重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

(a) ‘Revenue recognition should always be approached as a high risk area of the audit.’

Required:

Discuss this statement. (6 marks)

(b) You are a manager in Beck & Co, responsible for the audit of Kobain Co, a new audit client of your firm, with a financial year ended 31 July 2012. Kobain Co’s draft financial statements recognise total assets of $55 million, and profit before tax of $15 million. The audit is nearing completion and you are rewiewing the audit files.

Kobain Co designs and creates high-value items of jewellery. Approximately half of the jewellery is sold in Kobain Co’s own retail outlets. The other half is sold by external vendors under a consignment stock arrangement, the terms of which specify that Kobain Co retains the ability to change the selling price of the jewellery, and that the vendor is required to return any unsold jewellery after a period of nine months. When the vendor sells an item of jewellery to a customer, legal title passes from Kobain Co to the customer.

On delivery of the jewellery to the external vendors, Kobain Co recognises revenue and derecognises inventory. At 31 July 2012, jewellery at cost price of $3 million is held at external vendors. Revenue of $4 million has been recognised in respect of this jewellery.

Required:

Comment on the matters that should be considered, and explain the audit evidence you should expect to find in your file review in respect of the consignment stock arrangement. (6 marks)

(c) Your firm also performs the audit of Jarvis Co, a company which installs windows. Jarvis Co uses sales representatives to make direct sales to customers. The sales representatives earn a small salary, and also earn a sales commission of 20% of the sales they generate.

Jarvis Co’s sales manager has discovered that one of the sales representatives has been operating a fraud, in which he was submitting false claims for sales commission based on non-existent sales. The sales representative started to work at Jarvis Co in January 2012. The forensic investigation department of your firm has been engaged to quantify the amount of the fraud.

Required:

Recommend the procedures that should be used in the forensic investigation to quantify the amount of the fraud. (4 marks)

更多“(a) ‘Revenue recognition should always be approached as a high risk area of the audit.’Req”相关的问题

更多“(a) ‘Revenue recognition should always be approached as a high risk area of the audit.’Req”相关的问题

第1题

Section B – TWO questions ONLY to be attempted

(a) You are an audit manager in Weller & Co, an audit firm which operates as part of an international network of firms. This morning you received a note from a partner regarding a potential new audit client:

‘I have been approached by the audit committee of the Plant Group, which operates in the mobile telecommunications sector. Our firm has been invited to tender for the audit of the individual and group financial statements for the year ending 31 March 2013, and I would like your help in preparing the tender document. This would be a major new client for our firm’s telecoms audit department.

The Plant Group comprises a parent company and six subsidiaries, one of which is located overseas. The audit committee is looking for a cost effective audit, and hopes that the strength of the Plant Group’s governance and internal control mean that the audit can be conducted quickly, with a proposed deadline of 31 May 2013. The Plant Group has expanded rapidly in the last few years and significant finance was raised in July 2012 through a stock exchange listing.’

Required:

Identify and explain the specific matters to be included in the tender document for the audit of the Plant Group. (8 marks)

(b) Weller & Co is facing competition from other audit firms, and the partners have been considering how the firm’s revenue could be increased. Two suggestions have been made: 1. Audit partners and managers can be encouraged to sell non-audit services to audit clients by including in their remuneration package a bonus for successful sales. 2. All audit managers should suggest to their audit clients that as well as providing the external audit service, Weller & Co can provide the internal audit service as part of an ‘extended audit’ service. Required: Comment on the ethical and professional issues raised by the suggestions to increase the firm’s revenue. (8 marks)

第2题

e Group), which is listed. The Group’s main activity is steel manufacturing and it comprises a parent company and five subsidiaries. Sambora & Co currently audits all components of the Group.

You are working on the audit of the Group’s financial statements for the year ended 30 June 2012. This morning the audit engagement partner left a note for you:

‘Hello

The audit senior has provided you with the draft consolidated financial statements and accompanying notes which summarise the key audit findings and some background information.

