重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

Mighty IT Co provides hardware, software and IT services to small business customers.

Mighty IT Co has developed an accounting software package. The company offers a supply and installation service for $1,000 and a separate two-year technical support service for $500. Alternatively, it also offers a combined goods and services contract which includes both of these elements for $1,200. Payment for the combined contract is due one month after the date of installation.

In December 20X5, Mighty IT Co revalued its corporate headquarters. Prior to the revaluation, the carrying amount of the building was $2m and it was revalued to $2·5m.

Mighty IT Co also revalued a sales office on the same date. The office had been purchased for $500,000 earlier in the year, but subsequent discovery of defects reduced its value to $400,000. No depreciation had been charged on the sales office and any impairment loss is allowable for tax purposes.

Mighty It Co’s income tax rate is 30%.

In accordance with IFRS 15 Revenue from Contracts with Customers, when should Mighty IT Co recognise revenue from the combined goods and services contract?

A.Supply and install: on installation Technical support: over two years

B.Supply and install: when payment is made Technical support: over two years

C.Supply and install: on installation Technical support: on installation

D.Supply and install: when payment is made Technical support: when payment is made

In January 20X6, the accountant at Mighty IT Co produced the company’s draft financial statements for the year ended 31 December 20X5. He then realised that he had omitted to consider deferred tax on development costs. In 20X5, development costs of $200,000 had been incurred and capitalised. Development costs are deductible in full for tax purposes in the year they are incurred. The development is still in process at 31 December 20X5.

What adjustment is required to the income tax expense in Mighty IT Co’s statement of profit or loss for the year ended 31 December 20X5 to account for deferred tax on the development costs?

A.Increase of $200,000

B.Increase of $60,000

C.Decrease of $60,000

D.Decrease of $200,000

For each combined contract sold, what is the amount of revenue which Mighty IT Co should recognise in respect of the supply and installation service in accordance with IFRS 15?A.$700

B.$800

C.$1,000

D.$1,200

In accordance with IAS 12 Income Taxes, what is the impact of the property revaluations on the income tax expense of Mighty IT Co for the year ended 31 December 20X5?

A.Income tax expense increases by $180,000

B.Income tax expense increases by $120,000

C.Income tax expense decreases by $30,000

D.No impact on income tax expense

Mighty IT Co sells a combined contract on 1 January 20X6, the first day of its financial year.

In accordance with IFRS 15, what is the total amount for deferred income which will be reported in Mighty IT Co’s statement of financial position as at 31 December 20X6?

A.$400

B.$250

C.$313

D.$200

更多“The following scenario relates to questions 11–15.”相关的问题

更多“The following scenario relates to questions 11–15.”相关的问题

第1题

Alisa commenced trading on 1 January 2015. Her sales since commencement have been as follows:

The above figures are stated exclusive of value added tax (VAT). Alisa only supplies services, and these are all standard rated for VAT purposes. Alisa notified her liability to compulsorily register for VAT by the appropriate deadline.

For each of the eight months prior to the date on which she registered for VAT, Alisa paid £240 per month (inclusive of VAT) for website design services and £180 per month (exclusive of VAT) for advertising. Both of these supplies are standard rated for VAT purposes and relate to Alisa’s business activity after the date from when she registered for VAT.

After registering for VAT, Alisa purchased a motor car on 1 January 2016. The motor car is used 60% for business mileage. During the quarter ended 31 March 2016, Alisa spent £456 on repairs to the motor car and £624 on fuel for both her business and private mileage. The relevant quarterly scale charge is £294.

All of these figures are inclusive of VAT. All of Alisa’s customers are registered for VAT, so she appreciates that she has to issue VAT invoices when services are supplied.

From what date would Alisa have been required to be compulsorily registered for VAT and therefore have had to charge output VAT on her supplies of services?

