A company has 100,000 shares of ordinary share whose par value is $1, and 50,000 10% prefe

A、$10,000

B、$30,000

C、$20,000

D、$15,000

第1题

capital of Hira Ltd from Belgrove Ltd. Belgrove Ltd currently owns 100% of the share capital of Hira Ltd and has no

other subsidiaries. All three companies have their head offices in the UK and are UK resident.

Hira Ltd had trading losses brought forward, as at 1 April 2006, of £18,600 and no income or gains against which

to offset losses in the year ended 31 March 2006. In the year ending 31 March 2007 the company expects to make

further tax adjusted trading losses of £55,000 before deduction of capital allowances, and to have no other income

or gains. The tax written down value of Hira Ltd’s plant and machinery as at 31 March 2006 was £96,000 and

there will be no fixed asset additions or disposals in the year ending 31 March 2007. In the year ending 31 March

2008 a small tax adjusted trading loss is anticipated. Hira Ltd will surrender the maximum possible trading losses

to Belgrove Ltd and Dovedale Ltd.

The tax adjusted trading profit of Dovedale Ltd for the year ending 31 March 2007 is expected to be £875,000 and

to continue at this level in the future. The profits chargeable to corporation tax of Belgrove Ltd are expected to be

£38,000 for the year ending 31 March 2007 and to increase in the future.

On 1 February 2007 Dovedale Ltd will sell a small office building to Hira Ltd for its market value of £234,000.

Dovedale Ltd purchased the building in March 2005 for £210,000. In October 2004 Dovedale Ltd sold a factory

for £277,450 making a capital gain of £84,217. A claim was made to roll over the gain on the sale of the factory

against the acquisition cost of the office building.

On 1 April 2007 Dovedale Ltd intends to acquire the whole of the ordinary share capital of Atapo Inc, an unquoted

company resident in the country of Morovia. Atapo Inc sells components to Dovedale Ltd as well as to other

companies in Morovia and around the world.

It is estimated that Atapo Inc will make a profit before tax of £160,000 in the year ending 31 March 2008 and will

pay a dividend to Dovedale Ltd of £105,000. It can be assumed that Atapo Inc’s taxable profits are equal to its profit

before tax. The rate of corporation tax in Morovia is 9%. There is a withholding tax of 3% on dividends paid to

non-Morovian resident shareholders. There is no double tax agreement between the UK and Morovia.

Required:

(a) Advise Belgrove Ltd of any capital gains that may arise as a result of the sale of the shares in Hira Ltd. You

are not required to calculate any capital gains in this part of the question. (4 marks)

第2题

第3题

Nikau Ltd to develop a new product range, under the name ‘Project Sabal’. Nikau Ltd owns shares in a non-UK

resident company, Date Inc.

The following information has been extracted from client files and from a meeting with the Finance Director of Palm

plc.

Palm plc:

– Has more than 40 wholly owned subsidiaries such that all group companies pay corporation tax at 30%.

– All group companies prepare accounts to 31 March.

– Acquired Nikau Ltd on 1 November 2007 from Facet Ltd, an unrelated company.

Nikau Ltd:

– UK resident company that manufactures domestic electronic appliances for sale in the European Union (EU).

– Large enterprise for the purposes of the enhanced relief available for research and development expenditure.

– Trading losses brought forward as at 1 April 2007 of £195,700.

– Budgeted taxable trading profit of £360,000 for the year ending 31 March 2008 before taking account of ‘Project

Sabal’.

– Dividend income of £38,200 will be received in the year ending 31 March 2008 in respect of the shares in Date

Inc.

‘Project Sabal’:

– Development of a range of electronic appliances, for sale in North America.

– Project Sabal will represent a significant advance in the technology of domestic appliances.

– Nikau Ltd will spend £70,000 on staffing costs and consumables researching and developing the necessary

technology between now and 31 March 2008. Further costs will be incurred in the following year.

– Sales to North America will commence in 2009 and are expected to generate significant profits from that year.

Shares in Date Inc:

– Nikau Ltd owns 35% of the ordinary share capital of Date Inc.

– The shares were purchased from Facet Ltd on 1 June 2003 for their market value of £338,000.

– The sale was a no gain, no loss transfer for the purposes of corporation tax.

– Facet Ltd purchased the shares in Date Inc on 1 March 1994 for £137,000.

Date Inc:

– A controlled foreign company resident in the country of Palladia.

– Annual chargeable profits arising out of property investment activities are approximately £120,000, of which

approximately £115,000 is distributed to its shareholders each year.

The tax system in Palladia:

– No taxes on income or capital profits.

– 4% withholding tax on dividends paid to shareholders resident outside Palladia.

Required:

(a) Prepare detailed explanatory notes, including relevant supporting calculations, on the effect of the following

issues on the amount of corporation tax payable by Nikau Ltd for the year ending 31 March 2008.