At the planning stage, materiality was initially determined to be $900,000, and was calculated based on the assumption that the Jovi Group is a high risk client due to its listed status. During the audit, a number of issues arose which meant that we needed to revise the materiality level for the financial statements as a whole. The revised level of materiality is now determined to be $700,000. One of the audit juniors was unsure as to why the materiality level had been revised. There are two matters you need to deal with:

(i) Explain why auditors may need to reassess materiality as the audit progresses. (4 marks)

(ii) Assess the implications of the key audit findings for the completion of the audit. Your assessment must consider whether the key audit findings indicate a risk of material misstatement. Where the key audit findings refer to audit evidence, you must also consider the adequacy of the audit evidence obtained, but you do not need to recommend further specific procedures. (18 marks)

Thank you’

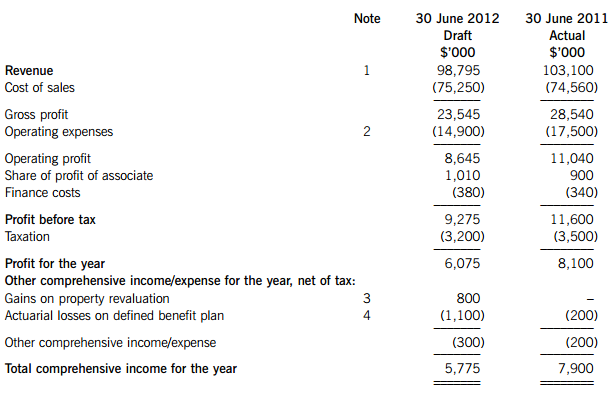

The Group’s draft consolidated financial statements, with notes referenced to key audit findings, are shown below:

Draft consolidated statement of comprehensive income

Notes: Key audit findings – statement of comprehensive income

1. Revenue has been stable for all components of the Group with the exception of one subsidiary, Copeland Co, which has recognised a 25% decrease in revenue.

2. Operating expenses for the year to June 2012 is shown net of a profit on a property disposal of $2 million. Our evidence includes agreeing the cash receipts to bank statement and sale documentation, and we have confirmed that the property has been removed from the non-current asset register. The audit junior noted when reviewing the sale document, that there is an option to repurchase the property in five years time, but did not discuss the matter with management.

3. The property revaluation relates to the Group’s head office. The audit team have not obtained evidence on the revaluation, as the gain was immaterial based on the initial calculation of materiality.

4. The actuarial loss is attributed to an unexpected stock market crash. The Group’s pension plan is managed by Axle Co – a firm of independent fund managers who maintain the necessary accounting records relating to the plan. Axle Co has supplied written representation as to the value of the defined benefit plan’s assets and liabilities at 30 June 2012. No other audit work has been performed other than to agree the figure from the financial statements to supporting documentation supplied by Axle Co.

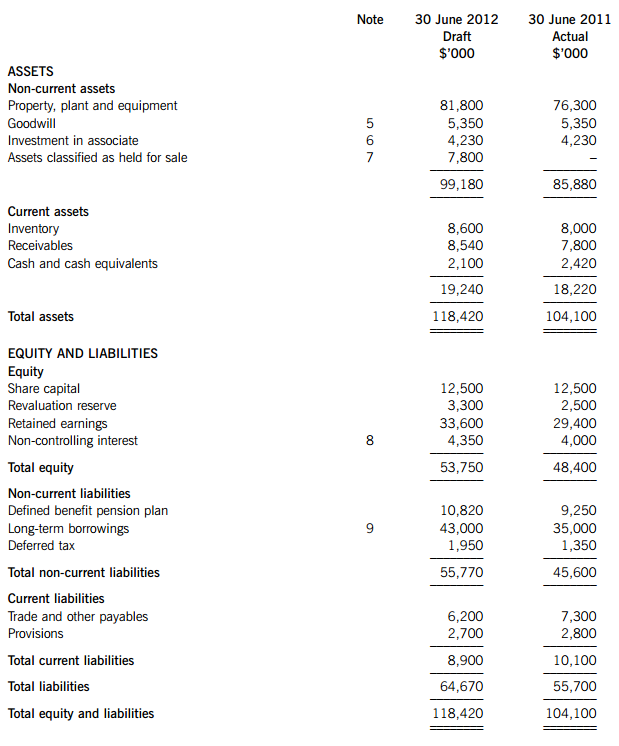

Draft consolidated statement of financial position

Notes: Key audit findings – statement of financial position

5. The goodwill relates to each of the subsidiaries in the Group. Management has confirmed in writing that goodwill is stated correctly, and our other audit procedure was to arithmetically check the impairment review conducted by management.