A.30 September 2015

B.1 November 2015

C.1 October 2015

D.30 October 2015

What amount of pre-registration input VAT would Alisa have been able to recover in respect of inputs incurred prior to the date on which she registered for VAT?A.£468

B.£608

C.£536

D.£456

How and by when does Alisa have to pay any VAT liability for the quarter ended 31 March 2016?A.Using any payment method by 30 April 2016

B.Electronically by 7 May 2016

C.Electronically by 30 April 2016

D.Using any payment method by 7 May 2016

Which of the following items of information is Alisa NOT required to include on a valid VAT invoice?A.The customer’s VAT registration number

B.An invoice number

C.The customer’s address

D.A description of the services supplied

What is the maximum amount of input VAT which Alisa can reclaim in respect of her motor expenses for the quarter ended 31 March 2016?A.£108

B.£138

C.£180

D.£125

请帮忙给出每个问题的正确答案和分析,谢谢!

第2题

Mighty IT Co provides hardware, software and IT services to small business customers.

Mighty IT Co has developed an accounting software package. The company offers a supply and installation service for $1,000 and a separate two-year technical support service for $500. Alternatively, it also offers a combined goods and services contract which includes both of these elements for $1,200. Payment for the combined contract is due one month after the date of installation.

In December 20X5, Mighty IT Co revalued its corporate headquarters. Prior to the revaluation, the carrying amount of the building was $2m and it was revalued to $2·5m.

Mighty IT Co also revalued a sales office on the same date. The office had been purchased for $500,000 earlier in the year, but subsequent discovery of defects reduced its value to $400,000. No depreciation had been charged on the sales office and any impairment loss is allowable for tax purposes.

Mighty It Co’s income tax rate is 30%.

In accordance with IFRS 15 Revenue from Contracts with Customers, when should Mighty IT Co recognise revenue from the combined goods and services contract?

A.Supply and install: on installation Technical support: over two years

B.Supply and install: when payment is made Technical support: over two years

C.Supply and install: on installation Technical support: on installation

D.Supply and install: when payment is made Technical support: when payment is made

In January 20X6, the accountant at Mighty IT Co produced the company’s draft financial statements for the year ended 31 December 20X5. He then realised that he had omitted to consider deferred tax on development costs. In 20X5, development costs of $200,000 had been incurred and capitalised. Development costs are deductible in full for tax purposes in the year they are incurred. The development is still in process at 31 December 20X5.

What adjustment is required to the income tax expense in Mighty IT Co’s statement of profit or loss for the year ended 31 December 20X5 to account for deferred tax on the development costs?

A.Increase of $200,000

B.Increase of $60,000

C.Decrease of $60,000

D.Decrease of $200,000

For each combined contract sold, what is the amount of revenue which Mighty IT Co should recognise in respect of the supply and installation service in accordance with IFRS 15?A.$700

B.$800

C.$1,000

D.$1,200

In accordance with IAS 12 Income Taxes, what is the impact of the property revaluations on the income tax expense of Mighty IT Co for the year ended 31 December 20X5?

A.Income tax expense increases by $180,000

B.Income tax expense increases by $120,000

C.Income tax expense decreases by $30,000

D.No impact on income tax expense

Mighty IT Co sells a combined contract on 1 January 20X6, the first day of its financial year.

In accordance with IFRS 15, what is the total amount for deferred income which will be reported in Mighty IT Co’s statement of financial position as at 31 December 20X6?

A.$400

B.$250

C.$313

D.$200

请帮忙给出每个问题的正确答案和分析,谢谢!

第3题

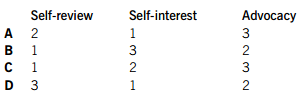

Sycamore & Co is the auditor of Fir Co, a listed computer software company. The audit team comprises an engagement partner, a recently appointed audit manager, an audit senior and a number of audit assistants. The audit engagement partner has only been appointed this year due to the rotation of the previous partner who had been involved in the audit for seven years. Only the audit senior has experience of auditing a company in this specialised industry. The previous audit manager, who is a close friend of the new audit manager, left the firm before the completion of the prior year audit and is now the finance director of Fir Co.

