重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

Section A – This ONE question is compulsory and MUST be attempted

Cocoa-Mocha-Chai (CMC) Co is a large listed company based in Switzerland and uses Swiss Francs as its currency. It imports tea, coffee and cocoa from countries around the world, and sells its blended products to supermarkets and large retailers worldwide. The company has production facilities located in two European ports where raw materials are brought for processing, and from where finished products are shipped out. All raw material purchases are paid for in US dollars (US$), while all sales are invoiced in Swiss Francs (CHF).

Until recently CMC Co had no intention of hedging its foreign currency exposures, interest rate exposures or commodity price fluctuations, and stated this intent in its annual report. However, after consultations with senior and middle managers, the company’s new Board of Directors (BoD) has been reviewing its risk management and operations strategies.

The following two proposals have been put forward by the BoD for further consideration:

Proposal one

Setting up a treasury function to manage the foreign currency and interest rate exposures (but not commodity price fluctuations) using derivative products. The treasury function would be headed by the finance director. The purchasing director, who initiated the idea of having a treasury function, was of the opinion that this would enable her management team to make better decisions. The finance director also supported the idea as he felt this would increase his influence on the BoD and strengthen his case for an increase in his remuneration.

In order to assist in the further consideration of this proposal, the BoD wants you to use the following upcoming foreign currency and interest rate exposures to demonstrate how they would be managed by the treasury function:

(i) a payment of US$5,060,000 which is due in four months’ time; and

(ii) a four-year CHF60,000,000 loan taken out to part-fund the setting up of four branches (see proposal two below). Interest will be payable on the loan at a fixed annual rate of 2·2% or a floating annual rate based on the yield curve rate plus 0·40%. The loan’s principal amount will be repayable in full at the end of the fourth year.

Proposal two

This proposal suggested setting up four new branches in four different countries. Each branch would have its own production facilities and sales teams. As a consequence of this, one of the two European-based production facilities will be closed. Initial cost-benefit analysis indicated that this would reduce costs related to production, distribution and logistics, as these branches would be closer to the sources of raw materials and also to the customers. The operations and sales directors supported the proposal, as in addition to above, this would enable sales and marketing teams in the branches to respond to any changes in nearby markets more quickly. The branches would be controlled and staffed by the local population in those countries. However, some members of the BoD expressed concern that such a move would create agency issues between CMC Co’s central management and the management controlling the branches. They suggested mitigation strategies would need to be established to minimise these issues.

Response from the non-executive directors

When the proposals were put to the non-executive directors, they indicated that they were broadly supportive of the second proposal if the financial benefits outweigh the costs of setting up and running the four branches. However, they felt that they could not support the first proposal, as this would reduce shareholder value because the costs related to undertaking the proposal are likely to outweigh the benefits.

Additional information relating to proposal one

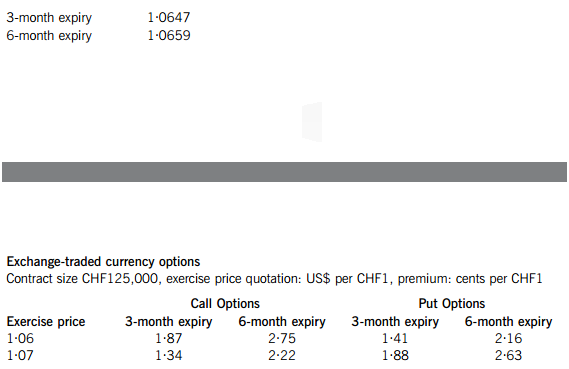

The current spot rate is US$1·0635 per CHF1. The current annual inflation rate in the USA is three times higher than Switzerland.

The following derivative products are available to CMC Co to manage the exposures of the US$ payment and the interest on the loan:

Exchange-traded currency futures

Contract size CHF125,000 price quotation: US$ per CHF1

It can be assumed that futures and option contracts expire at the end of the month and transaction costs related to these can be ignored.

Over-the-counter products

In addition to the exchange-traded products, Pecunia Bank is willing to offer the following over-the-counter derivative products to CMC Co:

(i) A forward rate between the US$ and the CHF of US$ 1·0677 per CHF1.