6. The associate is a 30% holding in James Co, purchased to provide investment income. The audit team have not obtained evidence regarding the associate as there is no movement in the amount recognised in the statement of financial position.

7. The assets held for sale relate to a trading division of one of the subsidiaries, which represents one third of that subsidiary’s net assets. The sale of the division was announced in May 2012, and is expected to be complete by 31 December 2012. Audit evidence obtained includes a review of the sales agreement and confirmation from the buyer, obtained in July 2012, that the sale will take place.

8. Two of the Group’s subsidiaries are partly owned by shareholders external to the Group.

9. A loan of $8 million was taken out in October 2011, carrying an interest rate of 2%, payable annually in arrears. The terms of the loan have been confirmed to documentation provided by the bank.

Required:

Respond to the note from the audit engagement partner. (22 marks)

Note: The split of the mark allocation is shown within the partner’s note.

(b) The audit engagement partner now sends a further note regarding the Jovi Group:

‘The Group finance director has just informed me that last week the Group purchased 100% of the share capital of May Co, a company located overseas in Farland. The Group audit committee has suggested that due to the distant location of May Co, a joint audit could be performed, starting with the next financial statements for the year ending 30 June 2013. May Co’s current auditors are a small local firm called Moore & Co who operate only in Farland.’

Required:

Discuss the advantages and disadvantages of a joint audit being performed on the financial statements of May Co. (6 marks)

第3题

Section A – BOTH questions are compulsory and MUST be attempted

(a) You are a manager in Foo & Co, responsible for the audit of Grohl Co, a company which produces circuit boards which are sold to manufacturers of electrical equipment such as computers and mobile phones. It is the first time that you have managed this audit client, taking over from the previous audit manager, Bob Halen, last month. The audit planning for the year ended 30 November 2012 is about to commence, and you have just received an email from Mia Vai, the audit engagement partner.

Comments made by Mo Satriani in your meeting

Business overview

Grohl Co’s principal business activity remains the production of circuit boards. One of the key materials used in production is copper wiring, all of which is imported. As a cost cutting measure, in April 2012 a contract with a new overseas supplier was signed, and all of the company’s copper wiring is now supplied under this contract. Purchases are denominated in a foreign currency, but the company does not use forward exchange contracts in relation to its imports of copper wiring.

Grohl Co has two production facilities, one of which produces goods for the export market, and the other produces goods for the domestic market. About half of its goods are exported, but the export market is suffering due to competition from cheaper producers overseas. Most domestic sales are made under contract with approximately 20 customers.

Recent developments

In early November 2012, production was halted for a week at the production facility which supplies the domestic market. A number of customers had returned goods, claiming faults in the circuit boards supplied. On inspection, it was found that the copper used in the circuit boards was corroded and therefore unsuitable for use. The corrosion is difficult to spot as it cannot be identified by eye, and relies on electrical testing. All customers were contacted immediately and, where necessary, products recalled and replaced. The corroded copper remaining in inventory has been identified and separated from the rest of the copper.

Work has recently started on a new production line which will ensure that Grohl Co meets new regulatory requirements prohibiting the use of certain chemicals, which come into force in March 2013. In July 2012, a loan of $30 million with an interest rate of 4% was negotiated with Grohl Co’s bank, the main purpose of the loan being to fund the capital expenditure necessary for the new production line. $2·5 million of the loan represents an overdraft which was converted into long-term finance.

Other matters

Several of Grohl Co’s executive directors and the financial controller left in October 2012, to set up a company specialising in the recycling of old electronic equipment. This new company is not considered to be in competition with Grohl Co’s operations. The directors left on good terms, and replacements for the directors have been recruited. One of Foo & Co’s audit managers, Bob Halen, is being interviewed for the role of financial controller at Grohl Co. Bob is a good candidate for the position, as he developed good knowledge of Grohl Co’s business when he was managing the audit.

