重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

A.23%

B.20%

C.30%

D.25%

答案

答案

纠错

纠错

更多“A portfolio consists of three stocks (A, B, and C), which have a 30%,20%,50% weighting, and the thre…”相关的问题

更多“A portfolio consists of three stocks (A, B, and C), which have a 30%,20%,50% weighting, and the thre…”相关的问题

第1题

第2题

According to "modem portfolio theory", we should ______.

A.buy one single kind of stocks

B.buy stocks whose prices fluctuates at the same pace

C.never sell our stocks

D.sell stocks whose prices go relatively too high in our portfolio

第4题

A、the expected return of the portfolio is less than the weighted average expected return of the stocks.

B、the expected return of the portfolio is greater than the weighted average expected return of the stocks.

C、the expected return of the portfolio is equal to the weighted average expected return of the stocks.

D、there is no relationship between the expected return of the portfolio and the expected return of the stocks.

第5题

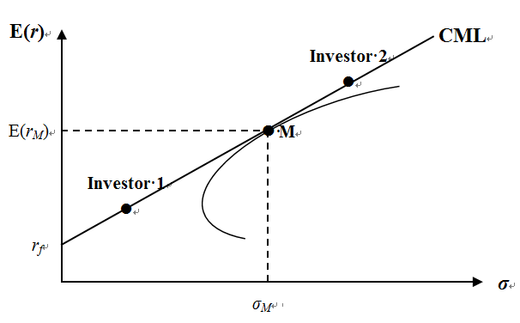

CAPM is an equilibrium theory based on the theory of portfolio selection. The following figure depicts the relation between risk and return in equilibrium, where M represents the market portfolio constructed by risky stocks. Denote that the risk-free return is rf and the expected return and risk of M are E(rM) and σM, respectively. Which of the following statements is correct?

A、The portfolio hold by Investor 2 is more efficient than the portfolio hold by Investor 1

B、Both investor 1 and investor 2 would invest the same amount of money into risky stocks

C、Investor 2 puts more money into risky stocks

D、Investor 2 isn’t a risk-seeking investor

第6题

A.return

B.portfolio

C.patent

D.budget

第7题

He had a cottage which consists _____ three rooms, a bathroom and kitchen.

A:of

B:with

C:in

D:by

第8题

A sparkler consists of three different compounds.

A.Y

B.N

C.NG

第9题

第10题

Consider a U.S. portfolio manager who holds a portfolio of French stocks currently worth €10 million. In order to hedge against a potential depreciation of the euro, the portfolio manager proposes to sell December futures contracts on the euro that currently trade at $1/€ and expire in two months. The spot exchange rate is currently $1.1/€. A month later, the value of the French portfolio is €10,050,000 and the spot exchange rate is $1.05/€, while the futures exchange rate is $0.95/€. a. Evaluate the effectiveness of the hedge by comparing the fully hedged portfolio return with the unhedged portfolio return. b. Calculate the return on the portfolio, assuming a 35 percent hedge ratio.

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!