证券交易员课程测验

知识技能:1.专注。专注是一种技能,它能让更多的证券交易员练习它。因为有太多的财务信息,交易者需要能够磨练的重要,可操作的数据,将影响他们的交易。2.控制。证券交易员需要能够控制他们的情绪并坚持交易计划和战略。这对于通过止损或在设定点获利来管理风险尤为重要。

[单选题]

甲公司20×8年1月1日购入A公司当日发行的债券20万张,每张面值100元,票面年利率6%,期限3年,到期一次还本付息。甲公司当日支付价款1870万元,另支付交易费用3.37万元。甲公司取得此投资后,将其分类为以公允价值计量且其变动计入其他综合收益的金融资产,实际利率为8%。20×8年末上述债券的公允价值为2100万元,20×9年末的公允价值为2300万元。假定不考虑其他因素,甲公司该投资在20×9年末的摊余成本为()。

A .2300万元B .1896.85万元C .2212.49万元D .2185.10万元

[单选题]

甲公司和乙公司为同一集团控制的两家股份有限公司。2×15年3月1日,甲公司以银行存款100万元购入乙公司5%的股权,甲公司将其直接指定为以公允价值计量且其变动计入其他综合收益的金融资产核算,当日乙公司可辨认净资产的公允价值为1200万元。2×15年6月30日,该项股权的公允价值为120万元。2×15年7月1日,甲公司再次以一项固定资产为对价自集团母公司取得乙公司60%的股权,至此对乙公司能够实施控制。该项固定资产在增资当日的账面价值为800万元,公允价值为850万元。增资当日,乙公司可辨认净资产公允价值为1500万元,相对于集团母公司而言的所有者权益的账面价值为1600万元。假定该项交易不属于一揽子交易。不考虑其他因素,下列关于合并日个别报表会计处理的表述中,正确的是()。

A .甲公司应确认固定资产处置利得50万元B .合并日长期股权投资的初始投资成本为920万元C .合并日应确认资本公积(股本溢价)120万元D .其他权益工具投资确认的其他综合收益应在增资时转入资本公积(股本溢价)

[多选题]

关于金融负债和权益工具的区分,下列表述正确的有()。

A .如果一项金融工具须用或可用企业自身权益工具进行结算,且用于结算该工具的自身权益工具是作为现金或其他金融资产的替代品,则该金融工具是发行方的金融负债B .如果一项金融工具须用或可用企业自身权益工具进行结算,且用于结算该工具的自身权益工具是为了使该工具持有方享有在发行方扣除所有负债后的资产中的剩余权益,则该金融工具是发行方的权益工具C .对于将来须用或可用企业自身权益工具结算的金融工具,若为非衍生工具,且发行方未来有义务交付可变数量的自身权益工具进行结算,则该非衍生工具是发行方的金融负债D .对于将来须用或可用企业自身权益工具结算的金融工具,若为衍生工具,且发行方只能通过以固定数量的自身权益工具交换固定金额的现金或其他金融资产进行结算,则该衍生工具是发行方的金融负债

[多选题]

《企业会计准则——固定资产》第十三条规定,确定固定资产成本时,应当考虑预计弃置费用因素。下列关于弃置费用的说法正确的有()。

A .一般企业的固定资产无须考虑弃置费用B .弃置费用仅针对特殊行业的特殊固定资产,例如石油天然气行业的油气资产、核电站的核燃料等。这些行业均承担了环保法规规定的环境恢复义务,且金额较大(可能大于相关固定资产的购建支出)C .弃置费用需要考虑货币时间价值的影响且计算现值D .所有企业的所有固定资产都需考虑弃置费用

[多选题]

企业因追加投资将原持有的指定为以公允价值计量且其变动计入其他综合收益的金融资产转为对非同一控制下子公司的投资,下列关于购买日报表中会计处理的表述中,正确的有()。

A .个别报表中应将原金融资产持有期间确认的其他综合收益在购买日结转计入留存收益B .合并报表中应将原金融资产的账面价值与新增股权支付对价的公允价值之和作为合并成本C .个别报表中原金融资产应转为长期股权投资核算D .合并报表中应在购买日确认商誉或营业外收入

[单选题]

关于金融负债和权益工具区分的基本原则表述中,不正确的是()。

A .如果企业不能无条件地避免以交付现金或其他金融资产来履行一项合同义务,则该合同义务按权益工具核算B .如果企业能够无条件地避免交付现金或其他金融资产,例如能够根据相应的议事机制自主决定是否支付股息,同时所发行的金融工具没有到期日且持有方没有回售权或虽有固定期限但发行方有权无限期递延,则此类交付现金或其他金融资产的结算条款不构成金融负债C .如果发放股利由发行方根据相应的议事机制自主决定,则股利是累积股利还是非累积股利本身均不会影响该金融工具被分类为权益工具D .对于非衍生工具,如果发行方未来有义务交付可变数量的自身权益工具进行结算,则该非衍生工具是金融负债

[单选题]

