重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

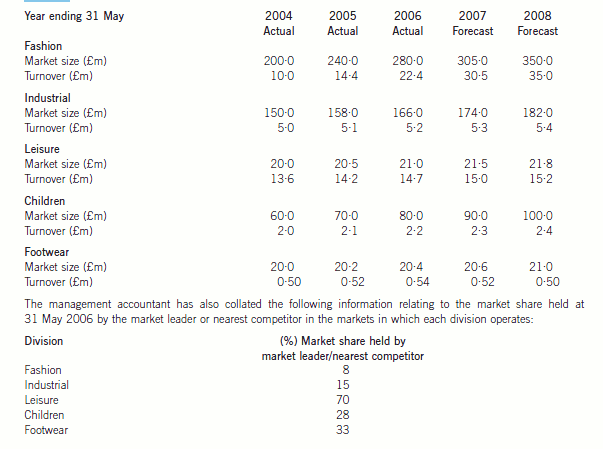

3 The Specialist Clothing Company Ltd (SCC Ltd) is a manufacturer of a wide range of clothing. Its operations are

organised into five divisions which are as follows:

(i) Fashion

(ii) Industrial

(iii) Leisure

(iv) Children

(v) Footwear

The Fashion division manufactures a narrow range of high quality clothing which is sold to a leading retail store which

has branches in every major city in its country of operation. The products have very short life cycles.

The Industrial division manufactures a wide range of clothing which has been designed for use in industrial

environments. In an attempt to increase sales volumes, SCC Ltd introduced the sale of these products via mail order

with effect from 1 June 2005.

The Leisure division manufactures a narrow range of clothing designed for outdoor pursuits such as mountaineering

and sky diving, which it markets under its own, well-established ‘Elite’ brand label.

The Children division manufactures a range of school and casual wear which is sold to leading retail stores.

The Footwear division manufactures a narrow range of footwear.

The management accountant of SCC Ltd has gathered the following actual and forecast information relating to the five

divisions:

Required:

(a) Use the Boston Consulting Group matrix in order to assess the competitive position of SCC Ltd. (10 marks)

更多“3 The Specialist Clothing Company Ltd (SCC Ltd) is a manufacturer of a wide range of cloth”相关的问题

更多“3 The Specialist Clothing Company Ltd (SCC Ltd) is a manufacturer of a wide range of cloth”相关的问题

第1题

the country of Mayland.

Each centre offers dietary plans and fitness programmes to clients under the supervision of dieticians and fitness

trainers. Residential accommodation is also available at each centre. The centres are located in the towns of Ayetown,

Beetown and Ceetown.

The following information is available:

(1) Summary financial data for HFG in respect of the year ended 31 May 2008.

(2) HFG defines Residual Income (RI) for each centre as operating profit minus a required rate of return of 12% of

the total assets of each centre.

(3) At present HFG does not allocate the long-term borrowings of the group to the three separate centres.

(4) Each centre faces similar risks.

(5) Tax is payable at a rate of 30%.

(6) The market value of the equity capital of HFG is $9 million. The cost of equity of HFG is 15%.

2

(7) The market value of the long-term borrowings of HFG is equal to the book value.

(8) The directors are concerned about the return on investment (ROI) generated by the Beetown centre and they are

considering using sensitivity analysis in order to show how a target ROI of 20% might be achieved.

(9) The marketing director stated at a recent board meeting that ‘The Group’s success depends on the quality of

service provided to our clients. In my opinion, we need only to concern ourselves with the number of complaints

received from clients during each period as this is the most important performance measure for our business.

The number of complaints received from clients is a perfect performance measure. As long as the number of

complaints received from clients is not increasing from period to period, then we can be confident about our

future prospects’.

Required:

(a) The directors of HFG have asked you, as management accountant, to prepare a report providing them with

explanations as to the following:

(i) Which of the three centres is the most ‘successful’? Your report should include a commentary on return

on investment (ROI), residual income (RI), and economic value added (EVA) as measures of financial

performance. Detailed calculations regarding each of these three measures must be included as part of

your report;

Note: a maximum of seven marks is available for detailed calculations. (14 marks)

第2题

1 The Geeland Bus Company (GBC) is a partly government-funded organisation which provides transport services to

the population of Geeland, a country which is divided into four regions i.e. Northern, Eastern, Southern and Western.

The Western region differs from the Northern, Eastern and Southern regions in that it is a rural area with a low

population.

The Terrific Transport Company (TTC) is a privately owned organisation which also provides transport services to the

population of Geeland. All TTC buses are luxuriously fitted; each passenger has their own television and all buses

have on-board catering facilities which serve a variety of drinks and snacks. The costs of these luxuries are included

in fares charged by TTC.

