重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

In certain circumstances an individual is automatically not resident in the UK.

Which of the following two individuals, if either, is automatically not resident in the UK for the tax year 2015–16?

Eric, who has never previously been resident in the UK. In the tax year 2015–16, he was in the UK for 40 days.

Fran, who was resident in the UK for the two tax years prior to the tax year 2015–16. In the tax year 2015–16, she was in the UK for 18 days.

A.Eric only

B.Fran only

C.Both Eric and Fran

D.Neither Eric nor Fran

更多“In certain circumstances an individual is automatically not resident in the UK.Which of th”相关的问题

更多“In certain circumstances an individual is automatically not resident in the UK.Which of th”相关的问题

第1题

.

For the year ended 31 December 2015, the net VAT payable by Triangle Ltd was £73,500.

For the year ended 31 December 2014, the net VAT payable by Triangle Ltd was £47,700.

What monthly payments on account of VAT must Triangle Ltd make in respect of the year ended 31 December 2015 prior to submitting its VAT return for that year?

A.Nine monthly payments of £7,350

B.Nine monthly payments of £4,770

C.Ten monthly payments of £4,770

D.Ten monthly payments of £7,350

第2题

ast three tax years:

What is the maximum gross contribution which Abena can make to her personal pension scheme for the tax year 2015–16 without giving rise to an annual allowance charge?

A.£63,000

B.£40,000

C.£65,000

D.£55,000

第3题

On 31 March 2016, Angus sold a house, which he had bought on 31 March 2002.

Angus occupied the house as his main residence until 31 March 2007, when he left for employment abroad.

Angus returned to the UK on 1 April 2009 and lived in the house until 31 March 2010, when he bought a flat in a neighbouring town and made that his principal private residence.

What is Angus’ total number of qualifying months of occupation for principal private residence relief on the sale of the house?

A.72 months

B.54 months

C.114 months

D.96 months

第4题

s true?

A.Individuals with tax payable of less than £1,000 for a tax year are not required to file a tax return

B.Individuals are only required to file a tax return for a tax year if they receive a notice to deliver from HM Revenue and Customs (HMRC)

C.All individuals who submit a tax return on time are able to have their tax payable calculated by HM Revenue and Customs (HMRC)

D.The tax return for an individual covers income tax, class 1, class 2 and class 4 national insurance contributions and capital gains tax liabilities

第5题

Which of the following statements is/are true?

(1) Corporation tax is a direct tax on the turnover of companies

(2) National insurance is a direct tax suffered by employees, employers and the self-employed on earnings

(3) Inheritance tax is a direct tax on transfers of income by individuals

(4) Value added tax is a direct tax on the supply of goods and services by businesses

A.1 and 3 only

B.2 only

C.1, 2, 3 and 4

D.1, 2 and 4 only

第6题

re prior to 1 January 2015:

What is the amount of Lili Ltd’s deductible pre-trading expenditure in respect of the year ended 31 December 2015?

A.£10,000

B.£14,000

C.£27,000

D.£29,000

第7题

On 1 July 2014, Sameer made a cash gift of £2,500 to his sister.

On 1 May 2015, he made a cash gift of £2,000 to a friend.

On 1 June 2015, he made a cash gift of £50,000 to a trust. Sameer has not made any other lifetime gifts.

In respect of Sameer’s cash gift of £50,000 to the trust, what is the lifetime transfer of value for inheritance tax purposes after taking account of all available exemptions?

A.£48,500

B.£44,000

C.£46,000

D.£46,500

第8题

rprise income tax (EIT) rate is 25%. The company’s accountant has prepared the following statement of profit or loss for the year end 31 December 2014.

Notes:

(1) Customers who settle their bills within 30 days receive an early payment discount of 2%. Discounts totalling RMB55,000 were deducted directly from sales.

(2) Staff welfare is calculated and provided for in the accounts at 14% of the wages and salaries paid of RMB8,240,000. The actual amount of staff welfare expenses incurred was RMB1,026,350.

(3) Entertainment expenses incurred in the year 2014 were as charged in the profit or loss account, i.e. RMB967,000. Entertainment expenses incurred in 2013 in excess of the deduction threshold were RMB68,000.

(4) The bad debt related to a debtor who went bankrupt in 2013. The accountant has submitted a report to the tax bureau in relation to this bad debt.

(5) The specific provision for doubtful debts relates to an amount which was difficult to recover. The accountant has submitted a report to the tax bureau in relation to this specific provision.

(6) These research and development costs qualified for an additional deduction.

(7) The compensation was due to the late delivery of software to the customers.

