重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

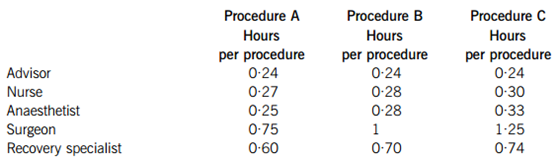

1 All patients go through a five step process, irrespective of which procedure they are having:

– step 1: consultation with the advisor;

– step 2: pre-operative injection given by the nurse;

– step 3: anaesthetic given by anaesthetist;

–step 4: procedure performed in theatre by the surgeon;

– step 5: recovery with the recovery specialist.

2 The price of each of procedures A, B and C is $2,700, $3,500 and $4,250 respectively.

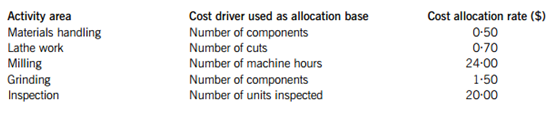

3 The only materials’ costs relating to the procedures are for the pre-operative injections given by the nurse, the anaesthetic and the dressings. These are as follows:

4 There are five members of staff employed by Thin Co. Each works a standard 40-hour week for 47 weeks of the year, a total of 1,880 hours each per annum. Their salaries are as follows:

– Advisor: $45,000 per annum;

– Nurse: $38,000 per annum;

– Anaesthetist: $75,000 per annum;

– Surgeon: $90,000 per annum;

– Recovery specialist: $50,000 per annum.

The only other hospital costs (comparable to ‘factory costs’ in a traditional manufacturing environment) are general overheads, which include the theatre rental costs, and amount to $250,000 per annum.

5 Maximum annual demand for A, B and C is 600, 800 and 1,200 procedures respectively. Time spent by each of the five different staff members on each procedure is as follows:

Part hours are shown as decimals e.g. 0·24 hours = 14·4 minutes (0·24 x 60).

Surgeon’s hours have been correctly identified as the bottleneck resource.

Required:

(a) Calculate the throughput accounting ratio for procedure C.

Note: It is recommended that you work in hours as provided in the table rather than minutes. (6 marks)

(b) The return per factory hour for products A and B has been calculated and is $2,612·53 and $2,654·40 respectively. The throughput accounting ratio for A and B has also been calculated and is 8·96 and 9·11 respectively.

Calculate the optimum product mix and the maximum profit per annum. (7 marks)

(c) Assume that your calculations in part (b) showed that, if the optimum product mix is adhered to, there will be excess demand for procedure C of 696 procedures per annum. In order to satisfy this excess demand, the company is considering equipping and using its own theatre, as well as continuing to rent the existing theatre. The company cannot rent any more theatre time at either the existing theatre or any other theatres in the area, so equipping its own theatre is the only option. An additional surgeon would be employed to work in the newly equipped theatre.

Required:

Discuss whether the overall profit of the company could be improved by equipping and using the extra theatre.

Note: Some basic calculations may help your discussion. (7 marks)

更多“Thin Co is a private hospital offering three types of surgical procedures known as A, B an”相关的问题

更多“Thin Co is a private hospital offering three types of surgical procedures known as A, B an”相关的问题

第1题

ment. Historically, the company has used solely financial performance measures to assess the performance of the company as a whole. The company’s Managing Director has recently heard of the ‘balanced scorecard approach’ and is keen to learn more.

Required:

Describe the balanced scorecard approach to performance measurement. (10 marks)

(b) Brace Co is split into two divisions, A and B, each with their own cost and revenue streams. Each of the divisions is managed by a divisional manager who has the power to make all investment decisions within the division. The cost of capital for both divisions is 12%. Historically, investment decisions have been made by calculating the return on investment (ROI) of any opportunities and at present, the return on investment of each division is 16%.

A new manager who has recently been appointed in division A has argued that using residual income (RI) to make investment decisions would result in ‘better goal congruence’ throughout the company.

Each division is currently considering the following separate investments:

The company is seeking to maximise shareholder wealth.