At Grohl Co’s most recent board meeting, the audit fee was discussed. The board members expressed concern over the size of the audit fee, given the company’s loss for the year. The board members would like to know whether the audit can be performed on a contingent fee basis.

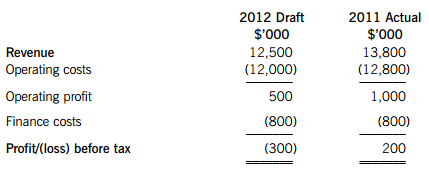

Financial Information provided by Mo Satriani

Extract from draft statement of comprehensive income for the year ended 30 November 2012

The draft statement of financial position has not yet been prepared, but Mo states that the total assets of Grohl Co at 30 November 2012 are $180 million, and cash at bank is $130,000. Based on draft figures, the company’s current ratio is 1·1, and the quick ratio is 0·8.

Required:

Respond to the email from the audit partner. (28 marks)

Note: The split of the mark allocation is shown within the partner’s email.

Professional marks will be awarded for the presentation, structure, logical flow and clarity of your answer. (4 marks)

(b) You have just received a phone call from Mo Satriani, Grohl Co’s finance director, in which he made the following comments:

‘There is something I forgot to mention in our meeting. Our business insurance covers us for specific occasions when business is interrupted. I put in a claim on 28 November 2012 for $5 million which I have estimated to cover the period when our production was halted due to the problem with the corroded copper. This is not yet recognised in the financial statements, but I want to make an adjustment to recognise the $5 million as a receivable as at 30 November.’

Required:

Comment on the matters that should be considered, and recommend the audit procedures to be performed, in respect of the insurance claim. (8 marks)

第4题

audit of Snipe Co. You are currently reviewing the audit working papers and draft audit report on the financial statements of Snipe Co for the year ended 31 January 2012. The draft financial statements recognise revenue of $8·5 million, profit before tax of $1 million, and total assets of $175 million.

(a) During the year Snipe Co’s factory was extended by the self-construction of a new processing area, at a total cost of $5 million. Included in the costs capitalised are borrowing costs of $100,000, incurred during the six-month period of construction. A loan of $4 million carrying an interest rate of 5% was taken out in respect of the construction on 1 March 2011, when construction started. The new processing area was ready for use on 1 September 2011, and began to be used on 1 December 2011. Its estimated useful life is 15 years.

Required:

In respect of your file review of non-current assets:

Comment on the matters that should be considered, and the evidence you would expect to find regarding the new processing area. (8 marks)

(b) Snipe Co has in place a defined benefit pension plan for its employees. An actuarial valuation on 31 January 2012 indicated that the plan is in deficit by $10·5 million. The deficit is not recognised in the statement of financial position. An extract from the draft audit report is given below:

Auditor’s opinion

In our opinion, because of the significance of the matter discussed below, the financial statements do not give a true and fair view of the financial position of Snipe Co as at 31 January 2012, and of its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards.

Explanation of adverse opinion in relation to pension

The financial statements do not include the company’s pension plan. This deliberate omission contravenes accepted accounting practice and means that the accounts are not properly prepared.

Required:

Critically appraise the extract from the proposed audit report of Snipe Co for the year ended 31 January 2012.

Note: you are NOT required to re-draft the extract of the audit report. (7 marks)

第5题

situations which have arisen in respect of audit clients, which were recently discussed at the monthly audit managers’ meeting:

Grouse Co is a significant audit client which develops software packages. Its managing director, Max Partridge, has contacted one of your firm’s partners regarding a potential business opportunity. The proposal is that Grouse Co and Raven & Co could jointly develop accounting and tax calculation software, and that revenue from sales of the software would be equally split between the two firms. Max thinks that Raven & Co’s audit clients would be a good customer base for the product.

Plover Co is a private hospital which provides elective medical services, such as laser eye surgery to improve eyesight. The audit of its financial statements for the year ended 31 March 2012 is currently taking place. The audit senior overheard one of the surgeons who performs laser surgery saying to his colleague that he is hoping to finish his medical qualification soon, and that he was glad that Plover Co did not check his references before employing him. While completing the subsequent events audit procedures, the audit senior found a letter from a patient’s solicitor claiming compensation from Plover Co in relation to alleged medical negligence resulting in injury to the patient.