(ii) An interest rate swap contract with a counterparty, where the counterparty can borrow at an annual floating rate based on the yield curve rate plus 0·8% or an annual fixed rate of 3·8%. Pecunia Bank would charge a fee of 20 basis points each to act as the intermediary of the swap. Both parties will benefit equally from the swap contract.

Required:

(a) Advise CMC Co on an appropriate hedging strategy to manage the foreign exchange exposure of the US$ payment in four months’ time. Show all relevant calculations, including the number of contracts bought or sold in the exchange-traded derivative markets. (15 marks)

(b) Demonstrate how CMC Co could benefit from the swap offered by Pecunia Bank. (6 marks)

(c) As an alternative to paying the principal on the loan as one lump sum at the end of the fourth year, CMC Co could pay off the loan in equal annual amounts over the four years similar to an annuity. In this case, an annual interest rate of 2% would be payable, which is the same as the loan’s gross redemption yield (yield to maturity).

Required: Calculate the modified duration of the loan if it is repaid in equal amounts and explain how duration can be used to measure the sensitivity of the loan to changes in interest rates. (7 marks)

(d) Prepare a memorandum for the Board of Directors (BoD) of CMC Co which:

(i) Discusses proposal one in light of the concerns raised by the non-executive directors; and (9 marks)

(ii) Discusses the agency issues related to proposal two and how these can be mitigated. (9 marks)

Professional marks will be awarded in part (d) for the presentation, structure, logical flow and clarity of the memorandum. (4 marks)

更多“Section A – This ONE question is compulsory and MUST be attemptedCocoa-Mocha-Chai (CMC) Co”相关的问题

更多“Section A – This ONE question is compulsory and MUST be attemptedCocoa-Mocha-Chai (CMC) Co”相关的问题

第1题

ories throughout Europe. It sells its own-brand items, which are produced by small manufacturers located in Africa, who work solely for Strom Co. The recent European sovereign debt crisis has affected a number of countries in the European Union (EU). Consequently, Strom Co has found trading conditions to be extremely difficult, putting pressure on profits and sales revenue.

The sovereign debt crisis in Europe resulted in countries finding it increasingly difficult and expensive to issue government bonds to raise funds. Two main reasons have been put forward to explain why the crisis took place: firstly, a number of countries continued to borrow excessive funds, because their expenditure exceeded taxation revenues; and secondly, a number of countries allocated significant sums of money to support their banks following the ‘credit crunch’ and the banking crisis.

In order to prevent countries defaulting on their debt obligations and being downgraded, the countries in the EU and the International Monetary Fund (IMF) established a fund to provide financial support to member states threatened by the risk of default, credit downgrades and excessive borrowing yields. Strict economic conditions known as austerity measures were imposed on these countries in exchange for receiving financial support.

The austerity measures have affected Strom Co negatively, and the years 2011 and 2012 have been particularly bad, with sales revenue declining by 15% and profits by 25% in 2011, and remaining at 2011 levels in 2012. On investigation, Strom Co noted that clothing retailers selling clothes at low prices and at high prices were not affected as badly as Strom Co or other mid-price retailers. Indeed, the retailers selling low-priced clothes had increased their profits, and retailers selling luxury, expensive clothes had maintained their profits over the last two to three years.

In order to improve profitability, Strom Co’s board of directors expects to cut costs where possible. A significant fixed cost relates to quality control, which includes monitoring the working conditions of employees of Strom Co’s clothing manufacturers, as part of its ethical commitment.

Required:

(a) Explain the role and aims of the International Monetary Fund (IMF) and discuss possible reasons why the austerity measures imposed on European Union (EU) countries might have affected Strom Co negatively. (10 marks)

(b) Suggest, giving reasons, why the austerity measures might not have affected clothing retailers at the high and low price range, as much as the mid-price range retailers like Strom Co. (4 marks)

(c) Discuss the risks to Strom Co of reducing the costs relating to quality control and how the detrimental impact of such reductions in costs could be decreased. (6 marks)

第2题

nt centres. It sets investment limits for each department based on a three-year cycle. Projects selected by departments would have to fall within the investment limits set for each of the three years. All departments would be required to maintain a capital investment monitoring system, and report on their findings annually to Arbore Co’s board of directors.