Required:

Calculate both the return on investment and residual income of the new investment for each of the two divisions. Comment on these results, taking into consideration the manager’s views about residual income. (10 marks)

第2题

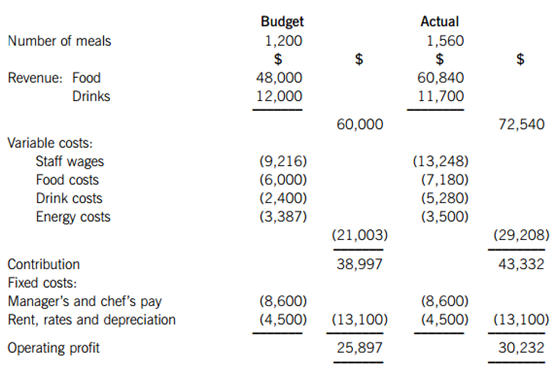

ight restaurant and kitchen staff, each paid a wage of $8 per hour on the basis of hours actually worked. It also has a restaurant manager and a head chef, each of whom is paid a monthly salary of $4,300. Noble’s budget and actual figures for the month of May was as follows:

The budget above is based on the following assumptions:

1 The restaurant is only open six days a week and there are four weeks in a month. The average number of orders each day is 50 and demand is evenly spread across all the days in the month.

2 The restaurant offers two meals: Meal A, which costs $35 per meal and Meal B, which costs $45 per meal. In addition to this, irrespective of which meal the customer orders, the average customer consumes four drinks each at $2·50 per drink. Therefore, the average spend per customer is either $45 or $55 including drinks, depending on the type of meal selected. The May budget is based on 50% of customers ordering Meal A and 50% of customers ordering Meal B.

3 Food costs represent 12·5% of revenue from food sales.

4 Drink costs represent 20% of revenue from drinks sales.

5 When the number of orders per day does not exceed 50, each member of hourly paid staff is required to work exactly six hours per day. For every incremental increase of five in the average number of orders per day, each member of staff has to work 0·5 hours of overtime for which they are paid at the increased rate of $12 per hour. You should assume that all costs for hourly paid staff are treated wholly as variable costs.

6 Energy costs are deemed to be related to the total number of hours worked by each of the hourly paid staff, and are absorbed at the rate of $2·94 per hour worked by each of the eight staff.

Required:

(a) Prepare a flexed budget for the month of May, assuming that the standard mix of customers remains the same as budgeted. (12 marks)

(b) After preparation of the flexed budget, you are informed that the following variances have arisen in relation to total food and drink sales:

(c) Noble’s owner told the restaurant manager to run a half-price drinks promotion at Noble for the month of May on all drinks. Actual results showed that customers ordered an average of six drinks each instead of the usual four but, because of the promotion, they only paid half of the usual cost for each drink. You have calculated the sales margin price variance for drink sales alone and found it to be a worrying $11,700 adverse. The restaurant manager is worried and concerned that this makes his performance for drink sales look very bad.

Required:

Briefly discuss TWO other variances that could be calculated for drinks sales or food sales in order to ensure that the assessment of the restaurant manager’s performance is fair. These should be variances that COULD be calculated from the information provided above although no further calculations are required here. (4 marks)

第3题

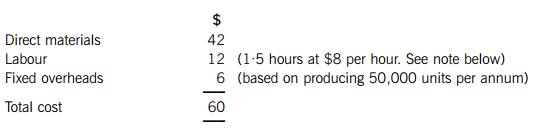

rial premises. It is about to launch a new product, the ‘Energy Buster’, a unique air conditioning unit which is capable of providing unprecedented levels of air conditioning using a minimal amount of electricity. The technology used in the Energy Buster is unique so Heat Co has patented it so that no competitors can enter the market for two years. The company’s development costs have been high and it is expected that the product will only have a five-year life cycle.

Heat Co is now trying to ascertain the best pricing policy that they should adopt for the Energy Buster’s launch onto the market. Demand is very responsive to price changes and research has established that, for every $15 increase in price, demand would be expected to fall by 1,000 units. If the company set the price at $735, only 1,000 units would be demanded.

The costs of producing each air conditioning unit are as follows:

Note

The first air conditioning unit took 1·5 hours to make and labour cost $8 per hour. A 95% learning curve exists, in relation to production of the unit, although the learning curve is expected to finish after making 100 units. Heat Co’s management have said that any pricing decisions about the Energy Buster should be based on the time it takes to make the 100th unit of the product. You have been told that the learning co-efficient, b = –0·0740005.

