made from the wider stakeholder perspective. (8 marks)

(iii) Professional marks for the persuasiveness and logical flow of arguments: two marks per statement.

(4 marks)

第6题

A.Thin people could never find themselves having enough time for leisure.

B.Thin people are seldom unable to find themselves having nothing to do.

C.Thin people are never lazy in doing things useful.

D.Thin people are fussily annoying and particularly disgusting.

第7题

A.Thin people could never find themselves having enough time for leisure.

B.Thin people are seldom unable to find themselves having nothing to do.

C.Thin people are never lazy in doing things useful.

D.Thin people are fussily annoying and particularly disgusting.

第8题

A.The directors of large firms will continue to anticipate the demand for products.

B.The directors of large firms are less interested in achieving a predictable level of profit than in achieving a large profit.

C.The directors of large firms will strive to reduce the costs of their products.

D.Many directors of large firms believe that the government should establish the prices that will be charged for products.

第9题

A.The directors of large firms will continue to anticipate the demand for products.

B.The directors of large firms are less interested in achieving a predictable level of profit than in achieving a large profit.

C.The directors of large firms will strive to reduce the costs of their products.

D.Many directors of large firms believe that the government should establish the prices that will be charged for products.

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!