重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

A. Correct the asset information and provide updates to prospective clients.

B. Report the discrepancy to CFA Institute’s Professional Conduct Program.

C. Provide a disclaimer within marketing material indicating prices are as of a specific date.

更多“Carlos Cruz, CFA, is one of two founders of an equity hedge fund. Cruz manages the fun”相关的问题

更多“Carlos Cruz, CFA, is one of two founders of an equity hedge fund. Cruz manages the fun”相关的问题

第1题

ranked from lowest to highest as follows:

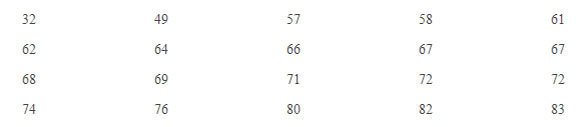

In a frequency distribution from 30% to 90% that is divided into six equal-sized intervals, the absolute frequency of the sixth interval is:

A) 2.

B) 4.

C) 1.

D) 3.

第2题

of the economy in thefollowing way:

The standard deviation of XYZ's expected return on equity is closest to:

A) 3.5%.

B) 12.3%.

C) 1.3%.

D) 1.5%.

第3题

. Romel wants to calculate the return on the portfolio. Over the last five years, the fund’s annual percentage returns were: 25, 15, 12, -8, and –14. Determine if the geometric return of the fund will be less than or greater than the arithmetic return and calculate the fund’s geometric return:

Geometric Return Geometric compared to Arithmetic

A) 4.96% greater than

B) 12.86% greater than

C) 12.86% less than

D) 4.96% less than

第4题

ample with 64 observations, the researcher calculates a sample mean of -2.5 and a sample standard deviation of 8.0. At which levels of significance should the researcher reject the hypothesis?

1% significance 5% significance 10% significance

A) Reject Fail to reject Fail to reject

B) Fail to reject Fail to reject Reject

C) Reject Reject Reject

D) Fail to reject Reject Reject

第5题

inheritance. Tekei needs funds for the down payment on a co-op in Manhattan and has found a bank that will give her the present value of her inheritance amount, assuming an 8.0% stated annual interest rate with continuous compounding. Will the proceeds from the bank be sufficient to cover her down payment of $65,000?

A) Yes, Tekei will receive $68,058.

B) No, Tekei will only receive $49,182.

C) No, Tekei will only receive $61,878.

D) Yes, Tekei will receive $67,028.

第6题

n of 6.45, its price value of a basis point (PVBP) isclosest to:

A. 0.0524

B. 0.0628

C. 0.0779

第7题

rest rate risk of a bond portfolio relative to the duration/convexity approach?

A. less time consuming.

B. easier to model.

C. more accurate.

第8题

erest rate risk of a bond portfolio, compared to the duration/convexity approach?

A. It ignores the impact of embedded options.

B. It is relatively time consuming.

C. It cannot be used for stress testing.

第9题

putable bonds will fall more quickly than comparable option-free bonds (beyond a critical point) due to the decline in value of the embedded put option. Meimei Han adds that as yields fall, the price of putable bonds will climb more quickly than comparable option-free bonds (beyond a critical point) due to the increase in value of the embedded put option. Are their statements about putable bonds correct?

A. Neither statement is correct.

B. Both statements are correct.

C. Only one of the statements is correct.

第10题

interest rate fell by 25 basis points, the new price would beclosest to:

A. $998

B. $1,015

C. $1,032

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!