(8) Sware Ltd was penalised by the State Administration for Industry and Commerce because of misstatements on its website.

(9) Project Pibeta relates to the piloting of software encouraged by the government. The project was started in 2013 and is expected to be completed in 2016. The project is subsidised by the government (see (18) below).

(10) A fire destroyed a warehouse with a net book value of RMB2,500,000. Sware Ltd received insurance compensation of RMB2,284,000. The accountant has submitted a report to the tax bureau in relation to this loss.

(11) Sware Ltd declared an interim dividend of RMB5,000,000 in 2014. Individual income tax was withheld from this interim dividend before distribution to the company’s shareholders.

(12) A donation receipt was obtained for the donation to China Red-Cross.

(13) A donation receipt was obtained for the donation to the school.

(14) Sware Ltd acquired a new subsidiary in 2014 and wrote off the goodwill incurred on this acquisition.

(15) Sware Ltd lent some of its surplus funds to its Shanghai subsidiary at an interest rate of 36% per annum. The market interest rate was 8% per annum.

(16) Sware Ltd has invested some of its surplus funds in the capital market. The profit on the sale of government bonds included interest of RMB15,000.

(17) The A-shares were acquired in 2012.

(18) The government granted Sware Ltd a specific financial subsidy to cover all of the expenditure on Project Pibeta.

Required:

(a) Calculate the enterprise income tax (EIT) payable by Sware Ltd for the year 2014.

Note: You should start your computation with the net loss figure of RMB3,385,150 and list all of the items referred to in notes (1) to (18) identifying any items which do not require adjustment by the use of zero (0). (11 marks)

(b) Identify and briefly describe ANY TWO enterprise income tax (EIT) preferential policies which Sware Ltd could consider applying, in addition to the qualified research and development additional deduction. (4 marks)

第9题

:

Option A: Joining Delta Ltd as a manager with a monthly salary of RMB40,000 and an annual bonus of RMB100,000 payable in December each year.

Option B: Providing services to Delta Ltd as a consultant for a consultancy fee of RMB50,000 per month.

Option C: Setting up his own sole proprietorship. He will pay himself a monthly salary of RMB20,000 from this sole proprietorship. For 2014 the net profit of the sole proprietorship after charging Mr Xu’s salary is expected to be RMB420,000.

Option D: Setting up a limited company, Xupa Ltd. He will pay himself a monthly salary of RMB20,000 from Xupa Ltd. For 2014 the net profit of the company after charging Mr Xu’s salary is expected to be RMB420,000. Xupa Ltd will pay enterprise income tax at the rate of 25% and distribute all of its profit after tax to its shareholder, Mr Xu, as a dividend.

Required:

Calculate the individual income tax (IIT) payable by Mr Xu for 2014 under each of the four options.

Note: Ignore value added tax and business tax. (10 marks)

(b) State, giving reasons, whether the following persons will be subject to individual income tax in China on their worldwide income in 2014:

(1) Ms Wang has her household in Xiamen and holds a China identity card. She has been studying in Australia since 2010 and has not returned to China for the last six years, including in 2014.

(2) Mr Beth is a US citizen, who has lived in China working for a non-government organisation since 2010. He has not travelled outside China for the last six years, including in 2014.

(3) Ms Ruth is an Australian citizen. She travelled to China and stayed in China for a total of 250 days in 2014. (5 marks)

第10题

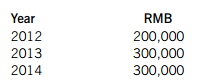

(a) Chris and Wendy graduated from high school in 2012 and set up a hair-dressing shop in the form. of a limited company, Hair Ltd. The total amounts received from the customers of Hair Ltd in each of the last three years has been as follows. The income is evenly spread over the 12 months.

In order to encourage small enterprises, the State Council has granted the following tax reliefs:

– Before 1 August 2014, an entity with a turnover of less than RMB20,000 per month was exempt from business tax (BT).

– For the period from 1 August 2014 to 31 December 2018, the exemption threshold was increased to RMB30,000 per month.

Hair Ltd files business tax on a monthly basis.

Required:

(i) Calculate the business tax payable by Hair Ltd in each of the three years, 2012, 2013 and 2014. (4 marks)

(ii) Calculate the enterprise income tax (EIT) of Hair Ltd of 2014. (2 marks)

(b) With respect to the three turnover taxes in China, namely, value added tax (VAT), business tax (BT) and consumption tax (CT):

(i) State which two of the turnover taxes are mutually exclusive. (1 mark)

(ii) Briefly explain the purpose and effect of levying consumption tax. (3 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!