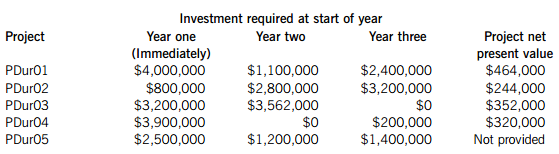

The Durvo department is considering the following five investment projects with three years of initial investment expenditure, followed by several years of positive cash inflows. The department’s initial investment expenditure limits are $9,000,000, $6,000,000 and $5,000,000 for years one, two and three respectively. None of the projects can be deferred and all projects can be scaled down but not scaled up.

PDur05 project’s annual operating cash flows commence at the end of year four and last for a period of 15 years. The project generates annual sales of 300,000 units at a selling price of $14 per unit and incurs total annual relevant costs of $3,230,000. Although the costs and units sold of the project can be predicted with a fair degree of certainty, there is considerable uncertainty about the unit selling price. The department uses a required rate of return of 11% for its projects, and inflation can be ignored.

The Durvo department’s managing director is of the opinion that all projects which return a positive net present value should be accepted and does not understand the reason(s) why Arbore Co imposes capital rationing on its departments. Furthermore, she is not sure why maintaining a capital investment monitoring system would be beneficial to the company.

Required:

(a) Calculate the net present value of project PDur05. Calculate and comment on what percentage fall in the selling price would need to occur before the net present value falls to zero. (6 marks)

(b) Formulate an appropriate capital rationing model, based on the above investment limits, that maximises the net present value for department Durvo. Finding a solution for the model is not required. (3 marks)

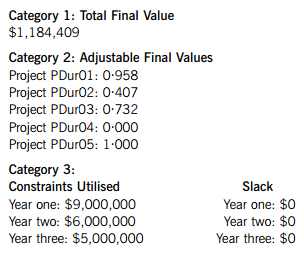

(c) Assume the following output is produced when the capital rationing model in part (b) above is solved:

Required:

Explain the figures produced in each of the three output categories. (5 marks)

(d) Provide a brief response to the managing director’s opinions by:

(i) Explaining why Arbore Co may want to impose capital rationing on its departments; (2 marks)

(ii) Explaining the features of a capital investment monitoring system and discussing the benefits of maintaining such a system. (4 marks)

第3题

Section B – TWO questions ONLY to be attempted

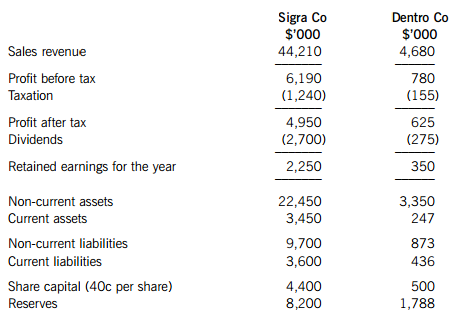

Sigra Co is a listed company producing confectionary products which it sells around the world. It wants to acquire Dentro Co, an unlisted company producing high quality, luxury chocolates. Sigra Co proposes to pay for the acquisition using one of the following three methods:

Method 1

A cash offer of $5·00 per Dentro Co share; or

Method 2

An offer of three of its shares for two of Dentro Co’s shares; or

Method 3

An offer of a 2% coupon bond in exchange for 16 Dentro Co’s shares. The bond will be redeemed in three years at its par value of $100.

Extracts from the latest financial statements of both companies are as follows:

Sigra Co’s current share price is $3·60 per share and it has estimated that Dentro Co’s price to earnings ratio is 12·5% higher than Sigra Co’s current price to earnings ratio. Sigra Co’s non-current liabilities include a 6% bond redeemable in three years at par which is currently trading at $104 per $100 par value.

