重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

PART C

Directions: You will hear three dialogues or monologues. Before listening to each one, you will have 5 seconds to read each of the questions which accompany it. While listening, answer each question by choosing A, B, C or D. After listening, you will have 10 seconds to check your answer to each question. You will hear each piece ONLY ONCE.

听力原文: A balanced diet contains proteins, which are composed of complex amino acids. There are 20 types of amino acids, comprising about 16 percent of the body weight in a lean individual. A body needs all 20 to be healthy. Amino acids can be divided into two groups: essential and nonessential. There are nine essential amino acids. These are the proteins that the body cannot produce by itself, so a healthy individual must ingest them. The 11 nonessential amino acids, on the other hand, are produced by the body, so it is not necessary to ingest them. Proteins are described as being either high-quality or low-quality. This refers to how many of the nine essential amino acids the food contains. High-quality proteins, typically found in animal meats, are proteins which have ample amounts of the essential amino acids. Low-quality proteins are mainly plant proteins and usually lack one or more of the essential amino acids. Since people who follow a strict vegetarian diet are ingesting only low-quality proteins, they must make sure that their diets contain a variety of proteins, in order to insure that what is lacking in one food is available in another. The process of selecting a variety of the essential proteins is called protein complementation. Since an insufficient amount of protein in the diet can be crippling, and prolonged absence of proteins can cause death, it is imperative that a vegetarian diet contains an ample amount of the essential proteins.

What is the main topic of this talk?

A.Proteins.

B.Low-quality protins.

C.Poor dietary habits.

D.Healthy diets.

更多“PART CDirections: You will hear three dialogues or monologues. Before listening to each on”相关的问题

更多“PART CDirections: You will hear three dialogues or monologues. Before listening to each on”相关的问题

第1题

甲公司2008年末“递延所得税负债”科目的贷方余额为90万元(均为固定资产后续计量对所得税的影响),适用的所得税税率为18%。2009年初适用所得税税率改为25%。2009年末固定资产的账面价值为6 000万元,计税基础为5 800万元,2009年确认销售商品提供售后服务的预计负债100万元,年末预计负债的账面价值为100万元,计税基础为0。甲公司预计会持续盈利,各年能够获得足够的应纳税所得额。则甲公司2009年末确认递延所得税时应做的会计分录为()。

第2题

甲公司2008年末“递延所得税负债”科目的贷方余额为90万元(均为固定资产后续计量对所得税的影响),适用的所得税税率为18%。2009年初适用所得税税率改为25%。2009年末固定资产的账面价值为6 000万元,计税基础为5 800万元,2009年确认销售商品提供售后服务的预计负债100万元,年末预计负债的账面价值为100万元,计税基础为0。甲公司预计会持续盈利,各年能够获得足够的应纳税所得额。不考虑其他因素则甲公司2009年末确认递延所得税时应做的会计分录为()。

第3题

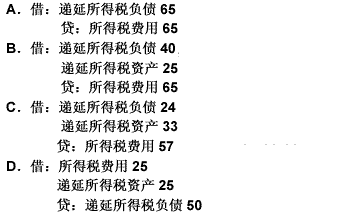

甲公司2011年末“递延所得税负债”科目的贷方余额为90万元(均为固定资产后续计量对所得税的影响),适用的所得税税率为l8%。2012年初适用所得税税率改为25%。2012年末固定资产的账面价值为6 000万元,计税基础为5 800万元,2012年确认销售商品提供售后服务的预计负债100万元,年末预计负债的账面价值为100万元,计税基础为0。甲公司预计会持续盈利,各年能够获得足够的应纳税所得额。不考虑其他因素则甲公司2012年末确认递延所得税时应做的会计分录为()。

A.借:递延所得税负债65 贷:所得税费用65

B.借:递延所得税负债40 递延所得税资产25 贷:所得税费用65

C.借:递延所得税负债24 递延所得税资产33 贷:所得税费用57

D.借:所得税费用25 递延所得税资产25 贷:递延所得税负债50

第4题

甲公司2008年末“递延所得税负债”科目的贷方余额为90万元(均为固定资产后续量对所得税的影响),适用的所得税税率为18%。2009年初适用所得税税率改为25%。2009年末固定资产的账面价值为6000万元,计税基础为5800万元,2009年确认销售商品提供售后服务的预计负债100万元,年末预计负债的账面价值为100万元,计税基础为0。甲公司预计会持续盈利,各年能够获得足够的应纳税所得额。不考虑其他因素

则甲公司2009年末确认递延所得税时应做的会计分录为()。

第5题

甲公司2011年末“递延所得税负债”科目的贷方余额为90万元(均为固定资产后续计量对所得税的影响),适用的所得税税率为18%。2012年初适用所得税税率改为25%。2012年末固定资产的账面价值为6000万元,计税基础为5800万元,2012年确认销售商品提供售后服务的预计负债100万元,年末预计负债的账面价值为100万元,计税基础为0。甲公司预计会持续盈利,各年能够获得足够的应纳税所得额。不考虑其他因素。则甲公司2012年末确认递延所得税时应做的会计分录是()。

A.借:递延所得税负债65 贷:所得税费用65

B.借:递延所得税负债40 递延所得税资产25 贷:所得税费用65

C.借:递延所得税负债24 递延所得税资产33 贷:所得税费用57

D.借:所得税费用25 递延所得税资产25 贷:递延所得税负债50

第6题

A.借:递延所得税负债 65 贷:所得税费用 65

B.借:递延所得税负债 40 递延所得税资产 25 贷:所得税费用 65

C.借:递延所得税负债 24 递延所得税资产 33 贷:所得税费用 57

D.借:所得税费用 25 递延所得税资产 25 贷:递延所得税负债 50

第7题

A.借:递延所得税负债 65 贷:所得税费用 65

B.借:递延所得税负债 40 递延所得税资产 25 贷:所得税费用 65

C.借:递延所得税负债 24 递延所得税资产 33 贷:所得税费用 57

D.借:所得税费用 25 递延所得税资产 25 贷:递延所得税负债 50

第8题

A.借:递延所得税负债49贷:所得税费用49

B.借:递延所得税负债54递延所得税资产33贷:所得税费用87

C.借:递延所得税负债49递延所得税资产25贷:所得税费用74

D.借:所得税费用24递延所得税资产25贷:递延所得税负债49

第9题

A.借:递延所得税负债65贷:所得税费用65

B.借:递延所得税负债40递延所得税资产25贷:所得税费用65

C.借:递延所得税负债24递延所得税资产33贷:所得税费用57

D.借:所得税费用25递延所得税资产25贷:递延所得税负债50

第10题

甲公司2008年末“递延所得税资产”科目的借方余额为69万元(均为固定资产后续计量对所得税的影响)。甲公司预计会持续盈利,各年能够获得足够的应纳税所得额,适用的所得税税率为25%。2009年末固定资产的账面价值为6200万元,计税基础为6800万元,2009年因产品质量保证确认预计负债120万元,税法规定,产品质量保证支出在实际发生时允许税前扣除。不考虑其他因素,则甲公司2009年应确认的递延所得税收益为()万元。

A.111

B.180

C.150

D.30

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!