重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

A.Reduction of friction

B.Insulation of hot surfaces

C.Lubrication of moving parts

D.Elevation of cooler outlet temperatures

更多“Machinery operating features are designed to help conserve energyWhich of the following re”相关的问题

更多“Machinery operating features are designed to help conserve energyWhich of the following re”相关的问题

第1题

A、Operating leases,and account for inventory using last-in first-out.

B、sales-type leases,and account for inventory using specific identification.

C、Direct financing leases,and account for inventory using weighted average cost.

第2题

A.The number of the machines in a cost center

B.The value of the machines in a cost center

C.The floor area occupied by the machines in each cost center

D.The operating hours of machines in each cost center

第3题

第4题

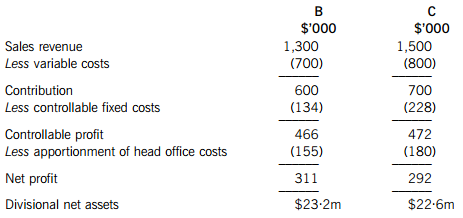

The Biscuits division (Division B) and the Cakes division (Division C) are two divisions of a large, manufacturing company. Whilst both divisions operate in almost identical markets, each division operates separately as an investment centre. Each month, operating statements must be prepared by each division and these are used as a basis for performance measurement for the divisions.

Last month, senior management decided to recharge head office costs to the divisions. Consequently, each division is now going to be required to deduct a share of head office costs in its operating statement before arriving at ‘net profit’, which is then used to calculate return on investment (ROI). Prior to this, ROI has been calculated using controllable profit only. The company’s target ROI, however, remains unchanged at 20% per annum. For each of the last three months, Divisions B and C have maintained ROIs of 22% per annum and 23% per annum respectively, resulting in healthy bonuses being awarded to staff. The company has a cost of capital of 10%.

The budgeted operating statement for the month of July is shown below:

Required

(a) Calculate the expected annualised Return on Investment (ROI) using the new method as preferred by senior management, based on the above budgeted operating statements, for each of the divisions. (2 marks)

(b) The divisional managing directors are unhappy about the results produced by your calculations in (a) and have heard that a performance measure called ‘residual income’ may provide more information. Calculate the annualised residual income (RI) for each of the divisions, based on the net profit figures for the month of July. (3 marks)

(c) Discuss the expected performance of each of the two divisions, using both ROI and RI, and making any additional calculations deemed necessary. Conclude as to whether, in your opinion, the two divisions have performed well. (6 marks)

(d) Division B has now been offered an immediate opportunity to invest in new machinery at a cost of $2·12 million. The machinery is expected to have a useful economic life of four years, after which it could be sold for $200,000. Division B’s policy is to depreciate all of its machinery on a straight-line basis over the life of the asset. The machinery would be expected to expand Division B’s production capacity, resulting in an 8·5% increase in contribution per month.

Recalculate Division B’s expected annualised ROI and annualised RI, based on July’s budgeted operating statement after adjusting for the investment. State whether the managing director will be making a decision that is in the best interests of the company as a whole if ROI is used as the basis of the decision. (5 marks)

(e) Explain any behavioural problems that will result if the company’s senior management insist on using solely ROI, based on net profit rather than controllable profit, to assess divisional performance and reward staff. (4 marks)

第5题

第三组:

Ship recycling contributes to sustainable development and is the environmentally friendly way of disposing of ships with virtually every part of the hull, machinery, equipment, fittings and even furniture being re-used. However, while the principle of ship recycling is a sound one, the reported status of working practices and environmental standards in recycling facilities often leaves much to be desired. Such growing concerns about environmental safety, health and welfare matters in the ship recycling industry have resulted in a growing belief that an international instrument to regulate the ship recycling process is urgently needed.

Having become aware of the need to reduce the environmental, occupational health and safety risks related to ship recycling, as well as the need to secure the smooth withdrawal of ships that have reached the end of their operating lives, the International Maritime Organization (IMO) has taken action to develop a realistic and effective solution to the problem of ship recycling, which will take into account the particular characteristics of international maritime transport and the economic realities.

Which statement of the following is true?