Sigra Co estimates that it could achieve synergy savings of 30% of Dentro Co’s estimated equity value by eliminating duplicated administrative functions, selling excess non-current assets and through reducing the workforce numbers, if the acquisition were successful.

Required:

(a) Estimate the percentage gain on a Dentro Co share under each of the above three payment methods. Comment on the answers obtained. (16 marks)

(b) In relation to the acquisition, the board of directors of Sigra Co are considering the following two proposals:

Proposal 1 Once Sigra Co has obtained agreement from a significant majority of the shareholders, it will enforce the remaining minority shareholders to sell their shares; and

Proposal 2 Sigra Co will offer an extra 3 cents per share, in addition to the bid price, to 30% of the shareholders of Dentro Co on a first-come, first-serve basis, as an added incentive to make the acquisition proceed more quickly.

Required:

With reference to the key aspects of the global regulatory framework for mergers and acquisitions, briefly discuss the above proposals. (4 marks)

第4题

fferent markets around the world. Although its main manufacturing base is in France and it uses the Euro (€) as its base currency, it also has a few subsidiary companies around the world. Lignum Co’s treasury division is considering how to approach the following three cases of foreign exchange exposure that it faces.

Case One

Lignum Co regularly trades with companies based in Zuhait, a small country in South America whose currency is the Zupesos (ZP). It recently sold machinery for ZP140 million, which it is about to deliver to a company based there. It is expecting full payment for the machinery in four months. Although there are no exchange traded derivative products available for the Zupesos, Medes Bank has offered Lignum Co a choice of two over-the-counter derivative products.

The first derivative product is an over-the-counter forward rate determined on the basis of the Zuhait base rate of 8·5% plus 25 basis points and the French base rate of 2·2% less 30 basis points.

Alternatively, with the second derivative product Lignum Co can purchase either Euro call or put options from Medes Bank at an exercise price equivalent to the current spot exchange rate of ZP142 per €1. The option premiums offered are: ZP7 per €1 for the call option or ZP5 per €1 for the put option.

The premium cost is payable in full at the commencement of the option contract. Lignum Co can borrow money at the base rate plus 150 basis points and invest money at the base rate minus 100 basis points in France.

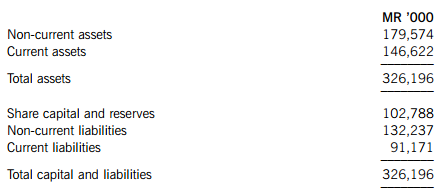

Case Two Namel Co is Lignum Co’s subsidiary company based in Maram, a small country in Asia, whose currency is the Maram Ringit (MR). The current pegged exchange rate between the Maram Ringit and the Euro is MR35 per €1. Due to economic difficulties in Maram over the last couple of years, it is very likely that the Maram Ringit will devalue by 20% imminently. Namel Co is concerned about the impact of the devaluation on its Statement of Financial Position.

Given below is an extract from the current Statement of Financial Position of Namel Co.

The current assets consist of inventories, receivables and cash. Receivables account for 40% of the current assets. All the receivables relate to sales made to Lignum Co in Euro. About 70% of the current liabilities consist of payables relating to raw material inventory purchased from Lignum Co and payable in Euro. 80% of the non-current liabilities consist of a Euro loan and the balance are borrowings sourced from financial institutions in Maram.

Case Three

Lignum Co manufactures a range of farming vehicles in France which it sells within the European Union to countries which use the Euro. Over the previous few years, it has found that its sales revenue from these products has been declining and the sales director is of the opinion that this is entirely due to the strength of the Euro. Lignum Co’s biggest competitor in these products is based in the USA and US$ rate has changed from almost parity with the Euro three years ago, to the current value of US$1·47 for €1. The agreed opinion is that the US$ will probably continue to depreciate against the Euro, but possibly at a slower rate, for the foreseeable future.