Required:

Identify and discuss the ethical, commercial and other professional issues raised, and recommend any actions that should be taken in respect of:

(a) Grouse Co; and (8 marks)

(b) Plover Co. (7 marks)

第6题

Section B – TWO questions ONLY to be attempted

(a) You are a manager in Lark & Co, responsible for the audit of Heron Co, an owner-managed business which operates a chain of bars and restaurants. This is your firm’s first year auditing the client and the audit for the year ended 31 March 2012 is underway. The audit senior sends a note for your attention:

‘When I was auditing revenue I noticed something strange. Heron Co’s revenue, which is almost entirely cash-based, is recognised at $5·5 million in the draft financial statements. However, the accounting system shows that till receipts for cash paid by customers amount to only $3·5 million. This seemed odd, so I questioned Ava Gull, the financial controller about this. She said that Jack Heron, the company’s owner, deals with cash receipts and posts through journals dealing with cash and revenue. Ava asked Jack the reason for these journals but he refused to give an explanation.

‘While auditing cash, I noticed a payment of $2 million made by electronic transfer from the company’s bank account to an overseas financial institution. The bank statement showed that the transfer was authorised by Jack Heron, but no other documentation regarding the transfer was available.

‘Alarmed by the size of this transaction, and the lack of evidence to support it, I questioned Jack Heron, asking him about the source of cash receipts and the reason for electronic transfer. He would not give any answers and became quite aggressive.’

Required:

(i) Discuss the implications of the circumstances described in the audit senior’s note; and (6 marks)

(ii) Explain the nature of any reporting that should take place by the audit senior. (3 marks)

(b) You are also responsible for the audit of Coot Co, and you are currently reviewing the working papers of the audit for the year ended 28 February 2012. In the working papers dealing with payroll, the audit junior has commented as follows:

‘Several new employees have been added to the company’s payroll during the year, with combined payments of $125,000 being made to them. There does not appear to be any authorisation for these additions. When I questioned the payroll supervisor who made the amendments, she said that no authorisation was needed because the new employees are only working for the company on a temporary basis. However, when discussing staffing levels with management, it was stated that no new employees have been taken on this year. Other than the tests of controls planned, no other audit work has been performed.’

Required:

In relation to the audit of Coot Co’s payroll:

Explain the meaning of the term ‘professional skepticism’, and recommend any further actions that should be taken by the auditor. (6 marks)

第7题

ates commercial real estate properties typically comprising several floors of retail units and leisure facilities such as cinemas and health clubs, which are rented out to provide rental income.

Your firm has just been approached to provide an additional engagement for Hawk Co, to review and provide a report on the company’s business plan, including forecast financial statements for the 12-month period to 31 May 2013. Hawk Co is in the process of negotiating a new bank loan of $30 million and the report on the business plan is at the request of the bank. It is anticipated that the loan would be advanced in August 2012 and would carry an interest rate of 4%. The report would be provided by your firm’s business advisory department and a second partner review will be conducted which will reduce any threat to objectivity to an acceptable level.

Extracts from the forecast financial statements included in the business plan are given below:

Statement of comprehensive income (extract)

Notes:

1. Beak Retail is a retail park which is underperforming. Its sale is currently being negotiated, and is expected to take place in September 2012.

2. Hawk Co is planning to invest the cash raised from the bank loan in a new retail and leisure park which is being developed jointly with another company, Kestrel Co.

Required:

In respect of the engagement to provide a report on Hawk Co’s business plan:

(i) Identify and explain the matters that should be considered in agreeing the terms of the engagement; and Note: You are NOT required to consider ethical threats to objectivity. (6 marks)

(ii) Recommend the procedures that should be performed in order to examine and report on the forecast financial statements of Hawk Co for the year to 31 May 2013. (13 marks)

(b) You are also responsible for the audit of Osprey Co, which has a financial year ended 31 May 2012. The audit engagement partner, Bill Kingfisher, sent you the following email this morning:

Required:

Respond to the partner’s email. (10 marks)

Note: the split of the mark allocation is shown within the partner’s email.

