重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

In January 2015, the supermarket sold 2,000 of the offer packs.

What is the amount of value added tax (VAT) charged on the sale of the 2,000 offer packs?

A.RMB14,530

B.RMB17,000

C.RMB20,342

D.RMB23,800

更多“The sales manager of a supermarket has proposed a marketing promotion of selling a pack of”相关的问题

更多“The sales manager of a supermarket has proposed a marketing promotion of selling a pack of”相关的问题

第1题

25%. KINO Ltd has a wholly (100%) owned subsidiary, Company A, set up in Country X.

In 2014, Company A had a profit of USD200,000 and paid enterprise income tax in Country X at the rate of 15% (USD30,000). Company A declared a dividend of USD170,000 and paid this to KINO Ltd after deduction of withholding income tax of 10% (USD17,000).

What is the additional enterprise income tax (EIT) which KINO Ltd will pay on the dividend income received from its subsidiary, Company A?

A.USD25,500

B.USD3,000

C.USD42,500

D.USD0

第2题

Section A – ALL 15 questions are compulsory and MUST be attempted

Which government authorities promulgated the Enterprise Income Tax Law and the Consumption Tax Provisional Regulations?

A.The Standard Committee of the National People’s Congress and the State Council

B.The State Council and the Ministry of Finance

C.The Ministry of Finance and the State Administration of Taxation

D.The State Administration of Taxation and the Standard Committee of the National People’s Congress

第3题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

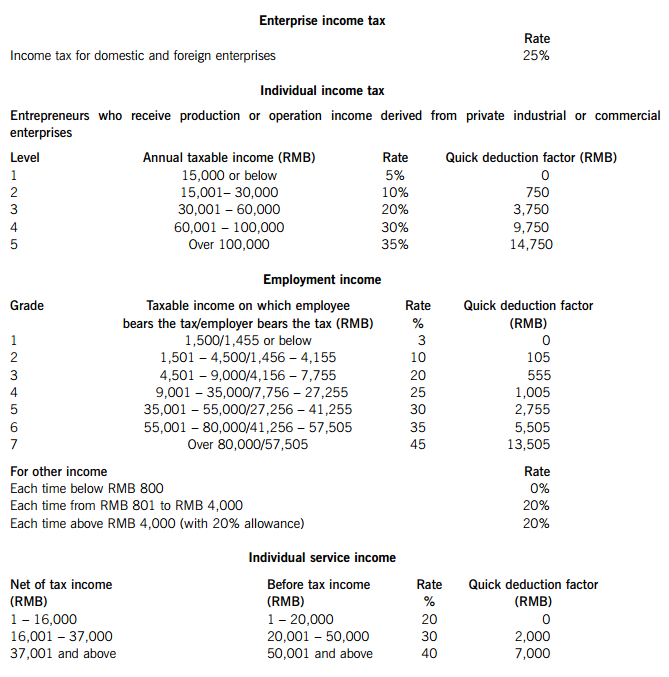

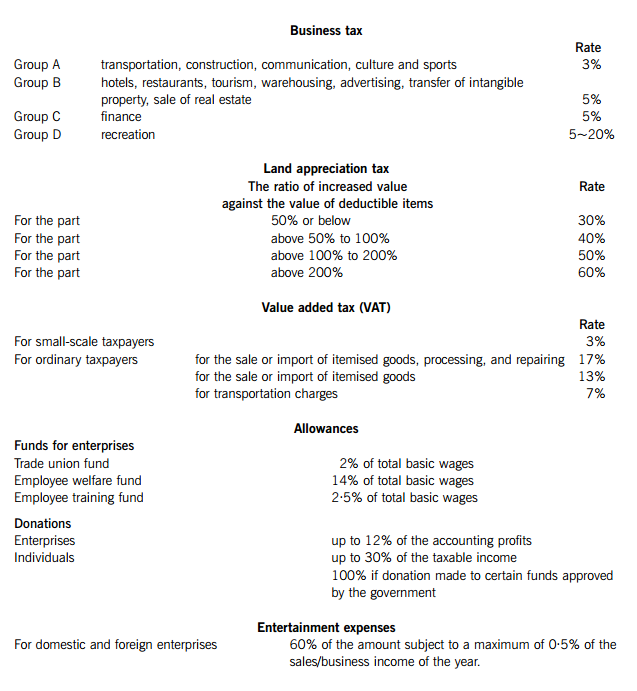

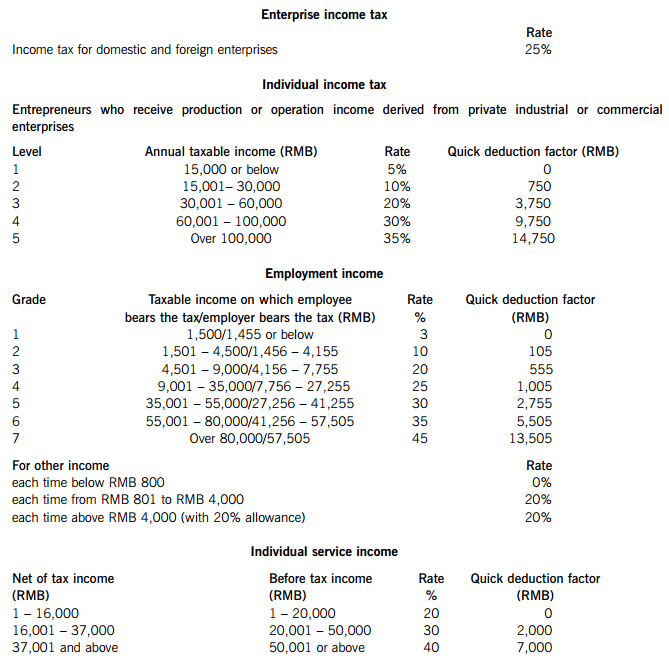

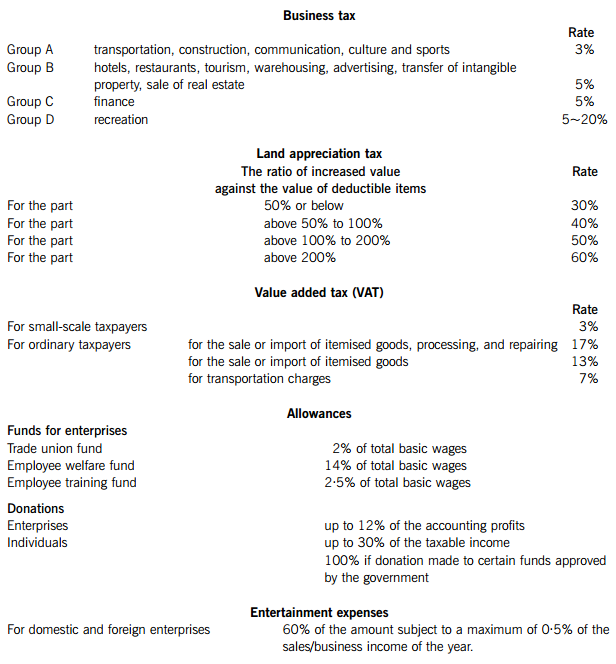

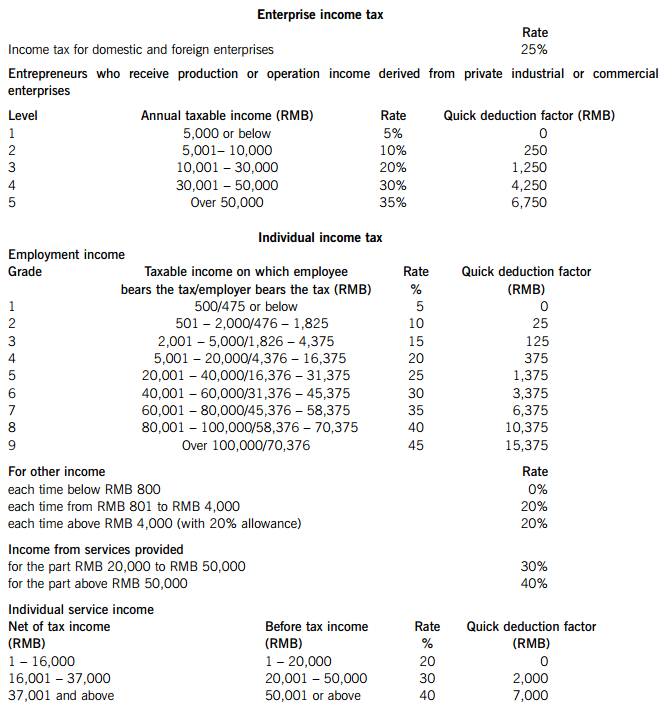

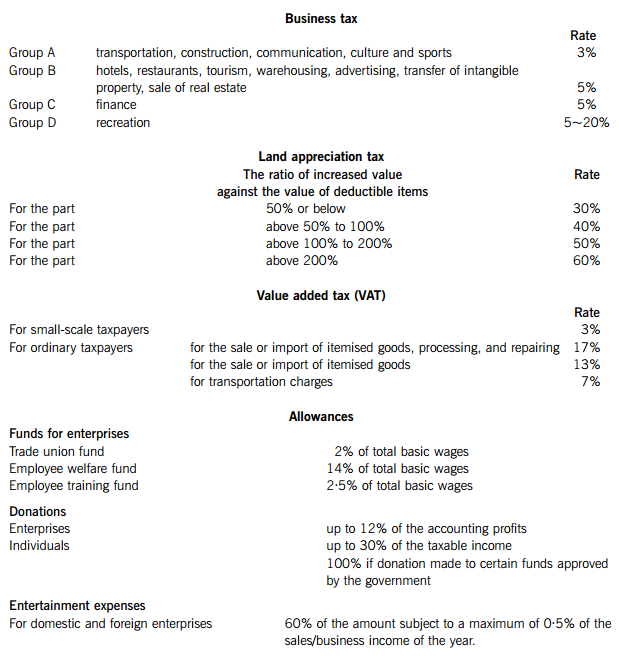

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

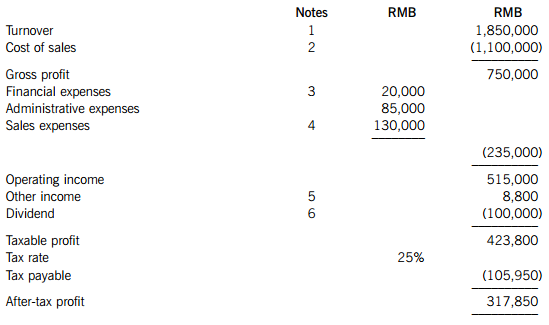

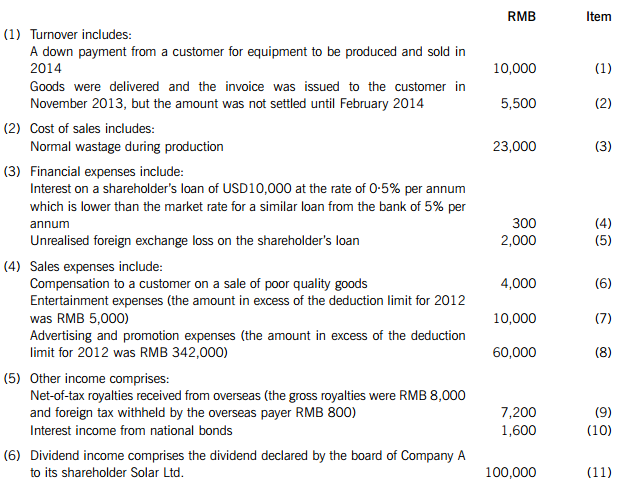

(a) Company A is a foreign investment enterprise set up in China, which manufactures and sells solar power equipment. The only shareholder of Company A is Solar Ltd, a company incorporated in the British Virgin Islands (BVI). The following is a summary of Company A’s income statement for 2013.