All other costs are expected to remain the same up to the maximum demand levels.

Required:

(a) (i) Establish the demand function (equation) for air conditioning units; (3 marks)

(ii) Calculate the marginal cost for each air conditioning unit after adjusting the labour cost as required by the note above; (6 marks)

(iii) Equate marginal cost and marginal revenue in order to calculate the optimum price and quantity. (3 marks)

(b) Explain what is meant by a ‘penetration pricing’ strategy and a ‘market skimming’ strategy and discuss whether either strategy might be suitable for Heat Co when launching the Energy Buster. (8 marks)

第4题

ilding industry. The company has found that when weather conditions are good, the demand for cement increases since more building work is able to take place. Last year, the weather was so good, and the demand for cement was so great, that Cement Co was unable to meet demand. Cement Co is now trying to work out the level of cement production for the coming year in order to maximise profits. The company doesn’t want to miss out on the opportunity to earn large profits by running out of cement again. However, it doesn’t want to be left with large quantities of the product unsold at the end of the year, since it deteriorates quickly and then has to be disposed of. The company has received the following estimates about the probable weather conditions and corresponding demand levels for the coming year:

Each bag of cement sells for $9 and costs $4 to make. If cement is unsold at the end of the year, it has to be disposed of at a cost of $0·50 per bag.

Cement Co has decided to produce at one of the three levels of production to match forecast demand. It now has to decide which level of cement production to select.

Required:

(a) Construct a pay off table to show all the possible profit outcomes. (8 marks)

(b) Decide the level of cement production the company should choose, based on the following decision rules:

(i) Maximin (1 mark)

(ii) Maximax (1 mark)

(iii) Expected value (4 marks)

You must justify your decision under each rule, showing all necessary calculations.

(c) Describe the ‘maximin’ and ‘expected value’ decision rules, explaining when they might be used and the attitudes of the decision makers who might use them. (6 marks)

第5题

e of high quality electrical appliances such as kettles, toasters and steam irons for domestic use which it sells to electrical stores in Voltland.

The directors consider that the existing product range could be extended to include industrial sized products such as high volume water boilers, high volume toasters and large steam irons for the hotel and catering industry. They recently commissioned a highly reputable market research organisation to undertake a market analysis which identifi ed a number of signifi cant competitors within the hotel and catering industry.

At a recent meeting of the board of directors, the marketing director proposed that BEG should make an application to gain ‘platinum status’ quality certifi cation in respect of their industrial products from the Hotel and Catering Institute of Voltland in order to gain a strong competitive position. He then stressed the need to focus on increasing the effectiveness of all operations from product design to the provision of after sales services.

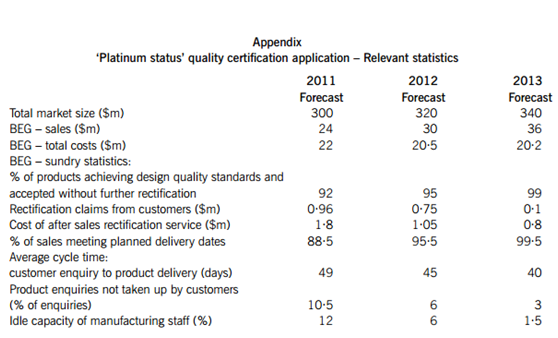

An analysis of fi nancial and non-fi nancial data relating to the application for ‘platinum status’ for each of the years 2011, 2012 and 2013 is contained in the appendix.

The managing director of BEG recently returned from a seminar, the subject of which was ‘The Use of Cost Targets’. She then requested the management accountant of BEG to prepare a statement of total costs for the application for platinum status for each of years 2011, 2012 and 2013. She further asked that the statement detailed manufacturing cost targets and the costs of quality.