Both GBC and TTC operate from premises in the Northern region. GBC operates a bus service to and from the Eastern,

Southern and Western regions as well as a ‘Hopper’ service which takes passengers around all regions, other than

the Western region, within Geeland. TTC also operates a bus service to and from the Eastern and Southern regions of

Geeland as well as a Hopper service. TTC does not operate a service to and from the Western region.

The following information is available:

(1) A summary of the financial performance of GBC and TTC for the years ended 30 November 2006 and 2007 is

as follows:

(12) At a meeting of the board of directors held during 2007, the managing director of GBC stated that: ‘on no account

shall we discontinue the operation of our Western route’.

Required:

(a) Prepare a report on the operating performance and financial performance of GBC and TTC for the years

ended 30 November 2006 and 2007. As part of your report, you should include an appendix showing

detailed workings of how each of the six figures marked with an asterisk (*) in note 1 has been calculated.

(23 marks)

Note: 6 marks are available in respect of the six figures marked with an asterisk (*). 17 marks are available

for other calculations and discussion, including 4 professional marks.

第3题

ctivities. All applications by

divisional management teams for funds with which to undertake capital projects require the authorisation of the board

of directors of NCL plc. Once authorisation has been granted to a capital application, divisional management teams

are allowed to choose the project for investment.

Under the terms of the management incentive plan, which is currently in operation, the managers of each division

are eligible to receive annual bonus payments which are calculated by reference to the return on investment (ROI)

earned during each of the first two years by new investments. ROI is calculated using the average capital employed

during the year. NCL plc depreciates its investments on a straight-line basis.

One of the most profitable divisions during recent years has been the IOA Division, which is engaged in the mining

of precious metals. The management of the IOA Division is currently evaluating three projects relating to the extraction

of substance ‘xxx’ from different areas in its country of operation. The management of the IOA Division has been given

approval by the board of directors of NCL plc to spend £24 million on one of the three proposals it is considering (i.e.

North, East and South projects).

The following net present value (NPV) calculations have been prepared by the management accountant of the IOA

Division.

第4题

Universities in Teeland have three stated objectives:

1. To improve the overall standard of education of citizens in Teeland.

2. To engage in high quality academic research.

3. To provide well-qualified university graduates to meet the needs of the graduate jobs market in Teeland.

Each university is funded by a fixed sum of money from the Teeland government according to the number of students studying there. In addition, universities receive extra funds from the government and also from other organisations, such as large businesses and charities. These funds are used to support academic research.

Following the onset of an economic recession, the Teeland government has stated its intention to reduce spending on publicly funded services such as the universities. One senior politician, following his recent visit to neighbouring Veeland, was controversially quoted as saying:

‘The universities in Veeland offer much better value for money for the citizens there compared to our universities here in Teeland. There are 25 students for each member of academic staff in Veeland, whereas in Teeland, the average number is 16, and yet, the standard of education of citizens is much higher in Veeland. The Veeland government sets targets for many aspects of the services delivered by all the universities in Veeland. Furthermore, league tables of the performance of individual universities are published on the internet, and university leaders are given bonuses if their university falls within the top quarter of the league table. In Veeland, the system of performance measurement of the universities is considered so important that there is a special government department of 150 staff just to measure it.’

He went on to add, ‘I want to see a similar system of league tables, targets and bonuses for university leaders being introduced here in Teeland. To appear near the top of the league tables, I think we should expect each university to increase the number of graduates entering graduate jobs by at least 5% each year. I would also like to see other steps taken to increase value for money, such as reducing the number of academic staff in each university and reducing the salary of newly recruited academic staff.’

You have been asked to advise the Teeland government on the measurement of value for money of the universities and the proposed introduction of league tables for comparing their performance. Appendix A contains details and existing performance data relating to four of the best known universities in Teeland.

Northcity University is famous for its high teaching standards and outstanding academic research in all subjects. As such, it attracts the most able students from all parts of the world to study there.

Southcity University is a large university in the capital city of Teeland and offers courses in a wide range of subjects, though most of the funding it receives for academic research is for science and technology in which it is particularly successful.

Eastcity University is a small university specialising in the teaching of arts and humanities subjects such as history and geography.

Westcity University currently offers less strict entry standards to students to attract students from more diverse backgrounds, who may not normally have the opportunity of a university education.

Appendix A

Existing university performance data

Key to performance data

1 – Entry requirements represent students’ average attainment in examinations prior to entering university. The entry requirement of the highest ranking university is scored as 100, with the score of all other universities being in proportion to that score.