Notes:

Required:

(i) Briefly explain the enterprise income tax (EIT) treatment of each of the items identified as (1) to (11). State clearly the items for which no adjustment is required. (13 marks)

(ii) Calculate the correct amount of EIT payable by Company A for the year 2013 starting with the taxable profit of RMB 423,800. (4 marks)

(iii) Calculate the amount of tax to be withheld by Company A from the dividend payable to Solar Ltd. Note: There is no treaty relief between China and the British Virgin Islands (BVI). (1 mark)

(b) An overseas company, P Ltd, provided management services to a China customer for a gross service fee of RMB 100,000. P Ltd is considered as having a China permanent establishment by the tax bureau, which has assessed a deemed profit rate of 50% on the service fee earned by P Ltd.

Required:

(i) Calculate the business tax and enterprise income tax (EIT) payable by P Ltd on the service fee. (3 marks)

(ii) State the circumstances in which the tax authorities can assess the taxable profit of a non-resident enterprise on a deemed basis. (2 marks)

(c) (i) State the FOUR types of tax exempt income for enterprise income tax (EIT) purposes. (4 marks)

(ii) Briefly explain the tax treatment of expenses incurred to earn non-taxable income and tax exempt income. (2 marks)

(d) Company Cap demolished its old factory building and constructed a new one in 2013. The following information relates to these transactions in 2013:

(1) The cost of the old factory building was RMB 400,000 and its net book value as at 1 January 2013 (for both accounting and taxation purposes) was RMB 60,000. The old factory was demolished on 1 January 2013.

(2) Materials were transferred from inventory for the construction of the new factory. The cost of these materials was RMB 90,000 and their selling price was RMB 100,000.

(3) To finance the construction of the new factory, a loan of RMB 500,000 was borrowed from 1 January 2013 at an interest rate of 8% per annum. The loan was repaid on 31 December 2013.

(4) A construction company was engaged to build the new factory with a contract sum of RMB 700,000.

(5) The new factory building was completed on 15 November 2013 and started operations from 16 November 2013.

(6) Company Cap adopted an economic life for the new factory building of 20 years and a residual value of 10%, for both tax and accounting purposes.

Required:

(i) Calculate the cost base of the new factory building for depreciation purposes. (4 marks)

(ii) Calculate the amount of depreciation on the new factory building for 2013. (2 marks)

2.

(a) Mr Chen, a Chinese national, was hired by an IT company in 2012. His employer has proposed the following two alternative remuneration packages both with a total of RMB 300,000 to him for 2013:

Plan 1: A salary of RMB 17,500 each month for 12 months and an annual bonus of RMB 90,000.

Plan 2: A salary of RMB 5,000 each month for 12 months, a special award in June of RMB 120,000 and an annual bonus in December of RMB 120,000.

Required:

Calculate the total individual income tax (IIT) payable by Mr Chen for the year 2013 in respect of each of the two plans.

(b) Ms Li, a Chinese national, earned the following income in 2013.

(1) Coupons for RMB 200 which were given as a result of her bulk buying when she bought groceries from a supermarket for RMB 1,500. She used the coupons to purchase groceries in the next month.

(2) Won a lottery prize of a smart phone with a value of RMB 3,000 from a supermarket. The supermarket has agreed to bear the individual income tax (IIT) payable by the winners.

(3) Received bank deposit interest of RMB 2,000.

(4) Lent Company W RMB 100,000 for a year at an interest rate of 15% per annum.

(5) Wrote a long article for the newspaper, PP Daily, which was published on three days from 1 to 3 February and received a fee of RMB 1,500 for each day.

(6) As the independent non-executive director of a listed company, received a director’s fee of RMB 10,000 each month, i.e. a total of RMB 120,000 for the year.

(7) Received employment income from two separate employments as follows:

– from a retail shop for the period 1 to 15 April, a salary of RMB 2,800; and

– from a restaurant for the period 16 April to 30 April, a salary of RMB 2,500.

Neither the retail shop nor the restaurant withheld any IIT for her.

Required:

Calculate the individual income tax (IIT) payable by Ms Li for 2013 in respect of each of the items of income (1) to (7). State clearly any item(s) which are ‘exempt from IIT’ or ‘not subject to IIT’. (8 marks)

(c) (i) Mr Zhang has a China domicile. In 2013, he was seconded to Hong Kong to work and earned a salary from this Hong Kong employment. After his secondment, he will return to China.

Required: State, giving reasons, whether Mr Zhang will be taxable in China on the salary from his Hong Kong secondment. (2 marks)

(ii) Ms Robin is a model working in the Hong Kong Special Administrative Region. Her Hong Kong employer sent her to China for a fashion show for five days in 2013. She earned a salary from her work at the fashion show. Except for this fashion show, Ms Robin did not spend any time in China in 2013.

Required:

State, giving reasons, whether Ms Robin will be taxable in China in 2013. (2 marks)

(d) Mr Wang is a China tax resident. In 2013, Mr Wang’s only income was employment income of RMB150,000 and his employer withheld the correct amount of individual income tax for him.

Required:

(i) State whether Mr Wang is required to submit an annual individual income tax (IIT) return. (1 mark)

(ii) State the tax filing deadline for the annual IIT return for the year 2013. (1 mark)

3.

(a) Electronic Ltd is a newly set up retail company selling computer accessories. Electronic Ltd’s finance manager prepared the following budget for 2013:

(1) Sales of goods to individual customers at a value added tax (VAT) inclusive price of RMB 780,000.

(2) Purchases of goods from a VAT general taxpayer at a VAT exclusive price of RMB 600,000.

Required:

(i) Calculate the value added tax (VAT) payable by and the gross profit of Electronic Ltd for 2013, if it is a VAT general taxpayer. (3 marks)

(ii) Calculate the VAT payable by and the gross profit of Electronic Ltd for 2013 if it is a small-scale taxpayer. (3 marks)

(b) Clothy Ltd is a factory producing garments for export, it does not have any domestic sales in China. The costs of production of the garments sold by Clothy Ltd in 2013 comprised:

(1) Raw materials of RMB 200,000 purchased for which special value added tax (VAT) invoices were received.

(2) Wages and salaries of RMB 50,000.

(3) Overhead costs for water, electricity, transportation, etc with a total input VAT of RMB 10,000, all of which are supported by valid VAT invoices.

Clothy Ltd had two options for the export of all of the garments produced in 2013:

(i) To export them itself, directly to an overseas customer for a price of RMB 400,000; or

(ii) To sell the garments to a Chinese trading company for a price of RMB 360,000 and the trading company will then export the garments to the overseas customer at a price of RMB 400,000.

The VAT refund rate for garments is 16%.

Required:

(i) Calculate the export value added tax (VAT) refundable to Clothy Ltd for the direct export of the garments. (2 marks)

(ii) Calculate the export VAT refundable to the trading company for the export of the garments purchased from Clothy Ltd. (1 mark)

(c) Toyly Ltd had the following transactions in 2013:

(1) Sold goods for cash-on-delivery in August and the customer paid in September.

(2) Sold goods on credit terms of 30 days after delivery. The goods were delivered in February.

(3) Sent goods on consignment to the consignee in March. The consignee sold the goods in May and passed a statement of the sale to Toyly Ltd also in May.

(4) Sent goods to a branch in another province for sale in November. The branch sold the goods in December.

(5) Received money from Customer X and issued a VAT invoice for the goods in June, but did not deliver the goods until July.

Required:

In the case of each of the transactions (1) to (5), state the month in which Toyly Ltd’s value added tax (VAT) liability will crystallise. (5 marks)

(d) Softko Ltd, a software development company, is a value added tax (VAT) general taxpayer. Softko Ltd had the following transactions in October 2013. All amounts are exclusive of VAT unless stated otherwise.

(1) Paid a software fee of USD2,000 to an overseas supplier. VAT was withheld and paid to the tax bureau.

(2) Purchased ten computers as fixed assets for RMB 100,000. A special VAT invoice was obtained. The computers are used for both taxable and tax exempt services and are used around 20% of the time to provide VAT exempt services.

(3) Paid a software house, which is a small-scale taxpayer, a gross amount of RMB 30,000 inclusive of VAT. A special VAT invoice issued via the tax bureau was obtained.

(4) Hired a coach for transporting its staff from the metro-station to the office for RMB 50,000. A special VAT invoice was obtained.

(5) Acquired a mainframe. computer for RMB 40,000, specifically for the development of some software for an overseas customer. A special VAT invoice was obtained. Softko Ltd has applied for VAT exemption on the export of the software overseas.

Required:

Calculate the input value added tax (VAT) of Softko Ltd for the month of October 2013. Clearly identify any item(s) for which input VAT is not creditable and state the reason. (6 marks)

4.

(a) The following transactions were undertaken by the persons indicated in 2013:

(1) A university set up by the local government received tuition fees of RMB 170,000 from students studying for bachelor degrees.

(2) A property developer sold used computers for RMB 20,000.

(3) A factory received rent of RMB 48,000 from sub-leasing an unused area.

(4) A trading company received bank interest income of RMB 10,000.

(5) A trading company received interest income of RMB 38,000 from lending to another company.

(6) A construction company provided construction services for RMB 500,000.

(7) The government transferred a land use right to a property developer for RMB 26,000,000.

(8) A company used a trademark valued at RMB 320,000 as a capital contribution to another company.

(9) A hotel charged a customer a total fee of RMB 1,300, of which RMB 100 was for the soft drinks from the refrigerator.

(10) A son received a villa valued at RMB 2,000,000 from his father’s estate.

(11) A property management company received a total of RMB 24,000 from tenants, of which RMB 12,000 was for the allocation of electricity and water costs to the tenants and RMB 8,000 was for the salaries of the guards.

Required:

In each of the cases (1) to (11), calculate the business tax payable where relevant, and where not relevant, state clearly whether the transaction is ‘subject to VAT instead of business tax’ or ‘exempt from business tax’ or ‘not subject to business tax’.

Note: Marks will not be given for stating ‘not taxable’. (11 marks)

(b) Cosmet Ltd, produces and sells cosmetics. Currently, Cosmet Ltd makes three standard types of goods with selling prices and costs as follows. All amounts are stated exclusive of value added tax (VAT).

In December 2013, Cosmet Ltd had the following transactions:

(1) Sold 4,200 sets of a pack containing rouge with a lipstick at a price of RMB 100 for each set.