Required:

Prepare a report for Lignum Co’s treasury division that:

(i) Briefly explains the type of currency exposure Lignum Co faces for each of the above cases; (3 marks)

(ii) Recommends which of the two derivative products Lignum Co should use to manage its exposure in case one and advises on alternative hedging strategies that could be used. Show all relevant calculations; (9 marks)

(iii) Computes the gain or loss on Namel Co’s Statement of Financial Position, due to the devaluation of the Maram Ringit in case two, and discusses whether and how this exposure should be managed; (8 marks)

(iv) Discusses how the exposure in case three can be managed. (3 marks) Professional marks will be awarded in question 2 for the structure and presentation of the report. (4 marks)

第5题

Section A – BOTH questions are compulsory and MUST be attempted

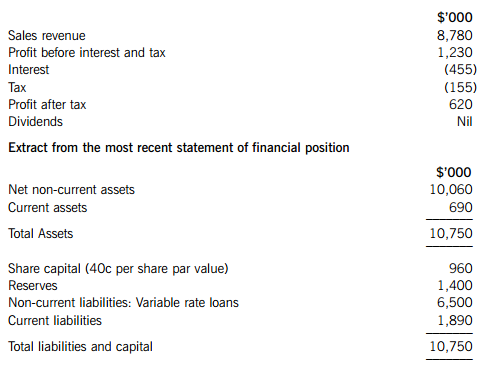

Coeden Co is a listed company operating in the hospitality and leisure industry. Coeden Co’s board of directors met recently to discuss a new strategy for the business. The proposal put forward was to sell all the hotel properties that Coeden Co owns and rent them back on a long-term rental agreement. Coeden Co would then focus solely on the provision of hotel services at these properties under its popular brand name. The proposal stated that the funds raised from the sale of the hotel properties would be used to pay off 70% of the outstanding non-current liabilities and the remaining funds would be retained for future investments.

The board of directors are of the opinion that reducing the level of debt in Coeden Co will reduce the company’s risk and therefore its cost of capital. If the proposal is undertaken and Coeden Co focuses exclusively on the provision of hotel services, it can be assumed that the current market value of equity will remain unchanged after implementing the proposal.

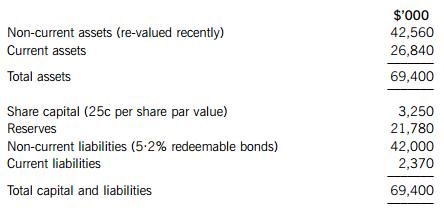

Coeden Co Financial Information

Extract from the most recent Statement of Financial Position

Coeden Co’s latest free cash flow to equity of $2,600,000 was estimated after taking into account taxation, interest and reinvestment in assets to continue with the current level of business. It can be assumed that the annual reinvestment in assets required to continue with the current level of business is equivalent to the annual amount of depreciation. Over the past few years, Coeden Co has consistently used 40% of its free cash flow to equity on new investments while distributing the remaining 60%. The market value of equity calculated on the basis of the free cash flow to equity model provides a reasonable estimate of the current market value of Coeden Co.

The bonds are redeemable at par in three years and pay the coupon on an annual basis. Although the bonds are not traded, it is estimated that Coeden Co’s current debt credit rating is BBB but would improve to A+ if the non-current liabilities are reduced by 70%.

Other Information

Coeden Co’s current equity beta is 1·1 and it can be assumed that debt beta is 0. The risk free rate is estimated to be 4% and the market risk premium is estimated to be 6%.

There is no beta available for companies offering just hotel services, since most companies own their own buildings. The average asset beta for property companies has been estimated at 0·4. It has been estimated that the hotel services business accounts for approximately 60% of the current value of Coeden Co and the property company business accounts for the remaining 40%.

Coeden Co’s corporation tax rate is 20%. The three-year borrowing credit spread on A+ rated bonds is 60 basis points and 90 basis points on BBB rated bonds, over the risk free rate of interest.