The management accountant produced the following statement of manufacturing cost targets and the costs of quality:

Required:

(a) Explain how the use of cost targets could be of assistance to BEG with regard to their application for platinum status. Your answer must include commentary on the items contained in the statement of manufacturing cost targets and the costs of quality prepared by the management accountant. (8 marks)

(b) Assess the forecasted performance of BEG for the period 2011 to 2013 with reference to the application for ‘platinum status’ quality certifi cation under the following headings:

(i) Financial performance and marketing;

(ii) External effectiveness; and

(iii) Internal effi ciency. (12 marks)

第6题

pbuilding components market. The current job-costing system has two categories of direct cost (direct materials and direct manufacturing labour) and a single indirect cost pool (manufacturing overhead which is allocated on the basis of direct labour hours). The indirect cost allocation rate of the existing job-costing system is $120 per direct manufacturing labour-hour.

Recently, the Visibility Consultancy Partnership (VCP) proposed the use of an activity-based approach to redefi ne the job-costing system of SFS. VCP made a recommendation to retain the two direct cost categories. However, VCP further recommended the replacement of the single indirect-cost pool with fi ve indirect-cost pools.

Each of the fi ve indirect-cost pools represents an activity area at the manufacturing premises of SFS. Each activity area has its own supervisor who is responsible for his/her operating budget.

Relevant data are as follows:

SFS has recently invested in ‘state of the art’ IT systems which have the capability to automatically collate all of the data necessary for budgeting in each of the fi ve activity areas.

The management accountant of SFS calculated the manufacturing cost per unit of two representative jobs under the two costing systems as follows:

Required:

(a) (i) Compare the cost fi gures per unit for Job order 973 and Job order 974 calculated by the management accountant and explain the reasons for, and potential consequences of, the differences in the job cost estimates produced under the two costing systems; (8 marks)

(ii) Explain two potential problems that SFS might have experienced in the successful implementation of an activity-based costing system using its recently acquired ‘state of the art’ IT systems. (4 marks)

(b) ‘The application of Activity Based Management (ABM) requires that the management of SFS focus on each of the following:

(i) Operational ABM;

(ii) Strategic ABM;

(iii) The implicit value of an activity’.

Required:

Critically appraise the above statement and explain the risks attaching to the use of ABM. (8 marks)

第7题

Section B – TWO questions ONLY to be attempted

A local government housing department (LGHD) has funds which it is proposing to spend on the upgrading of air conditioning systems in its housing inventory.

It is intended that the upgrading should enhance the quality of living for the occupants of the houses.

Preferred contractors will be identifi ed to carry out the work involved in the upgrading of the air conditioning systems, with each contractor being responsible for upgrading of the systems in a proportion of the houses. Contractors will also be required to provide a maintenance and operational advice service during the fi rst two years of operation of the upgraded systems.

Prior to a decision to implement the proposal, LGHD has decided that it should carry out a value for money (VFM) audit.

You have been given the task of preparing a report for LGHD, to help ensure that it can make an informed decision concerning the proposal.

Required:

Prepare a detailed analysis which will form. the basis for the preparation of the fi nal report. The analysis should include a clear explanation of the meaning and relevance of each of (i) to (iii) below:

(i) Value for Money (VFM) audit (including references to the roles of principal and agent). (6 marks)

(ii) Economy, effi ciency and effectiveness as part of the VFM audit. (6 marks)

(iii) The extent (if any) to which each of intangibility, heterogeneity, simultaneity and perishability may be seen to relate to the decision concerning the proposal, and any problems that may occur. (8 marks)

Note: Your analysis should incorporate specifi c references to examples relating to the upgrading proposal.

第8题

ation located in Hartland, a developing country which has a large agricultural sector and where much transportation is provided by horses. EMA operates an Equine College which provides a range of undergraduate and postgraduate courses for students who wish to pursue a career in one of the following disciplines:

Equine (Horse) Surgery

Equine Dentistry, and E

quine Business Management.

The Equine College which has a maximum capacity of 1,200 students per annum is currently the only equine college in Hartland.

The following information is available:

(1) A total of 1,200 students attended the Equine College during the year ended 31 May 2010. Student mix and fees paid were as per the following table:

(2) Total operating costs (all fi xed) during the year amounted to $6,500,000.

(3) Operating costs of the Equine College are expected to increase by 4% during the year ending 31 May 2011. This led to a decision by the management to increase the fees of all students by 5% with effect from 1 June 2010. The management expect the number of students and the mix of students during the year ending 31 May 2011 to remain unchanged from those of the year ended 31 May 2010.