(2) Sold 1,000 sets of hand cream with a lipstick at a price of RMB 50 for each set.

(3) Gave 100 pieces of lipstick to participants during the company’s annual dinner.

(4) Purchased 3,000 pieces of rouge from another factory at RMB 30 each and sold 2,500 of these purchased pieces at the same selling price as for its own rouge of RMB 80 each.

Required:

For each of the transactions (1) to (4), calculate the consumption tax payable by Cosmet Ltd or state clearly if the transaction is ‘not subject to consumption tax’. (4 marks)

5.

(a) State the FIVE methods which the tax authorities can use to carry out a special tax adjustment (transfer pricing adjustment) where a transaction is not conducted at arm’s length. (5 marks)

(b) Company D underpaid its enterprise income tax (EIT) for the year 2012 by RMB 230,000 because it overstated its deductible expenses by using fraudulent invoices for its annual tax filing. The tax bureau discovered the overstatement of expenses and considered it as an act of tax evasion and imposed a penalty on Company D. Company D settled the underpaid tax on 31 July 2013.

Required:

(i) Calculate the amount of late payment surcharge which Company D would have had to pay when it settled the underpaid tax on 31 July 2013. (2 marks)

(ii) State the range of penalties which the tax bureau could have imposed on Company D. (1 mark)

(c) The accountant of Company E wrongly typed income of RMB 10,000 as RMB 100,000 in the company’s tax return for February 2008 and as a result Company E overpaid its business tax by RMB 4,500.

Required:

State, giving reasons, whether Company E can obtain a refund of the business tax overpaid from the tax bureau in 2014. (2 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第4题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

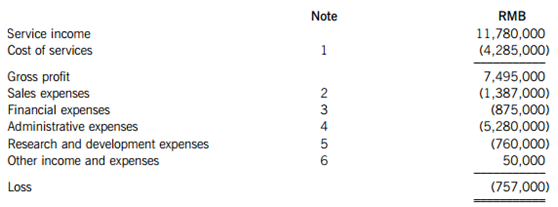

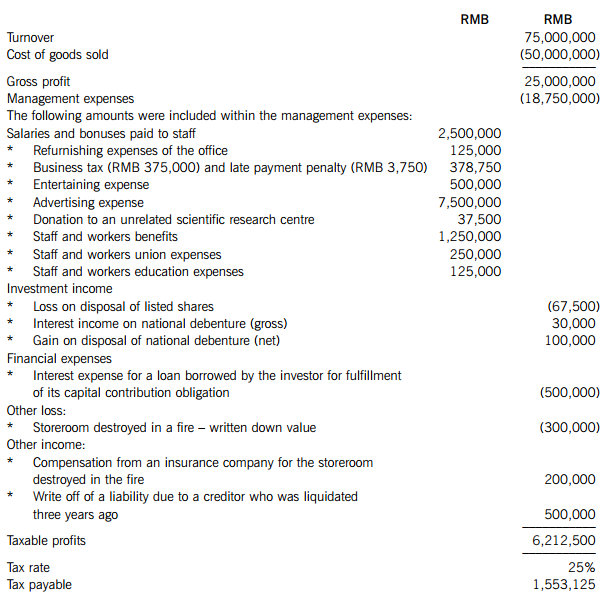

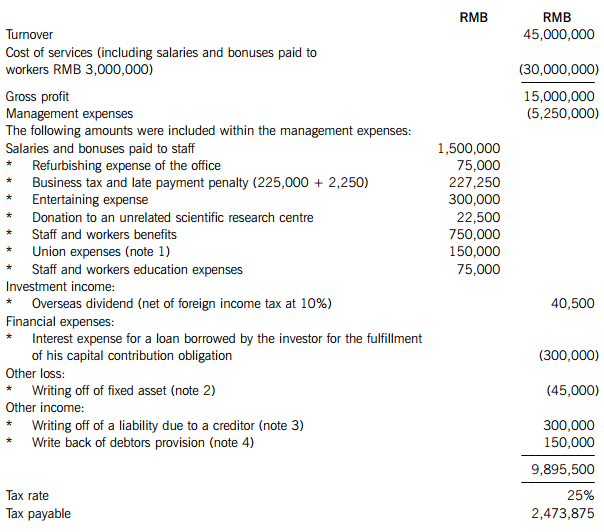

(a) Company B is a limited liability company set up on 1 January 2013. Company B is engaged in the provision of information technology and data processing services. The company’s accountant has prepared the following tax computation for the year ended 31 December 2013:

Notes:

(1) The cost of services includes wages and salaries of RMB 2,900,000, of which RMB 500,000 relates to the accrued portion of a bonus due and payable to a member of senior management on the termination of his contract in 2017.

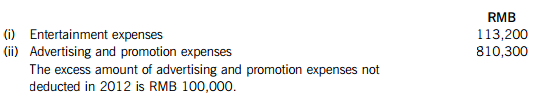

(2) Sales expenses include:

(3) Financial expenses include RMB 40,000 of interest paid on a shareholder’s loan. The interest rate on this loan is 5% p.a. which is the same as the market interest rate on loans on similar terms from banks.

(4) Administrative expenses include:

(5) Research and development (R&D) expenses include RMB 320,000 which has been registered with the tax bureau and agreed as qualifying for the tax incentives on R&D expenses.

(6) Other income and expenses comprise:

Required:

(i) Briefly explain the enterprise income tax (EIT) treatment of each of the 14 items referred to in notes (1) to (6). (17 marks)

(ii) Calculate the correct amount of EIT payable by Company B for the year 2013, starting with the loss of RMB 757,000 and clearly identifying those items which do not require any adjustment. (8 marks)

(b) Company H is a Hong Kong company which has set up a representative office (RO) in China. The RO provides liaison services in China for Company H. The China tax authorities have assessed the tax position of the RO and concluded that the RO should pay tax on a cost-plus basis at a deemed profit rate of 15%. In 2013 the taxable costs of the RO are RMB 160,000.

Required:

Calculate the business tax (BT) and enterprise income tax (EIT) of the representative office (RO) for the year 2013. (3 marks)

(c) Briefly explain the principle of ‘effective management’ used to determine whether an enterprise registered outside China can be considered as a China tax resident. (3 marks)

(d) State any FOUR circumstances in which the tax authorities can assess an enterprise’s liability to enterprise income tax (EIT) using the deemed basis. (4 marks)

2.

Ms Chen, a Chinese national, received the following income in 2013.

Income from her employment as a manager with Company X:

(1) A salary of RMB 10,000 per month for each of the 12 months of 2013. In addition, she was entitled to the following subsidies and allowances in 2013:

(a) A meal allowance of RMB 500 per month.

(b) Overtime income of RMB 1,000 per month.

(c) Reimbursement of business trip expenses in January 2013. The amount incurred was RMB 1,200 and the whole amount was supported with invoices.

(d) Employer’s mandatory contribution to social security of RMB 1,200.

(2) A year-end bonus of RMB 40,000 in December 2013.

Other income:

(3) She had an article published in a magazine in June and republished in July. The authorship fee was RMB 3,000 for each publication.

(4) In June, a private limited company paid her a dividend from which it withheld individual income tax (IIT). The net-of-tax dividend she received was RMB 40,000.

(5) In April 2013, she invested RMB 20,000 in A-shares and sold them for RMB 35,000 in August 2013.

(6) She has provided consultancy services to a Canadian company and received a gross service fee of USD20,000. Canadian tax of USD2,000 was withheld and deducted at source from this fee.

(7) Her uncle in France died in 2013 and she inherited an estate worth USD1,000,000.

(8) An advertising company used Ms Chen’s photo and image in an advertisement and paid her a fee of RMB 100,000. She decided to donate RMB 15,000 of this fee to an approved charitable organisation specifically for the earthquake in Sichuan. The donation was paid directly to the charity from the advertising company.

(9) She received net-of-tax interest from a private company of RMB 4,800. Individual income tax and business tax were withheld and deducted by the company before paying this interest.

Required:

(a) Calculate the individual income tax (IIT) payable by Ms Chen in respect of each of the items (1) to (9), clearly identifying any item(s) which are tax exempt.

Note: You should ignore the effect of business tax and surtaxes on business tax in respect of items (6) and (8) and surtaxes on business tax in respect of item (9). (16 marks)

(b) (i) State the penalty which will be levied on the publisher for not withholding IIT from the payment made to Ms Chen (item (3)). (1 mark)

(ii) Explain Ms Chen’s responsibilities for filing and paying the IIT on this fee. (3 marks)

3.

(a) Company T, an accountancy firm in Shanghai, is a value added tax (VAT) general taxpayer. Company T’s transactions for the month of November 2013 included the following:

(1) Provided book-keeping services to Client A and billed a fee of RMB 30,000 and outlays of RMB 1,000.

(2) Billed Client B RMB 40,000 inclusive of VAT for audit services provided.

(3) Sent a bill to Client Z on 1 November for RMB 100,000. As Client Z settled the bill before the end of November, Company T granted it an early payment discount of RMB 1,000.

(4) Provided consultancy services to a German client for a fee of RMB 80,000. These services qualified as an export of services.

(5) Engaged a law firm to provide legal advisory services and received a VAT invoice for fees of RMB 15,000.

(6) Paid a trademark fee to a global firm in the USA of RMB 50,000. VAT was withheld and paid by Company T.

(7) Bought computers for RMB 20,000 and obtained a VAT general invoice. (8) Paid RMB 5,000 for the repair of the computers. The repair company was a small-scale taxpayer and issued a general invoice to Company T.

(9) Paid rent to its landlord of RMB 60,000. A business tax invoice was obtained.

(10) Paid a transportation fee of RMB 2,000 for picking up its staff from the metro station and bringing them to its office. A VAT invoice at 11% was obtained.

(11) Provided free-of-charge audit services to a charitable organisation. The market value of these services was RMB 35,000.

(12) Paid leasing charges of RMB 6,000 for a photocopying machine. A VAT invoice was obtained.

Except where stated otherwise, all amounts are exclusive of VAT.

Required:

(i) In respect of Company T’s transactions for November 2013, state, giving reasons, those transactions on which value added tax (VAT) will not be charged or for which a VAT credit will not be allowed. (5 marks)

(ii) Calculate the VAT payable by Company T for the month of November 2013 as a result of transactions (1) to (12). (9 marks)

(b) Company M is a production company manufacturing lighting products for exportation. The company’s transactions for December 2013 are as follows:

(1) Exported goods at a FOB (freight on board) price of RMB 200,000.

(2) Sold goods domestically in China for RMB 180,000.

(3) Imported materials at a CIF (cost including insurance and freight) value of RMB 12,000. The import customs duty rate was 10%.

(4) Purchased raw materials for RMB 160,000. A bulk purchase discount of RMB 10,000 was deducted directly in the VAT invoice obtained.

(5) Paid transportation costs of RMB 10,000. A VAT invoice at 11% was obtained.

Except where stated otherwise, all amounts are exclusive of VAT.

Required:

(i) Calculate the amount of irrecoverable input value added tax (VAT) on the exported goods. Note: The export refund rate is 13%. (1 mark)

(ii) Calculate the VAT payable by Company M for the month of December 2013. (5 marks)

4.