The board of Fir Co has asked if Sycamore & Co can take on some additional work and have asked if the following additional non-audit services can be provided:

(1) Routine maintenance of payroll records

(2) Assistance with the selection of a new financial controller including the checking of references

(3) Tax services whereby Sycamore & Co would liaise with the tax authority on Fir Co’s behalf

Sycamore & Co has identified that the current year fees to be received from Fir Co for audit and other services will represent 16% of the firm’s total fee income and totalled 15·5% in the prior year. The audit engagement partner has asked you to consider what can be done in relation to this self-interest threat.

In relation to the composition of the current audit team, which of the following correctly identifies the fundamental principle which is at risk and provides an appropriate safeguard?

A.A

B.B

C.C

D.D

Which of the following identifies the threat which could arise as a result of the finance director’s previous employment at Sycamore & Co and recommends an appropriate safeguard?

A.A self-review threat; review the work performed by the previous audit manager

B.A familiarity threat; a different audit manager should be appointed

C.A self-review threat; change the existing audit plan

D.A familiarity threat; the firm should resign from the engagement

Ignoring the potential effect on total fee levels, which of the following options correctly identifies the threats to independence from providing the above non-audit services?

A.A

B.B

C.C

D.D

Which of the following safeguards would NOT be relevant in mitigating the threat identified in relation to fees?

A.Disclosure to those charged with governance that fees from Fir Co represent more than 15% of Sycamore & Co’s total fee income

B.A pre-issuance review to be conducted by an external accountant

C.The use of separate teams to provide the audit and non-audit services

D.A post-issuance review to be conducted by an external accountant or regulatory body

During the course of the audit of Fir Co, a suspicious cash transfer has been identified. The audit team has reported this to the relevant firm representative as a potential money-laundering transaction.

Which of the following statements is true regarding the confidentiality of this information?

A.Details of the transaction can only be disclosed with the permission of Fir Co

B.If there is a legal requirement to report money-laundering, this overrides the principle of confidentiality

C.Sycamore & Co is not permitted to disclose details of the suspicious transaction as the information has been obtained during the course of the audit

D.In order to maintain confidentiality, Sycamore & Co should report their concerns anonymously

请帮忙给出每个问题的正确答案和分析,谢谢!

第4题

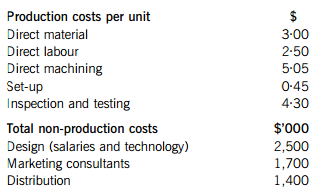

Helot Co develops and sells computer games. It is well known for launching innovative and interactive role-playing games and its new releases are always eagerly anticipated by the gaming community. Customers value the technical excellence of the games and the durability of the product and packaging.

Helot Co has previously used a traditional absorption costing system and full cost plus pricing to cost and price its products. It has recently recruited a new finance director who believes the company would benefit from using target costing. He is keen to try this method on a new game concept called Spartan, which has been recently approved.

After discussion with the board, the finance director undertook some market research to find out customers’ opinions on the new game concept and to assess potential new games offered by competitors. The results were used to establish a target selling price of $45 for Spartan and an estimated total sales volume of 350,000 units. Helot Co wants to achieve a target profit margin of 35%.

The finance director has also begun collecting cost data for the new game and has projected the following:

Which of the following statements would the finance director have used to explain to Helot Co’s board what the benefits were of adopting a target costing approach so early in the game’s life-cycle?

(1) Costs will be split into material, system, and delivery and disposal categories for improved cost reduction analysis

(2) Customer requirements for quality, cost and timescales are more likely to be included in decisions on product development

(3) Its key concept is based on how to turn material into sales as quickly as possible in order to maximise net cash

(4) The company will focus on designing out costs prior to production, rather than cost control during live production

A.1, 2 and 4

B.2, 3 and 4

C.1 and 3

D.2 and 4 only

第5题

The following information relates to an investment project which is being evaluated by the directors of Fence Co, a listed company. The initial investment, payable at the start of the first year of operation, is $3·9 million.

The directors believe that this investment project will increase shareholder wealth if it achieves a return on capital employed greater than 15%. As a matter of policy, the directors require all investment projects to be evaluated using both the payback and return on capital employed methods. Shareholders have recently criticised the directors for using these investment appraisal methods, claiming that Fence Co ought to be using the academically-preferred net present value method.