Required: (a) Calculate, and comment on, Coeden Co’s cost of equity and weighted average cost of capital before and after implementing the proposal. Briefly explain any assumptions made. (20 marks) (b) Discuss the validity of the assumption that the market value of equity will remain unchanged after the implementation of the proposal. (5 marks) (c) As an alternative to selling the hotel properties, the board of directors is considering a demerger of the hotel services and a separate property company which would own the hotel properties. The property company would take over 70% of Coeden Co’s long-term debt and pay Coeden Co cash for the balance of the property value. Required: Explain what a demerger is, and the possible benefits and drawbacks of pursuing the demerger option as opposed to selling the hotel properties. (8 marks)

第6题

are exported around the world. It is reviewing a proposal to set up a subsidiary company to manufacture a range of body and facial creams in Lanosia. These products will be sold to local retailers and to retailers in nearby countries.

Lanosia has a small but growing manufacturing industry in pharmaceutical products, although it remains largely reliant on imports. The Lanosian government has been keen to promote the pharmaceutical manufacturing industry through purchasing local pharmaceutical products, providing government grants and reducing the industry’s corporate tax rate. It also imposes large duties on imported pharmaceutical products which compete with the ones produced locally.

Although politically stable, the recent worldwide financial crisis has had a significant negative impact on Lanosia. The country’s national debt has grown substantially following a bailout of its banks and it has had to introduce economic measures which are hampering the country’s ability to recover from a deep recession. Growth in real wages has been negative over the past three years, the economy has shrunk in the past year and inflation has remained higher than normal during this time.

On the other hand, corporate investment in capital assets, research and development, and education and training, has grown recently and interest rates remain low. This has led some economists to suggest that the economy should start to recover soon. Employment levels remain high in spite of low nominal wage growth.

Lanosian corporate governance regulations stipulate that at least 40% of equity share capital must be held by the local population. In addition at least 50% of members on the Board of Directors, including the Chairman, must be from Lanosia. Kilenc Co wants to finance the subsidiary company using a mixture of debt and equity. It wants to raise additional equity and debt finance in Lanosia in order to minimise exchange rate exposure. The small size of the subsidiary will have minimal impact on Kilenc Co’s capital structure. Kilenc Co intends to raise the 40% equity through an initial public offering (IPO) in Lanosia and provide the remaining 60% of the equity funds from its own cash funds.

Required:

(a) Discuss the key risks and issues that Kilenc Co should consider when setting up a subsidiary company in Lanosia, and suggest how these may be mitigated. (15 marks)

(b) The directors of Kilenc Co have learnt that a sizeable number of equity trades in Lanosia are conducted using dark pool trading systems.

Required:

Explain what dark pool trading systems are and how Kilenc Co’s proposed Initial Public Offering (IPO) may be affected by these. (5 marks)

第7题

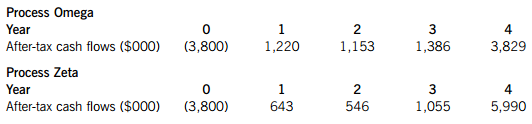

d into motor vehicle engines, will enable them to utilise fuel more efficiently. The component can be manufactured using either process Omega or process Zeta. Although this is an entirely new line of business for Tisa Co, it is of the opinion that developing either process over a period of four years and then selling the productions rights at the end of four years to another company may prove lucrative.

The annual after-tax cash flows for each process are as follows:

Tisa Co has 10 million 50c shares trading at 180c each. Its loans have a current value of $3·6 million and an average after-tax cost of debt of 4·50%. Tisa Co’s capital structure is unlikely to change significantly following the investment in either process.

Elfu Co manufactures electronic parts for cars including the production of a component similar to the one being considered by Tisa Co. Elfu Co’s equity beta is 1·40, and it is estimated that the equivalent equity beta for its other activities, excluding the component production, is 1·25. Elfu Co has 400 million 25c shares in issue trading at 120c each. Its debt finance consists of variable rate loans redeemable in seven years. The loans paying interest at base rate plus 120 basis points have a current value of $96 million. It can be assumed that 80% of Elfu Co’s debt finance and 75% of Elfu Co’s equity finance can be attributed to other activities excluding the component production.

Both companies pay annual corporation tax at a rate of 25%. The current base rate is 3·5% and the market risk premium is estimated at 5·8%.