(a) Company S sells cosmetics, its transactions in October 2013 were as follows:

(1) Imported 300 sets of cosmetics packs at a CIF (cost including insurance and freight) value of USD100 per set. The import customs duty rate was 10%.

(2) Purchased 1,000 pieces of lipstick at RMB 10 per piece from a manufacturing company, Company W.

(3) Purchased chemicals for the production of cosmetics packs from Company L for RMB 123,000.

(4) Sold 200 sets of the imported cosmetics packs at RMB 1,500 per set without further processing.

(5) Sold 600 pieces of lipstick at RMB 50 per piece without further processing.

(6) Sold 450 sets of self-produced cosmetics packs at RMB 1,000 per set.

All amounts are stated exclusive of VAT.

Required:

(i) Calculate the consumption tax (CT) paid by Company S on the importation of the cosmetics sets (item (1)). (2 marks)

(ii) State clearly whether the sales of goods in each of items (4), (5) and (6) are or are not subject to CT. (3 marks)

(iii) Calculate the CT payable by Company S on its sales for the month of October 2013. (1 mark)

Note: The consumption tax rate on cosmetics is 30%.

(b) In July 1998, Company P acquired an office for self-use, comprising one floor in a multi-storey building, for RMB 3,000,000. In December 2013, Company P sold the office for RMB 20,000,000. The appraised value of the office was RMB 15,000,000.

The taxes payable on the sale of the property were: business tax (BT); city maintenance and construction tax and education levy of 10% on the BT; and stamp duty of 0·05% on the sales contract.

Required:

Calculate the land appreciation tax (LAT) payable by Company P on the sale of the office. (5 marks)

(c) A retail shop, Shop R, sells air-conditioners to customers for RMB 2,000 each; at the same time Shop R charges a RMB 100 installation fee.

Required:

State, giving reasons, whether Shop R should pay business tax (BT) or value added tax (VAT) on the installation fee. (4 marks)

5.

(a) (i) Define the term ‘tax evasion’ as provided for in the Tax Collection and Administration Law. (3 marks)

(ii) State the statute of limitation on the recovery of taxes in the case of tax evasion. (1 mark)

(b) During a tax audit of Company A, it was discovered that it had committed the following acts:

(1) Deducted expenses of RMB 250,000 which were not related to its business operations.

(2) Sold goods to a related company for RMB 500,000 when the open market selling price of the similar type of goods was RMB 2,000,000.

Required:

Explain whether either or both of the acts committed by Company A constitutes tax evasion, and if not, state how the issue will be classified. (2 marks)

(c) State the actions which the taxpayer can take if there is a dispute on the amount of tax assessed by the tax authorities and by when such action should be taken. (4 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第5题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

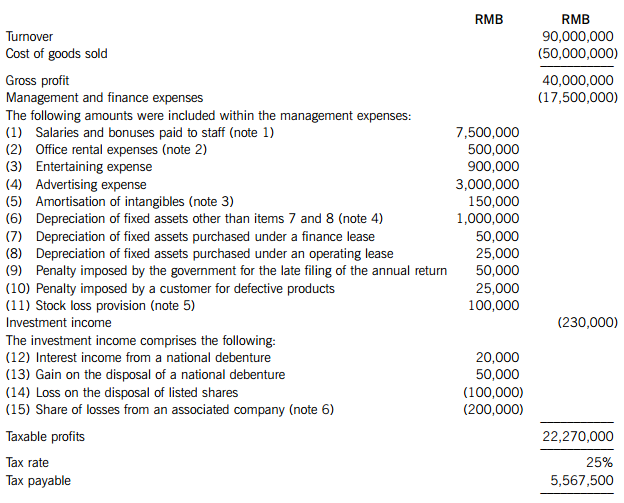

(a) Company Y is a manufacturing joint venture enterprise, which was established and started operations on 1 January 2011.

The statement of enterprise income tax (EIT) payable prepared by the accountant of Company Y for the year 2011 is as follows:

Notes:

(1) This amount includes bonuses of RMB 300,000 paid in December 2011.

(2) The office rental expense comprises a lump sum rental payment made for a period of two years from 1 July 2011.

(3) The amortisation of a self-developed brand name according to an independent valuer’s report.

(4) This amount includes depreciation of RMB 100,000 for a machine which was unused for the whole of 2011 because of a water flood.

(5) The provision is calculated at 5% of the closing stock value. (6) This loss represents Company Y’s share of the losses incurred by an associated company calculated under the equity accounting method.

Required:

(i) Explain the correct treatment of each of the items (1) to (15) of management expense and investment income included in the income tax calculation prepared by Company Y’s accountant; (16 marks)

(ii) Calculate the correct amount of enterprise income tax (EIT) payable by Company Y for the year 2011. (5 marks)

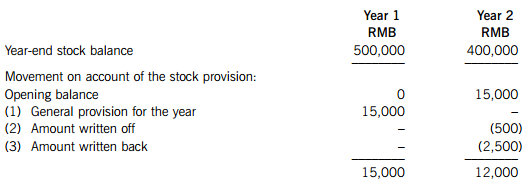

(b) Company C is a manufacturing foreign invested enterprise which commenced business two years ago. It has an accounting policy of making a general provision for obsolescence equal to 3% of its year-end stock balance.

Details of the movements in this provision for the two years since the commencement of Company C’s business are as follows:

Required:

Briefly explain the tax treatment of the items identified as (1), (2) and (3) comprising the movements in the provision in years 1 and 2. (4 marks)

(c) Briefly explain the enterprise income tax (EIT) treatment of the interest expense in each of the following cases:

(i) Interest incurred on a loan used for the purchase or construction of fixed assets prior to the assets being put into use; (1 mark)

(ii) Interest paid between operational units within a non-financial enterprise; (1 mark)

(iii) Interest incurred on a related party debt. (2 marks)

(d) Define the term ‘intangible assets’ for tax purposes and state the valuation bases used initially for such assets and their subsequent tax treatment. (6 marks)

2.

(a) Mr Chang, a Chinese citizen, is a university professor. He had the following income for the month of January 2012:

(1) Monthly employment income of RMB 16,000 and a bonus for the year 2011 of RMB 36,000.

(2) A dividend of RMB 10,000 received from an unlisted company.

(3) A translation fee of RMB 5,000 from a book publisher.

(4) Interest income of RMB 5,200 derived from Government bonds.

(5) Provided a patent to an overseas enterprise and received RMB 80,000. He paid RMB 7,000 individual income tax in the source country according to the tax rules of that country.

(6) Published a book and a series in a newspaper, and received income of RMB 60,000 and RMB 4,000 from the book publisher and newspaper respectively.

(7) Income of RMB 4,800 (net) received from selling certain listed shares on hand.

(8) Income of RMB 30,000 (gross) earned from proof reading the English translation version of a literary work.

(9) Sold a real property for RMB 700,000, which he had acquired two years earlier for RMB 400,000. He paid the relevant business tax on the sale, plus RMB 8,000 to the real estate agency which had handled the sales transaction. (Ignore any land appreciation tax (LAT) implications of this transaction)

Required:

Calculate the individual income tax (IIT) payable by Mr Chang for the year 2012, clearly identifying any amounts which are tax exempt.

Note: The monthly personal allowance for a Chinese local is RMB 3,500. (14 marks)

(b) Briefly explain the individual income tax (IIT) treatment of each of the following transactions and calculate the tax payable (if any) by Mr A, Mr B and Mr C:

(i) Mr A is one of the investors in a limited company, Company J. During the year, Company J bought a car for RMB 300,000 for Mr A’s personal use. Mr A is the registered owner of the car; (2 marks)

(ii) Mr B is one of the investors in a limited company, Company K. During the year, Company K lent RMB 300,000 to Mr B so he could buy a car for his personal use; (2 marks)

(iii) Mr C is the sole owner of private enterprise L. During the year, enterprise L bought a car for RMB 300,000 for Mr C’s personal use. Mr C is the registered owner of the car. (2 marks)

3.

(a) Company P manufactures fans. The standard selling price per fan, net of value added tax (VAT), is RMB 80 each.

For the month of May 2012, the following sales were made and the VAT on the goods sold was recorded by the company accountant:

(i) Sale of 10,000 fans to a supermarket at RMB 76 each; this price is net of a discount of 5% because of the large volume. RMB 700,000 was received to settle the transaction, which was net of a cash discount of RMB 60,000.

Output VAT: RMB 700,000 x 17% = RMB 119,000

(ii) Sale of 100 (new) fans, partly paid for by the trade-in of 100 old fans, resulting in a net sales value of RMB 50 each. The old fans were used as a staff benefit.

Output VAT : 100 x RMB 50 x 17% = RMB 850

(iii) Sale of 10,000 fans to a wholesaler at RMB 80 each. As a part of the contract terms, Company P agreed to pay back the whole consideration of RMB 800,000 to the wholesaler, at the end of four years.

Output VAT: RMB 800,000/4 years x 17% = RMB 34,000

(iv) Exchanged 1,000 fans for raw materials with a market value of RMB 68,000, for use in production.

Output VAT: RMB 68,000 x 17% = RMB 11,560

All amounts are stated excluding VAT.

Required:

Calculate the correct value added tax (VAT) output and input arising from items (i) to (iv), clearly explaining the treatment applied in each case. (9 marks)

(b) A trading company, Company W, imported some goods costing USD 2 million. The additional costs of importing these goods were ocean freight of USD 40,000, an ocean insurance premium of USD 4,000, inland transportation and customs declaration fees of USD 20,000 and a middle-man agent fee of USD 2,000.

All amounts are stated excluding VAT.

Required:

Calculate the customs duty and value added tax (VAT) on the importation of the goods, stating by when they must be paid.

Notes:

1 The exchange rate is USD 1 to RMB 6.

2 The customs tariff rate is 30%. (4 marks)

(c) (i) Briefly explain the criteria used to determine the status of a small value added tax (VAT) payer and its tax implication; (5 marks)

(ii) Calculate the VAT payable by a small scale VAT payer who sold goods for RMB 20,600 and a used car for RMB 46,350 in February 2012. (2 marks)

4.

Company M, a cigarette company, had the following transactions in the month of January 2012:

(1) Bought tobacco for RMB 250,000 (including value added tax (VAT) and consumption tax (CT)) from a commercial supplier who is a general VAT payer.

(2) Bought tobacco for RMB 40,000 (invoice value) from a local farmer and paid the related transportation cost of RMB 20,000 (invoice value).

(3) Subcontracted the tobacco in (2) to an outside subcontractor, Company N, and paid the fee of RMB 90,000 (including VAT) stated in the VAT invoice received from Company N.

(4) Received goods back from the subcontractor in (3), but Company N had not paid the related CT on Company M’s behalf.

(5) 50% of the goods in (1) and (4) were used in production during the month of January 2012.

(6) Sold 20,000 cases of cigarettes for RMB 40 million (excluding VAT).

(7) Distributed four cases of cigarettes for staff welfare.