The directors have a remuneration package which includes a financial reward for achieving an annual return on capital employed greater than 15%. The remuneration package does not include a share option scheme.

What is the payback period of the investment project?

A.2·75 years

B.1·50 years

C.2·65 years

D.1·55 years

Which of the following statements about investment appraisal methods is correct?A.The return on capital employed method considers the time value of money

B.Return on capital employed must be greater than the cost of equity if a project is to be accepted

C.Riskier projects should be evaluated with longer payback periods

D.Payback period ignores the timing of cash flows within the payback period

Which of the following statements about Fence Co is/are correct?

(1) Managerial reward schemes of listed companies should encourage the achievement of stakeholder objectives

(2) Requiring investment projects to be evaluated with return on capital employed is an example of dysfunctional behaviour encouraged by performance-related pay

(3) Fence Co has an agency problem as the directors are not acting to maximise the wealth of shareholders

A.1 and 2 only

B.1 only

C.2 and 3 only

D.1, 2 and 3

Which of the following statements about Fence Co directors’ remuneration package is/are correct?

(1) Directors’ remuneration should be determined by senior executive directors

(2) Introducing a share option scheme would help bring directors’ objectives in line with shareholders’ objectives

(3) Linking financial rewards to a target return on capital employed will encourage short-term profitability and discourage capital investment

A.2 only

B.1 and 3 only

C.2 and 3 only

D.1, 2 and 3

Based on the average investment method, what is the return on capital employed of the investment project?

A.13·3%

B.26·0%

C.52·0%

D.73·5%

请帮忙给出每个问题的正确答案和分析,谢谢!

第6题

BJM CO The following scenario relates to questions 11 – 15. You are an audit senior of YHT & Co and have worked on the external audit of BJM Co (BJM), an unlisted company, since your firm was appointed external auditor two years ago. BJM owns a chain of nine restaurants and is a successful company. BJM has always been subject to national hygiene regulations, especially in relation to the food preparation process. Non-compliance can result in a large fine or closure of the restaurant concerned. Despite running a successful company, BJM’s Board have often needed to be reminded of some fundamental principles and you often have to explain key concepts. Which of the following statements best defines the external audit?

A、The external audit is an exercise carried out by auditors in order to give an opinion on whether the financial statements of a company are fairly presented.

B、The external audit is an exercise carried out in order to give an opinion on the effectiveness of a company's internal control system.

C、The external audit is performed by management to identify areas of deficiency within a company and to make recommendations to mitigate those deficiencies.

D、The external audit provides negative assurance on the truth and fairness of a company's financial statements.

第7题

KLE Co The following scenario relates to questions 16 – 20. You are an audit manager in the internal audit department of KLE Co, a listed retail company. The internal audit department is auditing the company's procurement system. KLE’s ordering department consists of six members of staff: one chief buyer and five purchasing clerks. All orders are raised on pre-numbered purchase requisition forms, and are sent to the ordering department. In the ordering department, each requisition form is approved and signed by the chief buyer. A purchasing clerk transfers the order information onto an order form and identifies the appropriate supplier for the goods. Part one of the two part order form is sent to the supplier and part two to the accounts department. The requisition is thrown away. Which of the following is NOT a likely effect of the deficiencies in the internal control system described?

A、Purchases may be made unnecessarily at unauthorised prices

B、Subsequent queries on orders cannot be traced back to the original requisition

C、The order forms may contain errors that are not identified

D、Goods could be ordered twice in error or deliberately

第8题

Adana died on 17 March 2016, and inheritance tax (IHT) of £566,000 is payable in respect of her chargeable estate. Under the terms of her will, Adana left her entire estate to her children.

At the date of her death, Adana had the following debts and liabilities:

(1) An outstanding interest-only mortgage of £220,000.

(2) Income tax of £43,700 payable in respect of the tax year 2015–16.

(3) Legal fees of £4,600 incurred by Adana’s sister which Adana had verbally promised to pay.

Adana’s husband had died on 28 May 2006, and only 20% of his inheritance tax nil rate band was used on his death. The nil rate band for the tax year 2006–07 was £285,000.