Professional marks will be awarded in part (b) for the presentation and clarity of your answer. (4 marks)

第8题

Section A – BOTH questions are compulsory and MUST be attempted

You are a manager in Magpie & Co, responsible for the audit of the CS Group. An extract from the permanent audit file describing the CS Group’s history and operations is shown below:

Permanent file (extract)

Crow Co was incorporated 100 years ago. It was founded by Joseph Crow, who established a small pottery making tableware such as dishes, plates and cups. The products quickly grew popular, with one range of products becoming highly sought after when it was used at a royal wedding. The company’s products have retained their popularity over the decades, and the Crow brand enjoys a strong identity and good market share.

Ten years ago, Crow Co made its first acquisition by purchasing 100% of the share capital of Starling Co. Both companies benefited from the newly formed CS Group, as Starling Co itself had a strong brand name in the pottery market. The CS Group has a history of steady profitability and stable management.

Crow Co and Starling Co have a financial year ending 31 July 2012, and your firm has audited both companies for several years.

(a) You have received an email from Jo Daw, the audit engagement partner:

Attachment: Notes from meeting with Steve Eagle, finance director of the CS Group

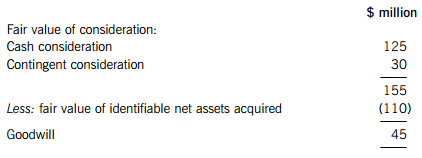

Acquisition of Canary Co

The most significant event for the CS Group this year was the acquisition of Canary Co, which took place on 1 February 2012. Crow Co purchased all of Canary Co’s equity shares for cash consideration of $125 million, and further contingent consideration of $30 million will be paid on the third anniversary of the acquisition, if the Group’s revenue grows by at least 8% per annum. Crow Co engaged an external provider to perform. due diligence on Canary Co, whose report indicated that the fair value of Canary Co’s net assets was estimated to be $110 million at the date of acquisition. Goodwill arising on the acquisition has been calculated as follows:

To help finance the acquisition, Crow Co issued loan stock at par on 31 January 2012, raising cash of $100 million. The loan has a five-year term, and will be repaid at a premium of $20 million. 5% interest is payable annually in arrears. It is Group accounting policy to recognise financial liabilities at amortised cost.

Canary Co manufactures pottery figurines and ornaments. The company is considered a good strategic fit to the Group, as its products are luxury items like those of Crow Co and Starling Co, and its acquisition will enable the Group to diversify into a different market. Approximately 30% of its sales are made online, and it is hoped that online sales can soon be introduced for the rest of the Group’s products. Canary Co has only ever operated as a single company, so this is the first year that it is part of a group of companies.

Financial performance and position

The Group has performed well this year, with forecast consolidated revenue for the year to 31 July 2012 of $135 million (2011 – $125 million), and profit before tax of $8·5 million (2011 – $8·4 million). A breakdown of the Group’s forecast revenue and profit is shown below:

Note: Canary Co’s results have been included from 1 February 2012 (date of acquisition), and forecast up to 31 July 2012, the CS Group’s financial year end.

The forecast consolidated statement of financial position at 31 July 2012 recognises total assets of $550 million.

Other matters

Starling Co received a grant of $35 million on 1 March 2012 in relation to redevelopment of its main manufacturing site. The government is providing grants to companies for capital expenditure on environmentally friendly assets. Starling Co has spent $25 million of the amount received on solar panels which generate electricity, and intends to spend the remaining $10 million on upgrading its production and packaging lines.

On 1 January 2012, a new IT system was introduced to Crow Co and Starling Co, with the aim of improving financial reporting controls and to standardise processes across the two companies. Unfortunately, Starling Co’s finance director left the company last week.

Required:

Respond to the email from the partner. (31 marks)

Note: the split of the mark allocation is shown within the email.