(i) The costs of developing ‘Project Sabal’ and the significant commercial changes to the company’s

activities arising out of its implementation. (8 marks)

第4题

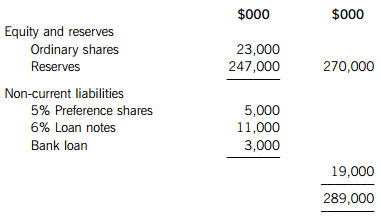

The ordinary shares of Dinla Co are currently trading at $4·26 per share on an ex dividend basis and have a nominal value of $0·25 per share. Ordinary dividends are expected to grow in the future by 4% per year and a dividend of $0·25 per share has just been paid.

The 5% preference shares have an ex dividend market value of $0·56 per share and a nominal value of $1·00 per share. These shares are irredeemable.

The 6% loan notes of Dinla Co are currently trading at $95·45 per loan note on an ex interest basis and will be redeemed at their nominal value of $100 per loan note in five years’ time.

The bank loan has a fixed interest rate of 7% per year.

Dinla Co pays corporation tax at a rate of 25%.

Required:

(a) Calculate the after-tax weighted average cost of capital of Dinla Co on a market value basis. (8 marks)

(b) Discuss the connection between the relative costs of sources of finance and the creditor hierarchy. (3 marks)

(c) Explain the differences between Islamic finance and other conventional finance. (4 marks)

第5题

A.his voting rights are considered more important

B.he has the greater right in choosing the board of directors

C.he receives his dividend before the ordinary shareholder

D.he has the right to buy ordinary shares more cheaply

第6题

A、$82,500

B、$85,000

C、$102,500

D、$105,000

第7题

A.not include the options because they are antidilutive.

B.include the options because they could dilute earnings.

C.not include the options because they cannot be exercised until June 30, 2003.

D.include the options because the shares declined in price during 2001.

第8题

higher rate.

Andrew is considering investing in a new business, and to provide funds for this investment he has recently disposed

of the following assets:

(1) A short leasehold interest in a residential property. Andrew originally paid £50,000 for a 47 year lease of the

property in May 1995, and assigned the lease in May 2006 for £90,000.

(2) His holding of £10,000 7% Government Stock, on which interest is payable half-yearly on 20 April and

20 October. Andrew originally purchased this holding on 1 June 1999 for £9,980 and he sold it for £11,250

on 14 March 2005.

Andrew intends to subscribe for ordinary shares in a new company, Scalar Limited, which will be a UK based

manufacturing company. Three investors (including Andrew) have been identified, but a fourth investor may also be

invited to subscribe for shares. The investors are all unconnected, and would subscribe for shares in equal measure.

The intention is to raise £450,000 in this manner. The company will also raise a further £50,000 from the investors

in the form. of loans. Andrew has been told that he can take advantage of some tax reliefs on his investment in Scalar

Limited, but does not know anything about the details of these reliefs

Andrew’s employer, Bestadvice & Co, is proposing to change the staff pension scheme from a defined benefit scheme

to which the firm and the employees each contribute 6% of their annual salary, to a defined contribution scheme, to

which the employees will continue to contribute 6%, but the firm will contribute 8% of their annual salary. The

majority of Andrew’s colleagues are opposed to this move, but, given the increase in the firm’s contribution rate

Andrew himself is less sure that the proposal is without merit.

Required:

(a) (i) Calculate the chargeable gain arising on the assignment of the residential property lease in May 2006.

(2 marks)

第9题

A.Where the company is to offer its shares to its senior executives

B.Where the company is to reduce its registered capital

C.Where the company is to fix the price of its stocks in the securities market

D.Where the company merges with another company which holds its shares

第10题

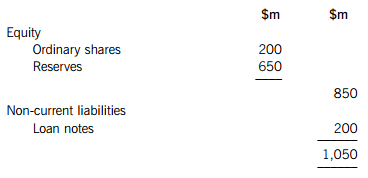

The ordinary shares of Tinep Co have a nominal value of 50 cents per share and are currently trading on the stock market on an ex dividend basis at $5·85 per share. Tinep Co has an equity beta of 1·15.

The loan notes have a nominal value of $100 and are currently trading on the stock market on an ex interest basis at $103·50 per loan note. The interest on the loan notes is 6% per year before tax and they will be redeemed in six years’ time at a 6% premium to their nominal value.

The risk-free rate of return is 4% per year and the equity risk premium is 6% per year. Tinep Co pays corporation tax at an annual rate of 25% per year.

Required:

(a) Calculate the market value weighted average cost of capital and the book value weighted average cost of capital of Tinep Co, and comment briefly on any difference between the two values. (9 marks)

(b) Discuss the factors to be considered by Tinep Co in choosing to raise funds via a rights issue. (6 marks)