A.Ship recycling is sustainable

B.Ship recycling is very friendly to our environment

C.Ship recycling is the best way to dispose the machinery, equipment, fittings and even furniture on board

D.Ship recycling brings many problems concerning environmental safety, health and______occupational safety

第6题

材料:

Pride of Le Havre is a 33,336 gross tonnage passenger/ro-ro cargo vessel operating a regular ferry service between Portsmouth and Le Havre.The vessel is fitted with bow and stern doors and is capable of carrying 590 cars and 1600 passengers.Propulsion is by four diesel engines driving through two controllable pitch propellers.Two transverse thrust units are fitted forward.

The vessel had sailed from A&P&39;s King George V dry dock,Southampton,just after midnight on Thursday 18 March,for engine trials.The intention was that after these trials,Pride of Le Havre would berth at Portsmouth,and re-enter service later that day.

Shortly after passing the Nab Tower,the bridge fire alarm activated at 0425,indicating a fire in the machinery spaces.At about the same time,a motorman reported to the engineer watchkeeper that a fire had broken out on the starboard thermal oil pump.While initial attempts were being made to put the fire out using portable extinguishers,the chief engineer was called and the bridge informed of the situation.On confirming that the initial attempt had failed,the chief engineer advised the bridge that he proposed to use the Halon total flooding extinguishing system.The general alarm was sounded and the main engines stopped. The engine room was evacuated and sealed,with Halon being released at 0437.The coastguard and owners were told of the situation with a message being broadcast to local shipping.

A fire brigade team boarded at 0641 with re-entry to machinery space at 0958.Funnel vents were re-opened at 1030 with a fire extinguishing foam blanket laid down in the main machinery space.Ventilation of the engine room started at 1210 with full electrical power available by 1330.Under the direction of the chief engineer,the engine room crew started systematically checking and preparing machinery until,at 1750,No 4 main engine was started followed shortly afterwards by No 1 main engine.

Pride of Le Havre sailed under her own power back to Southampton where she re-entered the dry dock berth to undergo examination and repair.She was all fast alongside at 0033 on Friday 19 March 1999.

问题:

Pride of Le Havre is equipped with ________.

A.4 transverse thrust units,2 propellers,2 engines and 2 vehicle doors

B.2 transverse thrust units,2 propellers,2 engines and 1 vehicle door

C.2 transverse thrust units,1 propeller,2 engines and 2 vehicle doors

D.2 transverse thrust units,2 propellers,4 engines and 2 vehicle doors

The fire was put out by ________.A.a fire brigade team

B.the coastguard

C.owners

D.the crew

Should she have not been on fire,Pride of Le Havre would have re-entered the service on ________.A.Friday

B.Thursday

C.19 March

D.any day after 18 March

The using of the Halon total flooding extinguishing system was initially suggested by ________.A.the engineer watchkeeper

B.a motorman

C.the coastguard and owners

D.the chief engineer

请帮忙给出每个问题的正确答案和分析,谢谢!

第7题

Computer question NSJCT is considering a project that requires initial investment of €150,000 in new machinery. The project will be shut down at the end of four years. The following is the projected cash flow from the project: Year 1 2 3 4 Sales €120,000 €120,000 €140,000 €140,000 Operating expenses €40,000 €40,000 €50,000 €50,000 The firm can raise funds at 8% and its tax rate is 45%. In Lesson 5 when depreciation was first introduced, it was mentioned that the different methods of depreciation for tax purposes will result in different tax shields. In this exercise, you will examine the effects of this difference. In part (a) you will calculate the after-tax cash flows that would occur if straight-line depreciation were an allowable expense for tax purposes. You will compare this to the cash flows in part (b) where a declining balance method is used. You will use the same worksheet for both parts. a. Assume that the proposed machinery is to be depreciated over four years on a straight-line basis, with no salvage value at the end of the four years. For this part, assume that the depreciation expense can be deducted from income to calculate the net tax for NSJCT. Use Excel file I-FN1L6Q1 to compute the net present value and the internal rate of return for this project over four years. b. Assume depreciation for tax purposes is to be taken using the declining-balance method at the rate of 20% for capital cost allowance. For this part, assume the machinery will have a salvage value of €30,000 at the end of year 4, and that the asset class to which it belongs will not be left empty by the sale of the machinery at that time, and that the half year rule does not apply to the salvage value. Use Excel file I-FN1L6Q1 to compute the net present value and the internal rate of return for this project. Also compute the net cash flow from this project for each of the four years. Compare the results from parts (a) and (b) and comment on the difference.