Required:

(a) Calculate the value added tax (VAT) liability of Company M for the month of January 2012. (7 marks)

(b) Calculate the consumption tax (CT) liability of Company M for the month of January 2012. (7 marks)

(c) Calculate the consumption tax (CT) liability of Company N, if any, for the month of January 2012. (1 mark)

Note: The CT rate for tobacco is 30% and for cigarettes is RMB 160 per case plus 45% of turnover. (15 marks)

5.

(a) Define the term ‘controlled foreign subsidiary’ and briefly explain the tax treatment of the profits of such an enterprise in the context of the special tax adjustment pursuant to the enterprise income tax law and rules. (5 marks)

(b) (i) Briefly explain when the tax authority can make a special tax adjustment in respect of transactions between related parties; (2 marks)

(ii) Briefly explain the interest levy applicable in the case of a special tax adjustment. (3 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第6题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

(a) Company L is a manufacturing joint venture enterprise which was established and started operations on 1 January 2010. The statement of enterprise income tax (EIT) payable prepared by the accountant of Company L for the year 2011 is as follows:

Required:

(i) Briefly comment on the correctness of the accountant’s treatment of the 15 items marked with an asterisk (*); (15 marks)

(ii) Calculate the correct amount of enterprise income tax (EIT) payable by Company L for the year 2011. (8 marks)

(b) State under what circumstances a company intending to launch a sales promotion involving the giving of gifts to its individual customers is/is not required to withhold the individual income tax (IIT). (7 marks)

(c) Company L is considering the following two alternatives for launching a sales promotion.

(i) An individual customer will get a gift with a market value equal to RMB100 (cost of purchase RMB80) for free if he/she has accumulated purchases within any single business day of RMB1,000 during the sales promotion period.

(ii) An individual customer will get a gift with a market value equal to RMB200 (cost of purchase RMB100) for free if he/she wins the lottery. A customer will be able to join the lottery for one time when he/she has accumulated purchases within any single business day of RMB1,000 during the sales promotion period.

Required:

Calculate the enterprise income tax (EIT) and individual income tax (IIT), if any, payable for each of the alternatives, assuming that Company L will bear any IIT due.

The following mark allocation is provided as guidance for this requirement:

(i) 2 marks

(ii) 3 marks

2.

(a) Mr Huang, a Chinese national, is the technical officer of Company J. He had the following receipts in the year 2011:

(1) In April, he provided technical services to an enterprise and received RMB 30,000. The related individual income tax was borne by the enterprise.

(2) Mr Huang together with three other people jointly started a partnership with equal shares on 1 October 2011. The profits of the partnership were RMB 300,000 in 2011.

(3) A net gain of RMB 18,000 from trading in the A-shares market.

(4) Euro 10,000 of income received in Country G for the transfer of a patent. Individual income tax equivalent to RMB 15,000 was paid in Country G.

(5) During his visit to Country K, he was invited to give a lecture in a university and was paid income of USD 1,500. Individual income tax equivalent to RMB 1,800 was paid in Country K.

(6) Received RMB 17,000 as insurance compensation.

(7) He won a lottery prize of RMB 30,000, but donated half of this amount to an approved charity.

Required:

Calculate the individual income tax (IIT) payable on each of the items (1) to (7) received by Mr Huang for the year 2011. Clearly state if any of the items of income are exempt from IIT.

Note: the following exchange rates are to be used:

Euro: RMB – 1:9·5

USD: RMB – 1:7 (10 marks)

(b) (i) Briefly explain the individual income tax (IIT) treatment of an annual one-off bonus where the IIT payable is partly borne by the employer as:

(1) a fixed amount; and (1 mark)

(2) a percentage of the IIT payable. (3 marks)

(ii) Company B is considering awarding an annual one-off bonus of RMB 100,000 to its general manager with the IIT being partly borne by the company. The general manager’s normal monthly salary exceeds the monthly deduction.

Required:

Calculate the individual income tax (IIT) payable and the amount to be borne by the general manager (as employee) if:

(1) Company B bears the fixed amount of RMB 20,000 of the total IIT payable by the general manager; and

(2) Company B bears 20% of the total IIT payable by the general manager. (6 marks)

3.

(a) Company M, a coal company, had the following transactions in the month of March 2011:

(1) Bought an excavator for RMB 720,000 plus value added tax (VAT) of RMB 122,400 and paid the related transportation fee of RMB 48,000 (invoice value).

(2) Bought low-value consumption goods for RMB 96,000 plus VAT of RMB 6,720.

(3) Sold 10,000 tons of coal by instalment to a customer for RMB 600 per ton (excluding VAT). One quarter of the payment was due in the month, but only RMB 1,000,000 (excluding VAT) was received. Separately RMB 72,000 was paid for transportation relating to the delivery.

(4) 250 tons of coal was used to provide heating for the staff dormitory and 600 tons of coal was given to customers as gifts.

(5) Sold 150 thousand cubic metres of natural gas acquired while mining for RMB 300,000 (excluding VAT).

Required:

Calculate the value added tax (VAT) liability of Company M for the month of March 2011. (6 marks)

(b) Define ‘Small-scale taxpayer’ for value added tax (VAT) purposes and state how their VAT liability is calculated and the type of VAT invoices they should use. (4 marks)

(c) Company N, a construction company, had the following transactions in the month of March 2011:

(1) Signed a contract with a metal company to build a factory. Partial payment of RMB 9,600,000 was received when the contract was signed. 15% of the building was constructed at the end of the month.

(2) Signed a contract with a country club for laying cables. The contract sum was RMB 1,200,000 which included the value of the cables provided by the country club of RMB 200,000. The job was finished and the money was received before the end of the month.

(3) Signed a contract with a metro company to provide mud engineering services and received RMB 2,000,000.

(4) Signed a contract with a supermarket for decoration services, including labour costs of RMB 450,000, management fees of RMB 50,000 and material costs of RMB200,000. The supermarket provided an additional RMB 150,000 of materials.

(5) Sold a self-constructed house to a member of staff for RMB 1,500,000, plus a gas pipe installation fee of RMB 10,000 and building repair funds of RMB 150,000. The cost of the building construction was RMB 600,000. The profit ratio for the construction as set by the local tax bureau is 20%.

Required:

Calculate the business tax payable by Company N for each of the transactions (1) to (5) relating to the month of March 2011.

(d) State how the tax bureau may assess business tax on service income if it considers the income declared to be too low and without proper justification and list the methods that may be used. (4 marks)

4.

(a) A trading company, Company S, imported some cosmetic goods costing USD 1,680,000. The additional costs of importing these goods were freight and insurance charges of USD 252,000, customs handling fees of USD 140,000 and a service fee to an overseas agent of USD 28,000.

Company S repacked the cosmetic goods into 10,000 sets for sale in China. 9,000 sets were sold to a wholesaler for USD 6,000,000 and 1,000 sets were sold by retail for USD 900,000. Both these sales figures include value added tax (VAT).

Required:

(i) Calculate the consumption tax, customs duty and value added tax (VAT) payable on the importation of the cosmetic goods; (5 marks)

(ii) Calculate the consumption tax and VAT payable on the sale of the cosmetic goods. (5 marks)

Notes:

(1) The customs tariff rate is 40%

(2) The consumption tax rate for cosmetic goods is 30%

(3) The USD:RMB exchange rate is 1:7·5

(b) List the methods by which Customs may assess the dutiable value of an import if it considers the value declared to be too low and without proper justification. (5 marks)

5.

Company C and its overseas branch, Branch D, both started business in 2010. Company C had a taxable loss of RMB 1,000,000 for the year 2010 and income of RMB 3,000,000 for the year 2011, while Branch D had taxable income of RMB 1,000,000 and paid foreign tax of RMB 300,000 for each of the years, 2010 and 2011. Both Company C and Branch D are subject to an income tax rate of 25%.

Required:

(a) In relation to foreign tax paid by a Chinese taxpayer, state the general tax treatment and the limitations on the amount of credit available. (3 marks)

(b) Calculate the enterprise income tax (EIT) payable by Company C for each of the years 2010 and 2011, clearly identifying the foreign tax credit used in each year and the unused tax credit carried forward, if any. (5 marks)

(c) Briefly explain the EIT provisional and annual filing requirements for a domestic registered enterprise with branches registered in different regions in China. (2 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第7题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. Apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

(a) The following is the statement of enterprise income tax (EIT) payable prepared by the accountant of Company P for the year 2010:

Notes:

(1) The union has not yet been set up and the expense is a general provision.

(2) The original cost of the fixed asset was RMB 150,000 and the accumulated depreciation was RMB 105,000, while the accumulated tax allowances claimed were RMB 120,000.

(3) The creditor had been liquidated three years ago.

(4) Last year (2009) was the first year a debtors provision was made. A general provision of RMB 500,000 was made but the whole amount was disallowed by the tax bureau. This year the management decided to write back part of provision amounting to RMB 150,000.

Required:

(i) Briefly comment on the correctness of the accountant’s treatment of the 12 items marked with an asterisk (*) in the income tax calculation sheet; (17 marks)

(ii) Calculate the correct amount of enterprise income tax (EIT) payable by Company P for the year 2010. (6 marks)

(b) Briefly explain the term ‘arm’s length principle’ in the context of transactions between associated enterprises pursuant to the enterprise income tax law, together with the adjustment methods that may be used by the tax bureau in cases where this principle is not complied with. (6 marks)

(c) Company C, a limited company with equity of RMB 1,000,000, borrowed two loans from related companies:

– RMB 1,000,000 at a 7% annual interest rate from Company A; and

– RMB 2,000,000 at an 8% annual interest rate from Company B.

The market interest rate for the equivalent loans is a 6% annual interest rate.

In 2010, the interest paid to Company A and Company B was RMB 70,000 and RMB 160,000 respectively. The total amount of interest of RMB 230,000 was allocated RMB 140,000 to interest expense and RMB 90,000 to construction in progress in Company C’s accounts.

Required:

Calculate the amount of interest that will be disallowed for enterprise income tax under each of the account headings: interest expense and construction in progress. (6 marks)

2.

(a) Mr Y, a local Chinese national, a professional writer and artist, had the following income during 2010:

(1) Received income of RMB 45,000 for publishing the first edition of a book, and of RMB 15,000 for the second edition of the same book. The book was also published in a newspaper and he was paid RMB 5,250 for this.

(2) Sold one of his paintings for RMB 5,400.

(3) Gave a speech and was paid RMB 28,500.

(4) Acted as a translator for a movie and was paid RMB 60,000.

(5) Gave a speech in overseas country M and was paid the gross equivalent of RMB 27,000, from which the equivalent of RMB 6,750 in overseas tax was deducted at source.

(6) Sold one of his paintings in overseas country H, and was paid the gross equivalent of RMB 15,000, from which the equivalent of RMB 2,250 in overseas tax was deducted at source.

(7) Received interest of RMB 7,500 on a loan he had made to a domestic enterprise.

Required:

(i) Calculate the individual income tax (IIT) payable by Mr Y in respect of each of the items (1) to (7); (12 marks)

(ii) State how and when any IIT due on Mr Y&39;s overseas income will be reported and paid. (3 marks)

(b)

(i) State when a withholding agent must report and pay the individual income tax (IIT) deducted on a monthly basis from employment income; (1 mark)

(ii) List ANY FOUR situations in which an individual taxpayer needs to do self-reporting for IIT purposes. (4 marks)

3.