甲公司于2×20年1月1日正式建造完成一个核电站并交付使用,全部的成本为6000万元,预计使用寿命为30年。据国家法律、行政法规和国际公约等规定,企业应承担环境保护和生态恢复等义务。2×20年1月1日预计30年后该核电站的弃置费用为300万元(金额较大)。在考虑货币的时间价值和相关期间通货膨胀等因素下确定的折现率为5%。已知:(P/F,5%,30)=0.2314,(P/A,5%,30)=15.3725。不考虑其他因素,甲公司在2×20年确认该固定资产的入账价值为()。

A .10611.75万元B .6069.42万元C .6000万元D .6300万元

[多选题]

企业因增资将原持有的以公允价值计量且其变动计入其他综合收益的非交易性权益工具投资转为对子公司的股权投资,形成非同一控制下企业合并时,下列各项会计处理的表述中,正确的有()。

A .合并报表中应将原股权在购买日的公允价值加上新增股权支付对价的公允价值之和作为合并成本B .个别报表中应将原股权持有期间确认的其他综合收益结转计入留存收益C .个别报表中应将原股权持有期间确认的其他综合收益结转计入处置股权当期损益D .合并报表中应将原股权的账面价值加上新增股权支付的对价的公允价值之和作为合并成本

[单选题]

A bond has a par value of $1,000, a time to maturity of 20 years, a coupon rateof 10% with interest paid annually, a current price of $850 and a yield to maturity of 12%.Intuitively and without the use calculations, if interest payments are reinvested at 10%, therealized compound yield on this bond must be().

A .10.00%B .10.9%C .12.0%D .12.4%E .none of the above

[单选题]

Most corporate bonds are traded()

A .on a formal exchange operated by the New York Stock Exchange.B .by the issuing corporation.C .over the counter by bond dealers linked by a computer quotation system.D .on a formal exchange operated by the American Stock Exchange.E .on a formal exchange operated by the Philadelphia Stock Exchange.

[单选题]

When a bond indenture includes a sinking fund provision()

A .firms must establish a cash fund for future bond redemption.B .bondholders always benefit, because principal repayment on the scheduled maturity date is guaranteed.C .bondholders may lose because their bonds can be repurchased by the corporation at below-market prices.D .both A and B are true.E .none of the above is true.

[单选题]

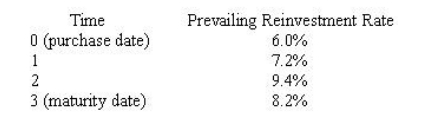

Three years ago you purchased a bond for $974.69. The bond had three years

to maturity, a coupon rate of 8%, paid annually, and a face value of $1,000. Each year you

reinvested all coupon interest at the prevailing reinvestment rate shown in the table below.

Today is the bond's maturity date. What is your realized compound yield on the bond?()

A .6.43%B .7.96%C .8.23%D .8.97%E .9.13%

[单选题]

Consider two bonds, F and G. Both bonds presently are selling at their par value of $1,000. Each pays interest of $90 annually. Bond F will mature in 15 years while bond G will mature in 26 years. If the yields to maturity on the two bonds change from 9% to 10%,().

A .both bonds will increase in value, but bond F will increase more than bond GB .both bonds will increase in value, but bond G will increase more than bond FC .both bonds will decrease in value, but bond F will decrease more than bond GD .both bonds will decrease in value, but bond G will decrease more than bond FE .none of the above

[单选题]

You have just purchased a 7-year zero-coupon bond with a yield to maturity of 11% and a par value of $1,000. What would your rate of return at the end of the year be if you sell the bond? Assume the yield to maturity on the bond is 9% at the time you sell.

A .10.00%B .23.8%C .13.8%D .1.4%E .none of the above

[单选题]

If a 9% coupon bond that pays interest every 182 days paid interest 112 days ago, the accrued interest would be

A .27.69B .27.35C .26.77D .27.98E .28.15

[单选题]

Under which scenario is basis risk likely to exist?()

A .A hedge (which was initially matched to the maturity of the underlying) is lifted before expiration.B .The correlation of the underlying and the hedge vehicle is less than one and their volatilities are unequal.C .The underlying instrument and the hedge vehicle are dissimilar.D .All of the above are correct.

[单选题]

Let Ω be a sample space. Let be an event. The complement of E is denoted by

be an event. The complement of E is denoted by  and it can be defined as follows:().

and it can be defined as follows:().

A .

B .

[单选题]

In rigorous probability theory,().

A .all the subsets of the sample space Ω can always be considered events.B .only the subsets of Ω that belong to a certain sigma-algebra (the space of events) can be considered events.C .only the subsets of Ω that have probability strictly greater than zero can be considered events.D .only the subsets of Ω whose complements have probability strictly greater than zero can be considered events.

[单选题]

Suppose you independently flip a coin times and the outcome of each toss can be either head (with probability ) or tails (also with probability ). Denote by the number of times the outcome is tails (out of the tosses). The random variable has a:().

A .Poisson distributionB .binomial distributionC .Bernoulli distributionD .exponential distribution

[单选题]

What feature of cash and futures prices tends to make hedging possible?()

A .They always move together in the same direction and by the same amount.B .They move in opposite directions by the same amount.C .They tend to move together, generally in the same direction and by the same amount.D .They move in the same direction by different amounts.