On 22 April 2006, Adana had made a chargeable lifetime transfer of shares valued at £500,000 to a trust. Adana paid the lifetime IHT of £52,250 arising from this gift. If Adana had not made this gift, her chargeable estate at the time of her death would have been £650,000 higher than it otherwise was. This was because of the subsequent increase in the value of the gifted shares.

What is the maximum nil rate band which will have been available when calculating the IHT of £566,000 payable in respect of Adana’s chargeable estate?

A.£325,000

B.£553,000

C.£390,000

D.£585,000

What is the total amount of deductions which would have been permitted in calculating Adana’s chargeable estate for IHT purposes?A.£263,700

B.£268,300

C.£43,700

D.£220,000

Who will be responsible for paying the IHT of £566,000 in respect of Adana’s chargeable estate, and what is the due date for the payment of this liability?A.The beneficiaries of Adana’s estate (her children) on 30 September 2016

B.The beneficiaries of Adana’s estate (her children) on 17 September 2016

C.The personal representatives of Adana’s estate on 30 September 2016

D.The personal representatives of Adana’s estate on 17 September 2016

How much IHT did Adana save by making the chargeable lifetime transfer of £500,000 to a trust on 22 April 2006, rather than retaining the gifted investments until her death?A.£260,000

B.£207,750

C.£147,750

D.£200,000

How much of the IHT payable in respect of Adana’s estate would have been saved if, under the terms of her will, Adana had made specific gifts of £400,000 to a trust and £200,000 to her grandchildren, instead of leaving her entire estate to her children?A.£240,000

B.£160,000

C.£0

D.£80,000

第9题

Herd Co is based in a country whose currency is the dollar ($). The company expects to receive €1,500,000 in six months’ time from Find Co, a foreign customer. The finance director of Herd Co is concerned that the euro (€) may depreciate against the dollar before the foreign customer makes payment and she is looking at hedging the receipt.

Herd Co has in issue loan notes with a total nominal value of $4 million which can be redeemed in 10 years’ time. The interest paid on the loan notes is at a variable rate linked to LIBOR. The finance director of Herd Co believes that interest rates may increase in the near future.

The spot exchange rate is €1·543 per $1. The domestic short-term interest rate is 2% per year, while the foreign short-term interest rate is 5% per year.

What is the six-month forward exchange rate predicted by interest rate parity?

A.€1·499 per $1

B.€1·520 per $1

C.€1·566 per $1

D.€1·588 per $1

As regards the interest rate risk faced by Herd Co, which of the following statements is correct?A.In exchange for a premium, Herd Co could hedge its interest rate risk by buying interest rate options

B.Buying a floor will give Herd Co a hedge against interest rate increases

C.Herd Co can hedge its interest rate risk by buying interest rate futures now in order to sell them at a future date

D.Taking out a variable rate overdraft will allow Herd Co to hedge the interest rate risk through matching

Which of the following hedging methods will NOT be suitable for hedging the euro receipt?A.Forward exchange contract

B.Money market hedge

C.Currency futures

D.Currency swap

Which of the following statements support the finance director’s belief that the euro will depreciate against the dollar?

(1) The dollar inflation rate is greater than the euro inflation rate

(2) The dollar nominal interest rate is less than the euro nominal interest rate

A.1 only

B.2 only

C.Both 1 and 2

D.Neither 1 nor 2

As regards the euro receipt, what is the primary nature of the risk faced by Herd Co?A.Transaction risk

B.Economic risk

C.Translation risk

D.Business risk

第10题

The following information relates to questions 13 and 14. Each unit of product Zeta requires 3 kg of raw material and 4 direct labour hours. Material costs $2 per kg and the direct labour rate is $7 per hour. The production budget for Zeta for April to June is as follows. April May June Production units 7,800 8,400 8,200 Raw material opening inventories are budgeted as follows. April May June 3,800 kg 4,200 kg 4,100 kg The closing inventory budgeted for June is 3,900 kg. Material purchases are paid for in the month following purchase. What is the figure to be included in the cash budget for June in respect of payments for purchases?

A、$25,100

B、$48,800

C、$50,200

D、$50,600

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!