(a) Enterprise G, a general value added tax payer incorporated in Shenzhen for more than 20 years, had the following transactions in the month of May 2010. Some of the enterprises sales are subject to the standard value added tax (VAT) rate, while others are exempt (VAT) activities. All figures are stated including any applicable VAT:

(1) Sold product A (a standard VAT rate item) for RMB 400,000 and product B (a VAT exempt item) for RMB 350,000.

(2) In addition to the sales in (1) above, distributed product A with a market value of RMB 20,000 for staff welfare benefit.

(3) Purchased RMB 500,000 production materials, of which RMB 50,000 was used for a self-constructed building.

(4) Purchased RMB 200,000 agriculture product, of which RMB 20,000 was used for staff welfare benefit.

(5) Purchased a production machine for RMB 100,000 and sold a used machine for RMB 10,000. The used machine had been bought in May 2009 and used by the enterprise ever since then.

Required:

Calculate the value added tax (VAT) payable by Enterprise G for the month of May 2010. (7 marks)

(b) Enterprise H, a small-scale value added tax payer, had the following transactions in the month of May 2010. All figures are stated including VAT:

(1) Sold product for RMB 20,000.

(2) Purchased RMB 500,000 of production materials.

(3) Purchased a production machine for RMB 100,000 and sold a used machine for RMB 10,000. The used machine had been bought in May 2009 and used by the enterprise ever since then.

Required:

Calculate the value added tax (VAT) payable by Enterprise H on each of the above transactions, giving brief explanations of their treatment. (4 marks)

(c) Company X, a property developer, had the following transactions in 2010:

(1) Donated a new building to a high school. The cost of construction of the building was RMB 500,000 and the deemed profit rate is 10%.

(2) Contributed an office building as part of a capital contribution. The cost of the building was RMB 600,000 and the market value RMB 800,000.

(3) Sold an equity holding of unlisted stock for RMB 900,000. The equity holding had been obtained by the contribution of a factory building by Company X which had cost RMB 300,000.

(4) Obtained a six-month bank loan of RMB 2,000,000 from 1 July 2010 with the pledge of a shop owned by the company. During the loan period, the bank did not charge any interest, but instead the bank had the right to use the shop rent free. The market interest rate for a similar loan is 6% per year. At the end of the loan period, Company X sold the shop for a price which gave it RMB 1,000,000 more than the amount needed to repay the bank loan.

Required:

Calculate the business tax (BT) payable by Company X as a result of each of the above transactions (1) to (4), giving brief explanations of their treatment. (6 marks)

(d) State the THREE conditions that must be met for a transportation fee paid by the seller to be excluded from the sale consideration for the purposes of value added tax (VAT). (3 marks)

4.

(a) Company K carried out the following transactions:

(1) Imported a vehicle costing RMB 300,000 and paid transportation costs of USD 10,000 for the journey from the overseas supplier to the port in China.

(2) Shipped a machine with a value of RMB 500,000 overseas for repair and paid for materials of USD 10,000 and a repairing fee of USD 30,000. The machine was shipped back to China in the same month.

(3) Subcontracted some domestic raw materials valued at RMB 200,000 to an overseas company. The related fee and transportation costs were USD 100,000 and USD 20,000 respectively.

(4) Imported raw materials costing RMB 30,000,000 and paid transportation costs of USD 50,000 for the journey from the overseas supplier to the port in China. After the arrival of the materials, Company K discovered that 20% of the materials had a quality problem. The supplier agreed to ship a further 20% replacement materials at no cost to Company K in the same month. Both parties agreed that the quality problem goods should be kept in China.

Required:

Calculate the customs tariff, consumption tax (CT) and value added tax (VAT) payable by Company K as a result of each of the above transactions.

Note: for the purposes of your calculations you should assume that:

(1) The customs tariff for all kinds of imported goods is 20%.

(2) The rate of consumption tax (CT) is 10%.

(3) The USD:RMB exchange rate is 1:6·6

(b) Briefly explain the procedures, including any time limits, for the declaration and payment of the customs

5.

Briefly explain the consequences of the following actions, including any fines or other penalty that may be imposed:

(a) Failure to keep or maintain proper accounting records/vouchers. (2 marks)

(b) Failure to file a return within the prescribed time limit. (2 marks)

(c) Failure to file a return and hence not paying or paying less tax than is duly payable. (1 mark)

(d) Failure to pay tax by concealment of property. (3 marks)

(e) Refusal to pay tax by violence or menace. (2 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第8题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. Apportionments should be made to the nearest month.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.3. All workings should be shown.

1.

(a) Company F is a manufacturing joint venture enterprise, which was established and started operations on 1 January 2010.

Company F’s statement of enterprise income tax (EIT) payable for the year 2010, as prepared by the company’s accountant is summarised below:

Notes:

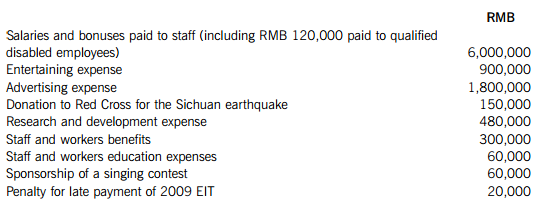

(1) The management and finance expenses included the following:

(2) The investment income included the following:

(3) The original cost of the fixed assets written off was RMB 600,000, the accumulated depreciation was RMB 420,000, and the accumulated tax allowances claimed were RMB 480,000.

Required:

(i) Briefly explain the treatment of each of the 13 items referred to in notes 1 to 3 for the purposes of enterprise income tax (EIT); (13 marks)

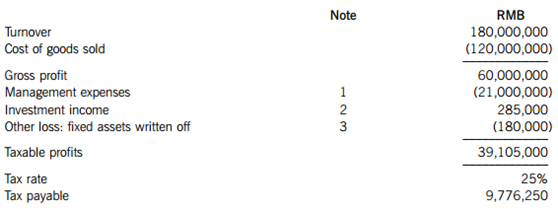

(ii) Calculate the correct amount of enterprise income tax (EIT) payable by Company F for the year 2010. Note: you should start your computation with the taxable profit calculated by the accountant of RMB 39,105,000 and indicating by the use of ‘0’ any items for which no adjustment is required. (7 marks)

(b) For the purposes of enterprise income tax (EIT) define the term ‘non-resident enterprise’ and explain the scope of such an enterprises EIT assessment. (4 marks)

(c) An overseas underground train building company, Company H is a non-resident enterprise for enterprise income tax (EIT) purposes. Company H signed a sales contract for RMB 100,000,000 for the supply of ten underground trains with a PRC company, Company K. The amount also included after-sales services (such as, installation, technical training, etc) but the service fee is not separately specified in the sales contract. The training will last two years and will be provided in China by Company H personnel from overseas.

Required:

Explain the enterprise income tax (EIT) and business tax (BT) implications in China for Company H and Company K if the tax bureau applies the lowest deemed income and profit rates that are specified in the relevant EIT laws and regulations. (7 marks)

(d) State the withholding tax rate for enterprise income tax (EIT) applicable to the following items paid to a non-resident enterprise:

(i) Dividends paid out of both pre-2008 and post-2008 retained earnings; (2 marks)

(ii) Interest; (1 mark)

(iii) Royalties on the licensing of trademarks, copyright, etc. (1 mark)

2.

(a) Mr Wu, a Chinese citizen, is a photographer for a newspaper. He had the following income for the month of September 2010:

(1) Monthly employment income of RMB 15,000 and a bonus for the year 2009 of RMB 20,000.

(2) Income of USD 5,000 (gross) from which tax of USD 750 was withheld from publishing an album overseas.

(3) Income of RMB 5,000 for publishing five of his photos as a postcard.

(4) A net gain of RMB 15,000 from trading in the A-shares market.

(5) Received RMB 200,000 from the sale of a property (50 square metres) that he had lived in for four years, which he had acquired for RMB 160,000.

(6) Gross interest income of RMB 6,000 from a bank deposit.

(7) Received RMB 11,000 as insurance compensation.

(8) Received RMB 50,000 as net proceeds from the sale of an antique, which he had originally acquired in 2004 for RMB 20,000.

(9) Income of Euro 300 for giving a lecture at a university during his visit to France. Individual income tax equivalent to RMB 400 was paid in France on this income.

Required:

Calculate the individual income tax (IIT) payable by Mr Wu on each of items (1) to (9) for the month of September 2010, clearly identifying any amounts which are tax exempt and briefly explaining any reliefs available.

Note: the following exchange rates are to be used:

1 1 USD = 7 RMB

2 1 Euro = 9·5 RMB (12 marks)

(b) Explain the treatment for individual income tax (IIT) of directorship fees. (3 marks)

(c) Explain the criteria used to determine whether an individual is a resident taxpayer in the PRC. (5 marks)

3.

(a) During the month of November 2010, Company Z, a food producer company, carried out the following transactions:

(1) Acquired five tons of wheat for RMB 50,000 (excluding value added tax (VAT)) from a farmer and paid RMB 1,200 (including VAT) to a manufacturing company, Company A, for flouring services.

(2) Purchased production tools for RMB 5,000 (including VAT) from a small-scale tools company.

(3) Produced eight tons of corn flour; sold seven tons of the corn flour for RMB 140,000 (excluding VAT), and distributed the remaining one ton to its own staff.

(4) Sold biscuits to several commercial entities by issuing general invoices and received RMB 80,000 (excluding VAT).

(5) Some wheat acquired in the previous month rotted due to improper keeping. The stock loss cost (excluding VAT) was RMB 6,000 including gross freight charges of RMB 800.

(6) Sold a used machine for RMB 7,000 (including VAT), which had been bought in June 2009 for RMB 9,000.

Required: Calculate the input and output value added tax (VAT) in respect of each of the above transactions and the VAT payable by Company Z for the month of November 2010. (12 marks)

(b) Company B had the following events during December 2010:

(i) stock costing RMB 12,000 (including transportation of RMB 6,000) was damaged in Warehouse A due to an earthquake; and

(ii) stock costing RMB 32,000 (including transportation of RMB 2,000) was damaged in Warehouse A due to mismanagement.

All figures are stated excluding any applicable value added tax (VAT)

Required:

Explain the treatment for value added tax (VAT) and enterprise income tax (EIT) of each of these stock losses, and calculate any deductible/non-deductible amounts. (5 marks)

(c) State the time limits (deadlines) for the reporting and payment of value added tax (VAT) for a taxpayer with:

(i) an assessable period of one month; and (1 mark)

(ii) an assessable period of less than one month. (2 marks)

4.