第8题

Question 9

A & D Ltd. provides you with the following information for the two years ended 31 December years 2002 and 2003.

Balance Sheet ended at 31 December

2002 2003

$'000 $'000

Plant and machinery 1,346 1,838

Less: Depreciation (224) (337)

Stock 234 346

Trade debtors 432 540

Bank and cash 60 414

Trade creditors (192) (216)

Accrued expenses (20) —

Taxation (80) (90)

Dividends (45) (60)

1,511 2,435

Less: 7% Debentures (350) (1,000) 1,161 1,435

Paid-up share capital 900 1,000

Share premium — 100

Revenue reserves 85 120

Profit and loss 176 215 1,161 1,435

Trading and Profit and Loss Account

2002 2003

$'000 $'000

Turnover 2,775 3,254

Less: Cost of sales (1,816) (2,245)

Gross profit 959 1,009

Less: Operating expenses (763) (765)

Profit before taxation 196 244

Less: taxation (80) (90)

Profit after taxation 116 154

Less: transfer to reserves (20) (35)

proposed dividends (45) (80)

Retained earnings for the year 51 39

Additional information:

Plant and machinery with a cost of $62,000 and a written-down value of $24,800 was sold for$12,000.

Required:

(a)Briefly state the purposes of preparing a cash flow statement.

(b)Prepare a cash flow statement for A & D Ltd. for the year ended 31 December 2003 in the format as prescribed by HKSSAP15: Cash Flow Statement.

第9题

Question 9

The following financial statements relate to Blue Ting for the year ended 31 December 2001

Balance Sheet ended at 31 December

2000 2001

$'000 $'000

Plant and machinery 1,296 1,788

Less: Depreciation (174) (287)

Stock 184 296

Trade debtors 382 490

Bank and cash 10 (301)

Trade creditors (142) (166)

Accrued expenses (45) -

Taxation (80) (100)

Dividends (45) (60)

1,386 1,660

Less: 6% Loan notes2009 (350) (350) 1,036 1,310

Paid-up share capital 875 975

Share premium - 50

Revenue reserves 35 70

Profit and loss 126 215 1,036 1,310

Trading and Profit and Loss Account

2000 2001

$'000 $'000

Turnover 2,725 3,204

Less: Cost of sales (1,766) (2,195)

Gross profit 959 1,009

Less: Operating expenses (713) (715)

Profit before taxation 246 294

Less: taxation (80) (90)

Profit after taxation 166 204

Less: transfer to reserves (20) (35)

proposed dividends (45) (80)

Retained earnings for the year 101 89

Additional information:

Plant and machinery with a cost of $52,000 and a written-down value of $22,800 was sold for$10,000.

Required:

(a)Briefly discuss why users regard cash flow analysis importantly.

(b)Prepare a cash flow statement for Blue Ting for the year ended 31 December 2001 in the format as prescribed by HKSSAP15: Cash Flow Statement.

第10题

Initial investment $2 million

Selling price (current price terms) $20 per unit

Expected selling price inflation 3% per year

Variable operating costs (current price terms) $8 per unit

Fixed operating costs (current price terms) $170,000 per year

Expected operating cost inflation 4% per year

The research and development division has prepared the following demand forecast as a result of its test marketing trials. The forecast reflects expected technological change and its effect on the anticipated life-cycle of Product W33.

It is expected that all units of Product W33 produced will be sold, in line with the company’s policy of keeping no inventory of finished goods. No terminal value or machinery scrap value is expected at the end of four years, when production of Product W33 is planned to end. For investment appraisal purposes, PV Co uses a nominal (money) discount rate of 10% per year and a target return on capital employed of 30% per year. Ignore taxation.

Required:

(a) Identify and explain the key stages in the capital investment decision-making process, and the role of

investment appraisal in this process. (7 marks)

(b) Calculate the following values for the investment proposal:

(i) net present value;

(ii) internal rate of return;

(iii) return on capital employed (accounting rate of return) based on average investment; and

(iv) discounted payback period. (13 marks)

(c) Discuss your findings in each section of (b) above and advise whether the investment proposal is financially acceptable. (5 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!