Required:

(a) Provide a reasoned estimate of the cost of capital that Tisa Co should use to calculate the net present value of the two processes. Include all relevant calculations. (8 marks)

(b) Calculate the internal rate of return (IRR) and the modified internal rate of return (MIRR) for Process Omega. Given that the IRR and MIRR of Process Zeta are 26·6% and 23·3% respectively, recommend which process, if any, Tisa Co should proceed with and explain your recommendation. (8 marks)

(c) Elfu Co has estimated an annual standard deviation of $800,000 on one of its other projects, based on a normal distribution of returns. The average annual return on this project is $2,200,000.

Required:

Estimate the project’s Value at Risk (VAR) at a 99% confidence level for one year and over the project’s life of five years. Explain what is meant by the answers obtained. (4 marks)

第8题

Section B – TWO questions ONLY to be attempted

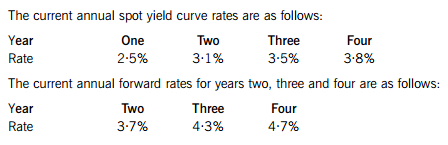

Sembilan Co, a listed company, recently issued debt finance to acquire assets in order to increase its activity levels. This debt finance is in the form. of a floating rate bond, with a face value of $320 million, redeemable in four years. The bond interest, payable annually, is based on the spot yield curve plus 60 basis points. The next annual payment is due at the end of year one.

Sembilan Co is concerned that the expected rise in interest rates over the coming few years would make it increasingly difficult to pay the interest due. It is therefore proposing to either swap the floating rate interest payment to a fixed rate payment, or to raise new equity capital and use that to pay off the floating rate bond. The new equity capital would either be issued as rights to the existing shareholders or as shares to new shareholders.

Ratus Bank has offered Sembilan Co an interest rate swap, whereby Sembilan Co would pay Ratus Bank interest based on an equivalent fixed annual rate of 3·76?% in exchange for receiving a variable amount based on the current yield curve rate. Payments and receipts will be made at the end of each year, for the next four years. Ratus Bank will charge an annual fee of 20 basis points if the swap is agreed.

Required:

(a) Based on the above information, calculate the amounts Sembilan Co expects to pay or receive every year on the swap (excluding the fee of 20 basis points). Explain why the fixed annual rate of interest of 3·76?% is less than the four-year yield curve rate of 3·8%. (6 marks)

(b) Demonstrate that Sembilan Co’s interest payment liability does not change, after it has undertaken the swap, whether the interest rates increase or decrease. (5 marks)

(c) Discuss the factors that Sembilan Co should consider when deciding whether it should raise equity capital to pay off the floating rate debt. (9 marks)

第9题

e directors of Ennea Co to discuss the future investment and financing strategy of the business. Ennea Co is a listed company operating in the haulage and shipping industry.

Proposal 1

To increase the company’s level of debt by borrowing a further $20 million and use the funds raised to buy back share capital.

Proposal 2

To increase the company’s level of debt by borrowing a further $20 million and use these funds to invest in additional non-current assets in the haulage strategic business unit.

Proposal 3

To sell excess non-current haulage assets with a net book value of $25 million for $27 million and focus on offering more services to the shipping strategic business unit. This business unit will require no additional investment in non-current assets. All the funds raised from the sale of the non-current assets will be used to reduce the company’s debt.

Ennea Co financial information

Extracts from the forecast financial position for the coming year

Ennea Co’s forecast after tax profit for the coming year is expected to be $26 million and its current share price is $3·20 per share. The non-current liabilities consist solely of a 6% medium term loan redeemable within seven years. The terms of the loan contract stipulates that an increase in borrowing will result in an increase in the coupon payable of 25 basis points on the total amount borrowed, while a reduction in borrowing will lower the coupon payable by 15 basis points on the total amount borrowed.

Ennea Co’s effective tax rate is 20%. The company’s estimated after tax rate of return on investment is expected to be 15% on any new investment. It is expected that any reduction in investment would suffer the same rate of return.