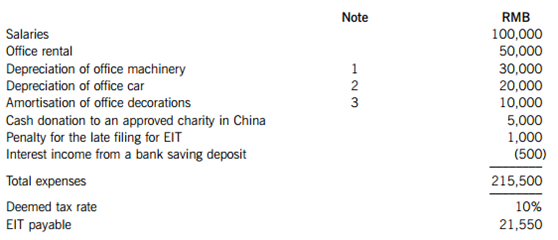

A representative office, Office X has agreed with the tax bureau to use the cost-plus basis for its enterprise income tax (EIT). The accountant of Office X prepared the following EIT calculation for the year 2010, the first year of Office X’s operation:

Notes:

1 The original cost of the office machinery was RMB 300,000 with a ten year economic life and no residual value.

2 The original cost of the office car was RMB 100,000 with a five year economic life and no residual value.

3 The original cost of the office decorations was RMB 30,000 with a three year economic life and no residual value.

Additional information:

The following payments, not included by the accountant when preparing the calculation above, were made in the year 2010:

RMB 100,000 for the purchase of goods from Office X’s head office, located overseas;

RMB 6,000 for samples of goods from Office X’s head office overseas; and

RMB 4,000 for the hire of a translator for the visit of head office staff to China.

Required:

Calculate the enterprise income tax (EIT) payable by Office X if the correct deemed profit rate is 15%, giving brief explanations of any items which were incorrectly treated by the accountant.

5.

(a) A property developer, Company R, had the following transactions in 2010:

(1) Sold a land use right for RMB 56 million, which had cost it RMB 42 million and with related legal costs of RMB 1 million.

(2) Sold a factory building for RMB 180 million, which had the following associated costs:

Required:

Calculate the land appreciation tax (LAT) payable on the above transactions by Company R. (6 marks)

(b) List the preferential enterprise income tax (EIT) treatment that applies to each of the following types of project:

(i) income derived from an agricultural/forestry/animal husbandry project;

(ii) income derived from a cultivation of flower/tea/sea farming project;

(iii) income derived from an approved infrastructure project; and

(iv) income derived from an approved environmental protection/energy/water conservation project. (4 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第9题

SUPPLEMENTARY INSTRUCTIONS

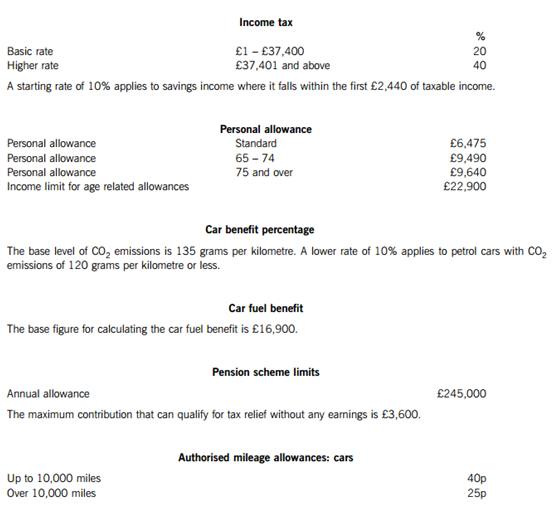

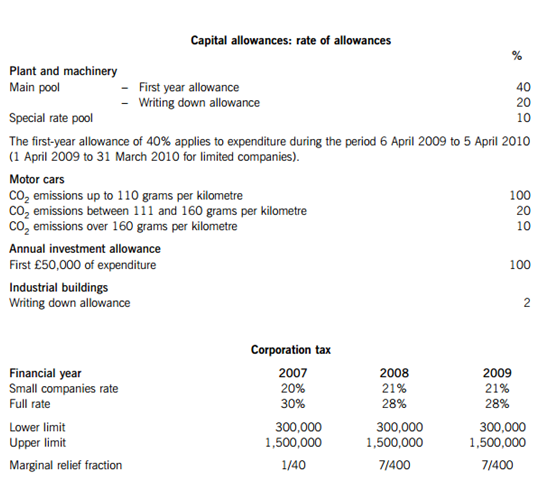

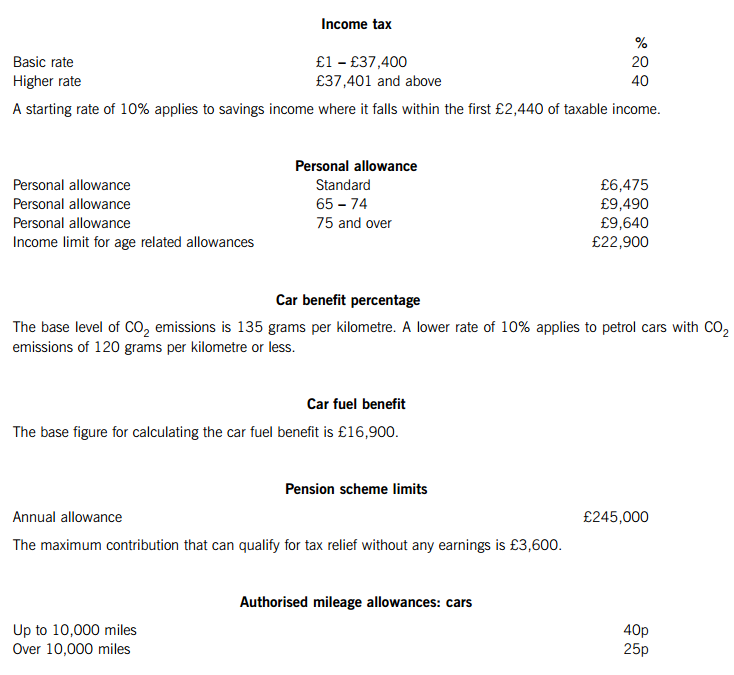

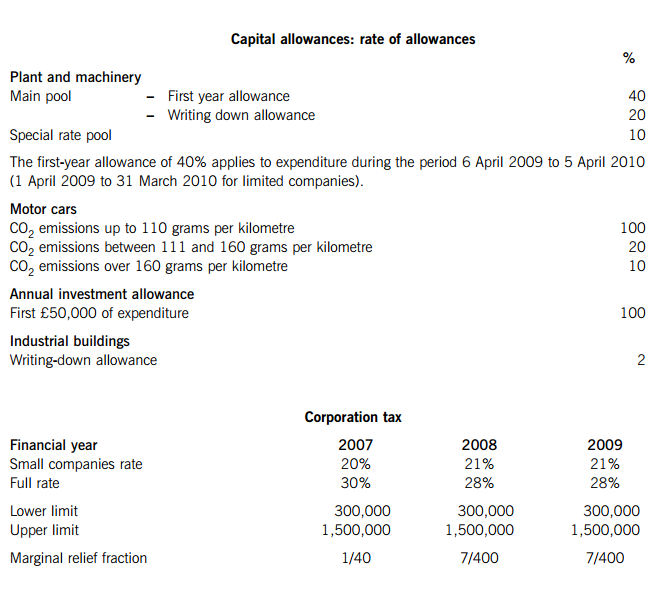

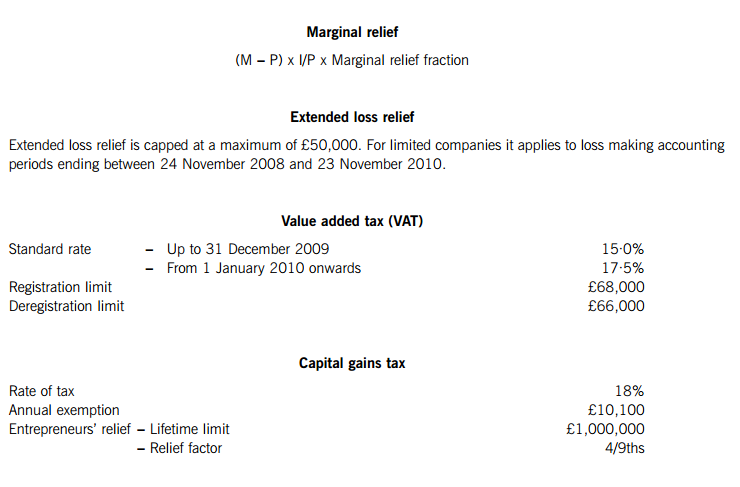

1. Calculations and workings need only be made to the nearest £.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

On 31 December 2009 Joe Jones resigned as an employee of Firstly plc, and on 1 January 2010 commenced employment with Secondly plc. Joe was employed by both companies as a financial analyst. The following information is available for the tax year 2009–10:

Employment with Firstly plc

(1) From 6 April 2009 to 31 December 2009 Joe was paid a salary of £11,400 per month. In addition to his salary, Joe was paid a bonus of £12,000 on 12 May 2009. He had become entitled to this bonus on 22 March 2009.

(2) Joe contributed 6% of his monthly gross salary of £11,400 into Firstly plc’s HM Revenue and Customs’ registered occupational pension scheme.

(3) On 1 May 2009 Firstly plc provided Joe with an interest free loan of £120,000 so that he could purchase a holiday cottage. Joe repaid £50,000 of the loan on 31 July 2009, and repaid the balance of the loan of £70,000 when he ceased employment with Firstly plc on 31 December 2009.

(4) During the period from 6 April 2009 to 31 December 2009 Joe’s three-year-old daughter was provided with a place at Firstly plc’s workplace nursery. The total cost to the company of providing this nursery place was £11,400 (190 days at £60 per day).

(5) During the period 6 April 2009 to 31 December 2009 Firstly plc paid gym membership fees of £1,050 for Joe.

(6) Firstly plc provided Joe with a home entertainment system for his personal use costing £4,400 on 6 April 2009. The company gave the home entertainment system to Joe for free, when he left the company on 31 December 2009, although its market value at that time was £3,860.

Employment with Secondly plc

(1) From 1 January 2010 to 5 April 2010 Joe was paid a salary of £15,200 per month.

(2) During the period 1 January 2010 to 5 April 2010 Joe contributed a total of £3,000 (gross) into a personal pension scheme.

(3) From 1 January 2010 to 5 April 2010 Secondly plc provided Joe with living accommodation. The property has an annual value of £10,400 and is rented by Secondly plc at a cost of £2,250 per month. On 1 January 2010 Secondly plc purchased furniture for the property at a cost of £16,320. The company pays for all of the running costs relating to the property, and for the period 1 January 2010 to 5 April 2010 these amounted to £1,900.

(4) During the period 1 January 2010 to 5 April 2010 Secondly plc provided Joe with 13 weeks of childcare vouchers costing £100 per week. Joe used the vouchers to provide childcare for his three-year-old daughter at a registered nursery near to his workplace.

(5) During the period 1 January 2010 to 5 April 2010 Joe used Secondly plc’s company gym which is only open to employees of the company. The cost to Secondly plc of providing this benefit to Joe was £340.

(6) During the period 1 January 2010 to 5 April 2010 Secondly plc provided Joe with a mobile telephone costing £560. The company paid for all of Joe’s business and private telephone calls.

Required:

(a) Calculate Joe Jones’ taxable income for the tax year 2009–10. (17 marks)

(b) (i) Briefly explain the basis of calculating Joe Jones’ PAYE tax code for the tax year 2009–10, and the purpose of this code; (2 marks)

(ii) For each of the PAYE forms P45, P60 and P11D, briefly describe the circumstances in which the form. will be completed, state who will provide it, the information to be included, and the dates by which they should have been provided to Joe Jones for the tax year 2009–10. (6 marks)

Note: your answer to both sub-parts (i) and (ii) should be confined to the details that are relevant to Joe Jones.