(b) Magpie & Co’s ethics partner, Robin Finch, leaves a note on your desk:

‘I have just had a conversation with Steve Eagle concerning the CS Group. He would like the audit engagement partner to attend the CS Group’s board meetings on a monthly basis so that our firm can be made aware of any issues relating to the audit as soon as possible. Also, Steve asked if one of our audit managers could be seconded to Starling Co in temporary replacement of its finance director who recently left, and asked for our help in recruiting a permanent replacement. Please provide me with a response to Steve which evaluates the ethical implications of his requests.’

Required:

Respond to the note from the partner. (6 marks)

第9题

evelops aircraft engines. The audit for the year ended 31 July 2011 is nearing completion and the audit senior has left the following file note for your attention:

‘I have just returned from a meeting with the management of Yew Co, and there is a matter I want to bring to your attention. Yew Co’s statement of financial position recognises an intangible asset of $12·5 million in respect of capitalised research and development costs relating to new aircraft engine designs. However, market research conducted by Yew Co in relation to these new designs indicated that there would be little demand in the near future for such designs. Management has provided written representation that they agree with the results of the market research.

Currently, Yew Co has a cash balance of only $125,000 and members of the management team have expressed concerns that the company is finding it difficult to raise additional finance.

The new aircraft designs have been discussed in the chairman’s statement which is to be published with the financial statements. The discussion states that ‘developments of new engine designs are underway, and we believe that these new designs will become a significant source of income for Yew Co in the next 12 months.’

Yew Co’s draft financial statements include profit before tax of $23 million, and total assets of $210 million.

Yew Co is due to publish its annual report next week, so we need to consider the impact of this matter urgently.’

Required:

Discuss the implications of the audit senior’s file note on the completion of the audit and on the auditor’s report, recommending any further actions that should be taken by the auditor. (12 marks)

(b) You are responsible for answering technical queries from other managers and partners of your firm. An audit partner left the following note on your desk this morning:

(i) ‘I am about to draft the audit report for my client, Sycamore Co. I am going on holiday tomorrow and want to have the audit report signed and dated before I leave. The only thing outstanding is the written representation from management – I have verbally confirmed the contents with the finance director who agreed to send the representations to the audit manager within the next few days. I presume this is acceptable?’ (3 marks)

(ii) ‘We are auditing Sycamore Co for the first time. The prior period financial statements were audited by another firm. We are aware that the auditor’s report on the prior period was qualified due to a material misstatement of trade receivables. We have obtained sufficient appropriate evidence that the matter giving rise to the misstatement has been resolved and I am happy to issue an unmodified opinion. But should I refer to the prior year modification in this year’s auditor’s report?’ (3 marks)

Required:

Respond to the audit partner’s comments.

Note: the split of the mark allocation is shown within the question. (18 marks)

第10题

rge company which provides information technology services to business customers. The finance director of Chestnut Co, Jack Privet, contacted you this morning, saying:

‘I was alerted yesterday to a fraud being conducted by members of our sales team. It appears that several sales representatives have been claiming reimbursement for fictitious travel and client entertaining expenses and inflating actual expenses incurred. Specifically, it has been alleged that the sales representatives have claimed on expenses for items such as gifts for clients and office supplies which were never actually purchased, claimed for business-class airline tickets but in reality had purchased economy tickets, claimed for non-existent business mileage and used the company credit card to purchase items for personal use.

I am very worried about the scale of this fraud, as travel and client entertainment is one of our biggest expenses. All of the alleged fraudsters have been suspended pending an investigation, which I would like your firm to conduct. We will prosecute these employees to attempt to recoup our losses if evidence shows that a fraud has indeed occurred, so your firm would need to provide an expert witness in the event of a court case. Can we meet tomorrow to discuss this potential assignment?’

Chestnut Co has a small internal audit department and in previous years the evidence obtained by Cedar & Co as part of the external audit has indicated that the control environment of the company is generally good. The audit opinion on the financial statements for the year ended 31 March 2011 was unmodified.

Required:

(a) Assess the ethical and professional issues raised by the request for your firm to investigate the alleged fraudulent activity. (6 marks)

(b) Explain the matters that should be discussed in the meeting with Jack Privet in respect of planning the investigation into the alleged fraudulent activity. (6 marks)

(c) Evaluate the arguments for and against the prohibition of auditors providing non-audit services to audit clients. (6 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!