Required:

(a) Estimate and discuss the impact of each of the three proposals on the forecast statement of financial position, the earnings and earnings per share, and gearing of Ennea Co. (20 marks)

(b) An alternative suggestion to proposal three was made where the non-current assets could be leased to other companies instead of being sold. The lease receipts would then be converted into an asset through securitisation. The proceeds from the sale of the securitised lease receipts asset would be used to reduce the outstanding loan borrowings.

Required:

Explain what the securitisation process would involve and what would be the key barriers to Ennea Co undertaking the process. (5 marks)

第10题

Section A – BOTH questions are compulsory and MUST be attempted

Nente Co, an unlisted company, designs and develops tools and parts for specialist machinery. The company was formed four years ago by three friends, who own 20% of the equity capital in total, and a consortium of five business angel organisations, who own the remaining 80%, in roughly equal proportions. Nente Co also has a large amount of debt finance in the form. of variable rate loans. Initially the amount of annual interest payable on these loans was low and allowed Nente Co to invest internally generated funds to expand its business. Recently though, due to a rapid increase in interest rates, there has been limited scope for future expansion and no new product development.

The Board of Directors, consisting of the three friends and a representative from each business angel organisation, met recently to discuss how to secure the company’s future prospects. Two proposals were put forward, as follows:

Proposal 1

To accept a takeover offer from Mije Co, a listed company, which develops and manufactures specialist machinery tools and parts. The takeover offer is for $2·95 cash per share or a share-for-share exchange where two Mije Co shares would be offered for three Nente Co shares. Mije Co would need to get the final approval from its shareholders if either offer is accepted;

Proposal 2

To pursue an opportunity to develop a small prototype product that just breaks even financially, but gives the company exclusive rights to produce a follow-on product within two years.

The meeting concluded without agreement on which proposal to pursue.

After the meeting, Mije Co was consulted about the exclusive rights. Mije Co’s directors indicated that they had not considered the rights in their computations and were willing to continue with the takeover offer on the same terms without them.

Currently, Mije Co has 10 million shares in issue and these are trading for $4·80 each. Mije Co’s price to earnings (P/E) ratio is 15. It has sufficient cash to pay for Nente Co’s equity and a substantial proportion of its debt, and believes that this will enable Nente Co to operate on a P/E level of 15 as well. In addition to this, Mije Co believes that it can find cost-based synergies of $150,000 after tax per year for the foreseeable future. Mije Co’s current profit after tax is $3,200,000.

The following financial information relates to Nente Co and to the development of the new product.

Nente Co financial information

Extract from the most recent income statement

In arriving at the profit after tax amount, Nente Co deducted tax allowable depreciation and other non-cash expenses totalling $1,206,000. It requires an annual cash investment of $1,010,000 in non-current assets and working capital to continue its operations.

Nente Co’s profits before interest and tax in its first year of operation were $970,000 and have been growing steadily in each of the following three years, to their current level. Nente Co’s cash flows grew at the same rate as well, but it is likely that this growth rate will reduce to 25% of the original rate for the foreseeable future.

Nente Co currently pays interest of 7% per year on its loans, which is 380 basis points over the government base rate, and corporation tax of 20% on profits after interest. It is estimated that an overall cost of capital of 11% is reasonable compensation for the risk undertaken on an investment of this nature.

New product development (Proposal 2)

Developing the new follow-on product will require an investment of $2,500,000 initially. The total expected cash flows and present values of the product over its five-year life, with a volatility of 42% standard deviation, are as follows:

Required:

Prepare a report for the Board of Directors of Nente Co that:

(i) Estimates the current value of a Nente Co share, using the free cash flow to firm methodology; (7 marks)

(ii) Estimates the percentage gain in value to a Nente Co share and a Mije Co share under each payment offer; (8 marks)

(iii) Estimates the percentage gain in the value of the follow-on product to a Nente Co share, based on its cash flows and on the assumption that the production can be delayed following acquisition of the exclusive rights of production; (8 marks)

(iv) Discusses the likely reaction of Nente Co and Mije Co shareholders to the takeover offer, including the assumptions made in the estimates above and how the follow-on product’s value can be utilised by Nente Co. (8 marks)

Professional marks will be awarded in question 1 for the presentation, structure and clarity of the answer. (4 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!