2.

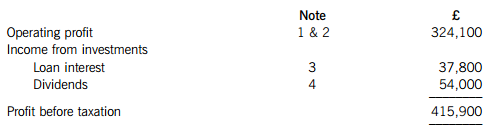

(a) Neung Ltd is a UK resident company that runs a business providing financial services. The company’s business is mainly based in the UK, but Neung Ltd also has two overseas branches. The company’s summarised profit and loss account for the year ended 31 March 2010 is as follows:

Note 1 – Operating profit

The operating profit does not include the results from either of Neung Ltd’s two overseas branches (see note (2) below).

Depreciation of £11,830 and amortisation of leasehold property of £7,000 have been deducted in arriving at the operating profit of £324,100.

Note 2 – Overseas branches

Neung Ltd’s first overseas branch made a trading profit of £41,000 for the year ended 31 March 2010. No overseas corporation tax was paid on this profit.

The second overseas branch made a trading loss of £15,700 for the year ended 31 March 2010.

Note 3 – Loan interest receivable

The loan was made for non-trading purposes on 1 July 2009. Loan interest of £25,200 was received on 31 December 2009, and interest of £12,600 was accrued at 31 March 2010.

Note 4 – Dividends received

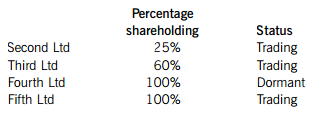

Neung Ltd holds shares in four UK resident companies as follows:

During the year ended 31 March 2010 Neung Ltd received a dividend of £37,800 from Second Ltd, and a dividend of £16,200 from Third Ltd. These figures were the actual cash amounts received.

Additional information

Leasehold property

On 1 April 2009 Neung Ltd acquired a leasehold office building, paying a premium of £140,000 for the grant of a 20-year lease. The office building was used for business purposes by Neung Ltd throughout the year ended 31 March 2010.

Plant and machinery

On 1 April 2009 the tax written down values of Neung Ltd’s plant and machinery were as follows:

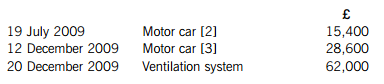

The company purchased the following assets during the year ended 31 March 2010:

Motor car [1] has a emission rate of 220 grams per kilometre. Motor car [2] purchased on 19 July 2009 has aemission rate of 242 grams per kilometre. Motor car [3] purchased on 12 December 2009 has aemission rate of 148 grams per kilometre.

emission rate of 220 grams per kilometre. Motor car [2] purchased on 19 July 2009 has aemission rate of 242 grams per kilometre. Motor car [3] purchased on 12 December 2009 has aemission rate of 148 grams per kilometre.

The ventilation system purchased on 20 December 2009 for £62,000 is integral to the freehold office building in which it was installed.

Required:

(i) State, giving reasons, which companies will be treated as being associated with Neung Ltd for corporation tax purposes; (2 marks)

(ii) Calculate Neung Ltd’s corporation tax liability for the year ended 31 March 2010; Note: you should assume that the whole of the annual investment allowance is available to Neung Ltd, and that the company wishes to maximise its capital allowances claim. (15 marks)

(iii) Advise Neung Ltd of the taxation disadvantages of converting its two overseas branches (see note (2)) into 100% overseas subsidiary companies. (3 marks)

(b) Note that in answering this part of the question you are not expected to take account of any of the information provided in part (a) above.

The following information is available in respect of Neung Ltd’s value added tax (VAT) for the quarter ended 31 March 2010:

(1) Invoices were issued for sales of £44,600 to VAT registered customers. Of this figure, £35,200 was in respect of exempt sales and the balance in respect of standard rated sales. The standard rated sales figure is exclusive of VAT.

(2) In addition to the above, on 1 March 2010 Neung Ltd issued a VAT invoice for £8,000 plus VAT of £1,400 to a VAT registered customer. This was in respect of a contract for standard rated financial services that will be completed on 15 April 2010. The customer paid for the contracted services in two instalments of £4,700 on 31 March 2010 and 30 April 2010 respectively.

(3) Invoices were issued for sales of £289,300 to non-VAT registered customers. Of this figure, £242,300 was in respect of exempt sales and the balance in respect of standard rated sales. The standard rated sales figure is inclusive of VAT.

(4) The managing director of Neung Ltd is provided with free fuel for private mileage driven in her company motor car. During the quarter ended 31 March 2010 this fuel cost Neung Ltd £260. The relevant quarterly scale charge is £390. Both these figures are inclusive of VAT.

For the quarters ended 30 September 2008 and 30 June 2009 Neung Ltd was one month late in submitting its VAT returns and in paying the related VAT liabilities. All of the company’s other VAT returns have been submitted on time.

Required:

(i) Calculate the amount of output VAT payable by Neung Ltd for the quarter ended 31 March 2010; (4 marks)

(ii) Advise Neung Ltd of the default surcharge implications if it is one month late in submitting its VAT return for the quarter ended 31 March 2010 and in paying the related VAT liability; (3 marks)

(iii) State the circumstances in which Neung Ltd is and is not required to issue a VAT invoice, and the period during which such an invoice should be issued. (3 marks)

3.

Lim Lam is the controlling shareholder and managing director of Mal-Mil Ltd, an unquoted trading company that provides support services to the oil industry.

Lim Lam

Lim disposed of the following assets during the tax year 2009–10:

(1) On 8 April 2009 Lim sold five acres of land to Mal-Mil Ltd for £260,000, which was the market value of the land on that date. The land had been inherited by Lim upon the death of her mother on 17 January 2003, when the land was valued at £182,000. Lim’s mother had originally purchased the land for £137,000.

(2) On 13 August 2009 Lim made a gift of 5,000 £1 ordinary shares in Oily plc, a quoted trading company, to her sister. On that date the shares were quoted on the Stock Exchange at £7·40–£7·56, with recorded bargains of £7·36, £7·38 and £7·60.

Lim had originally purchased 1,000 shares in Greasy plc on 8 July 2003 for £18,200. On 23 November 2003 Greasy plc was taken over by Oily plc. Lim received five £1 ordinary shares and two £1 preference shares in Oily plc for each £1 ordinary share held in Greasy plc. Immediately after the takeover each £1 ordinary share in Oily plc was quoted at £3·50 and each £1 preference share was quoted at £1·25.

Entrepreneurs’ relief and holdover relief are not available in respect of this disposal.

(3) On 22 March 2010 Lim sold 40,000 £1 ordinary shares in Mal-Mil Ltd for £280,000. She had originally purchased 125,000 shares in the company on 8 June 2002 for £142,000, and had purchased a further 60,000 shares on 23 May 2004 for £117,000. Mal-Mil Ltd has a total share capital of 250,000 £1 ordinary shares. Lim has made no previous disposals eligible for entrepreneurs’ relief.

Mal-Mil Ltd

On 20 December 2009 Mal-Mil Ltd sold two of the five acres of land that had been purchased from Lim on 8 April 2009. The sale proceeds were £162,000 and legal fees of £3,800 were incurred in connection with the disposal. The market value of the unsold three acres of land as at 20 December 2009 was £254,000. During April 2009 Mal-Mil Ltd had spent £31,200 levelling the five acres of land. The relevant retail price indexes (RPIs) are as follows:

Mal-Mil Ltd’s only other income for the year ended 31 December 2009 was a trading profit of £163,000.

Required:

(a) Explain why Lim Lam’s disposal of 40,000 £1 ordinary shares in Mal-Mil Ltd on 22 March 2010 qualifies for entrepreneurs’ relief. (2 marks)

(b) Calculate Lim Lam’s capital gains tax liability for the tax year 2009–10, and state by when this should be paid. (11 marks)

(c) Calculate Mal-Mil Ltd’s corporation tax liability for the year ended 31 December 2009, and state by when this should be paid. (7 marks)

4.

You should assume that today’s date is 20 March 2009.

Sammi Smith is a director of Smark Ltd. The company has given her the choice of being provided with a leased company motor car or alternatively being paid additional director’s remuneration and then privately leasing the same motor car herself.

Company motor car

The motor car will be provided throughout the tax year 2009–10, and will be leased by Smark Ltd at an annual cost of £26,540. The motor car will be petrol powered, will have a list price of £92,000, and will have an official CO2 emission rate of 320 grams per kilometre.

The lease payments will cover all the costs of running the motor car except for fuel. Smark Ltd will not provide Sammi with any fuel for private journeys.

Additional director’s remuneration

As an alternative to having a company motor car, Sammi will be paid additional gross director’s remuneration of £26,000 during the tax year 2009–10. She will then privately lease the motor car at an annual cost of £26,540.

Other information

The amount of business journeys that will be driven by Sammi will be immaterial and can therefore be ignored.

Sammi’s current annual director’s remuneration is in excess of £100,000. Smark Ltd prepares its accounts to 5 April, and pays corporation tax at the full rate of 28%. The lease of the motor car will commence on 6 April 2009.

Required:

(a) Advise Sammi Smith of the income tax and national insurance contribution implications for the tax year 2009–10 if she (1) is provided with the company motor car, and (2) receives additional director’s remuneration of £26,000. (5 marks)

(b) Advise Smark Ltd of the corporation tax and national insurance contribution implications for the year ended 5 April 2010 if the company (1) provides Sammi Smith with the company motor car, and (2) pays Sammi Smith additional director’s remuneration of £26,000. Note: you should ignore value added tax (VAT). (5 marks)

(c) Determine which of the two alternatives is the most beneficial from each of the respective points of view of Sammi Smith and Smark Ltd. (5 marks)

5.

Goff Green has been a self-employed manufacturer of golf equipment since 6 April 2000. For the year ended 5 April 2010 he made a trading loss of £85,000. Goff’s recent trading profits are as follows:

For each of the tax years from 2005–06 to 2009–10 Goff received gross building society interest of £3,800.

On 16 June 2009 Goff disposed of an investment and this resulted in a chargeable gain of £19,700. He disposed of another investment on 19 January 2010 and this resulted in a capital loss of £4,800.

Required:

(a) Calculate Goff Green’s taxable income and taxable gains for each of the tax years from 2005–06 to 2009–10 on the assumption that he relieves the maximum possible amount of the trading loss of £85,000 for the year ended 5 April 2010 as early as possible, but without unnecessarily wasting his personal allowances. Your answer should clearly show the amount of the trading loss that is unrelieved.

Note: you should assume that the tax allowances for the tax year 2009–10 apply throughout. (7 marks)

(b) Assuming that for the year ended 5 April 2011 Goff Green will make a trading profit of £40,000, explain why it would probably not be beneficial for him to make a loss relief claim against the chargeable gain of £19,700 arising on the disposal of the investment on 16 June 2009.

Note: you should assume that the tax rates and allowances for the tax year 2009–10 will continue to apply. (3 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

第10题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest £.

2. All apportionments should be made to the nearest month.

3. All workings should be shown.

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

ALL FIVE questions are compulsory and MUST be attempted

1.Auy Man and Bim Men have been in partnership since 6 April 2000 as management consultants. The following information is available for the tax year 2009–10:

Personal information