(4) EMA also operates a Riding School at which 240 horses are stabled. The Riding School is open for business on 360 days per annum. Each horse is available for four horse-riding lessons per day other than on the 40 days per annum that each horse is rested, i.e. not available for the provision of riding lessons. During the year ended 31 May 2010, the Riding School operated at 80% of full capacity.

(5) Horse-riding lessons are provided for riders in three different skill categories. These are ‘Beginner’, ‘Competent’ and ‘Advanced’.

During the year ended 31 May 2010, the fee per riding lesson was as follows:

(6) Total operating costs of the Riding School (all fi xed) amounted to $5,750,000 during the year ended 31 May 2010.

(7) It is anticipated that the operating costs of the Riding School will increase by 6% in the year ending 31 May 2011. The management have decided to increase the charge per lesson, in respect of ‘Competent’ and ‘Advanced’ riders by 10% with effect from 1 June 2010. There will be no increase in the charge per lesson for ‘Beginner’ riders.

(8) The lesson mix and capacity utilisation of the Riding School will remain the same during the year ending 31 May 2011.

Required:

(a) Prepare a statement showing the budgeted net profi t or loss for the year ending 31 May 2011. (7 marks)

Some time ago the government of Hartland, which actively promotes environmental initiatives, announced its intention to open an academy comprising an equine college and riding school. The management of EMA are uncertain of the impact that this will have on the budgeted number of students and riders during the year ending 31 May 2011, although they consider that due to the excellent reputation of the instructors at the riding school capacity utilisation could remain unchanged, or even increase, in spite of the opening of the government funded academy. Current estimates of the number of students entering the academy and the average capacity utilisation of the riding school are as follows:

Required:

(b) (i) Prepare a summary table which shows the possible net profi t or loss outcomes, and the combined probability of each potential outcome for the year ending 31 May 2011. The table should also show the expected value of net profi t or loss for the year; (9 marks)

(ii) Comment briefl y on the use of expected values by the management of EMA; (3 marks)

(iii) Suggest three reasons why the government of Hartland might have decided to open an academy comprising an equine college and a riding school. (6 marks)

第9题

Section A – BOTH questions are compulsory and MUST be attempted

The Superior Business Consultancy (SBC) which is based in Jayland provides clients with consultancy services in Advertising, Recruitment and IT Support. SBC commenced trading on 1 July 2003 and has grown steadily since then.

The following information, together with that contained in the appendix, is available:

(1) Three types of consultants are employed by SBC on a full-time basis. These are:

Advertising consultants who provide advice regarding advertising and promotional activities

Recruitment consultants who provide advice regarding recruitment and selection of staff, and

IT consultants who provide advice regarding the selection of business software and technical support.

(2) During the year ended 31 May 2010, each full-time consultant was budgeted to work on 200 days. All consultations undertaken by consultants of SBC had a duration of one day.

(3) During their 200 working days per annum, full-time consultants undertake some consultations on a ‘no-fee’ basis. Such consultations are regarded as Business Development Activity (BDA) by the management of SBC.

(4) SBC also engages the services of subcontract consultants who provide clients with consultancy services in the categories of Advertising, Recruitment and IT Support. All of the subcontract consultants have worked for SBC for at least three years.

(5) During recent years the directors of SBC have become increasingly concerned that SBC’s systems are inadequate for the measurement of performance. This concern was further increased after they each read a book entitled ‘How to improve business performance measurement’.

Required:

Prepare a report for the directors of SBC which:

(i) discusses the importance of non-fi nancial performance indicators (NFPIs) and evaluates, giving examples, how a ‘balanced scorecard’ approach may be used to improve performance within SBC; (13 marks)

(ii) contains a calculation of the actual average cost per chargeable consultation for both full-time consultants and separately for subcontract consultants in respect of each of the three categories of consultancy services during the year ended 31 May 2010; (7 marks)

(iii) suggests reasons for the trends shown by the fi gures contained in the appendix; (5 marks)

(iv) discusses the potential benefi ts and potential problems which might arise as a consequence of employing subcontract consultants within SBC. (6 marks)

Professional marks will be awarded in Question 1 for appropriateness of format, style. and structure of the report. (4 marks)

第10题

mance of CTC with

effect from 1 May 2009 (where only the products in (a) and (b) above are available for manufacture).

(4 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!