重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

假设你选择了3项资产组合(A.B.C),其预期收益分别是0.08,0.09,0.10,他们的标准差分别是0.04,0.06,0.08,这项资产组合包括40%的A资产,40%的B资产,20%的C资产,A与B的相关系数为0.6,A与C的相关系数为0.4,B与C的相关系数为0.3。 a.该资产组合的预期收益及风险为多少?与仅持有资产C比较。 b.如果将A资产换为一种无风险、收益率为7%的资产,对资产组合的预期收益和风险的影响怎样? c.如果将A资产换为一种预期收益率为11%。标准差为0.1,且与资产B和C无相关性的证券,对资产组合的预期收益及风险有何影响?在资产组合中,你倾向于持有该证券还是资产A? Suppose you select a portfolio of three assets(A,B,C)in which the expected returns are 0.08,0.09,and 0.10,respectively;their standard deviations are 0.04,0.06,and 0.08;the portfolio consists of 40 percent of asset A,40 percent of asset B,and 20 percent of asset C;and the correlation coefficient between A and B is 0.6,between A and C is 0.4,and between B and C is 0.3. a.What is the expected retum and risk of the portfolio?How does this compare with a portfolio that consists only of asset C? b.Suppose that you replace asset A with a risk-free asset having a 7 percent yield.How doesthis affect expected retum and risk? C.Suppose,instead,that you replace asset A with a security having an expected return of 11percent,a standard deviation of 0.10,and no correlation with assets B and C.How does this affect the portfolio’s risk and expected retum?Would you rather have this or asset A in our portfolio?

更多“假设你选择了3项资产组合(A.B.C),其预期收益分别是0.08,0.09,0.10,他们的标准差分别是0.04,0.06,”相关的问题

更多“假设你选择了3项资产组合(A.B.C),其预期收益分别是0.08,0.09,0.10,他们的标准差分别是0.04,0.06,”相关的问题

第1题

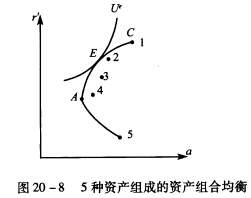

一位厌恶风险的投资者。其资产组合在如图20—8所示中的E点达到均衡。这时突然他能够得到一项无风险的资产。请用图形表示这将如何影响资产组合的均衡,试讨论。 A risk—averse investor is in equilibrium at a point such as E in Figure 20—8.Suddenly.a risk-free asset becomes available.Show graphically how this affects portfolio equilibrium.Discuss.

请帮忙给出正确答案和分析,谢谢!

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!