2 – The number of graduates each year who go on to further study or who begin jobs normally undertaken by university graduates. In Teeland, students attend university for an average of 3·2 years.

3 – The TSOR (Teeland students overall satisfaction rating) survey is undertaken by the Teeland government to assess students’ overall satisfaction with the standard of teaching, the social and support aspects of university life and their optimism for their own future job prospects.

4 – The education department of the Teeland government has produced a provisional league table ranking the overall performance of each of the 45 universities in Teeland, with 1 being the highest ranking university. This has been compiled using a number of performance measures, weighted according to what the government believes are the most important of these measures.

Required:

(a) Advise the Teeland government how it could assess the value for money of the universities in Teeland, using the performance data in Appendix A. (12 marks)

(b) Assess the potential benefits of league tables for improving the performance of universities in Teeland and discuss the problems of implementing the proposal to introduce league tables. (13 marks)

第5题

s for use in the construction industry. Dibble has always absorbed production overheads to the cost of each product on the basis of machine hours.

Timber Division

Timber Division manufactures timber frames used to support the roofs of new houses. The timber, which is purchased pre-cut to the correct length, is assembled into the finished frame. by a factory worker who fastens the components together. Timber Division manufactures six standard sizes of frame. which is sufficient for use in most newly built houses.

Steel Division

Steel Division manufactures steel frames and roof supports for use in small commercial buildings such as shops and restaurants. There is a large range of products, and many customers also specify bespoke designs for short production runs or one-off building projects. Steel is cut and drilled using the division’s own programmable computer aided manufacturing machinery (CAM), and is bolted together or welded by hand.

Steel Division’s strategy is to produce novel bespoke products at a price comparable to the simpler and more conventional products offered by its competitors. For example, many of Steel Division’s customers choose to have steel covered in one of a wide variety of coloured paints and other protective coatings at the end of the production process. This is performed off-site by a subcontractor, after which the product is returned to Steel Division for despatch to the customer. Customers are charged the subcontractor’s cost plus a 10% mark up for choosing this option. The board of Steel Division has admitted that this pricing structure may be too simplistic, and that it is unsure of the overall profitability of sales of some groups of products or sectors of the market.

Recently, several customers have complained that incorrectly applied paint has flaked off the steel after only a few months’ use. More seriously, a fast food restaurant has commenced litigation with Dibble after it had to close for a week while steel roof frames supplied by Steel Division were repainted. Following this, the production manager has proposed increasing the number of staff inspecting the quality of coating on the frames, and purchasing expensive imaging machinery to make inspection more efficient.

The chief executive officer (CEO) at Dibble has approached you as a performance management expert for your advice. ‘At a conference recently’, he told you, ‘I watched a presentation by a CEO at a similar business to ours talking about the advantages and disadvantages of using activity based costing (ABC) and how over several years the adoption of activity based management (ABM) had helped them to improve both strategic and operational performance.’

‘I don’t want you to do any detailed calculations at this stage, but I’d like to know more about ABC and ABM, and know whether they would be useful for Dibble’, he said.

You are provided with extracts of the most recent management accounts for Timber and Steel Divisions:

Required:

(a) (i) Advise the CEO how activity based costing could be implemented. (4 marks)

(ii) Assess whether it may be more appropriate to use activity based costing in Timber and Steel Divisions than the costing basis currently used. (8 marks)

(b) Advise the CEO how activity based management could be used to improve business performance in Dibble. (13 marks)

第6题

Section B – TWO questions ONLY to be attempted

Cuthbert is based in Ceeland and manufactures jackets for use in very cold environments by mountaineers and skiers. It also supplies the armed forces in several countries with variants of existing products, customised by the use of different coloured fabrics, labels and special fastenings for carrying equipment. Cuthbert incurs high costs on design and advertising in order to maintain the reputation of the brand.

Each jacket is made up of different shaped pieces of fabric called ‘components’. These components are purchased by Cuthbert from an external supplier. The external supplier is responsible for ensuring the quality of the components and the number of purchased components found to be defective is negligible. The cost of the components forms 80% of the direct cost of each jacket, and the prices charged by Cuthbert’s supplier for the components are the lowest in the industry. There are three stages to the production process of each jacket, which are each located in different parts of the factory:

Stage 1 – Sewing

The fabric components are sewn together by a machinist. Any manufacturing defects occurring after sewing has begun cannot be rectified, and finished garments found to be defective are heavily discounted, or in the case of bespoke variants, destroyed.

Stage 2 – Assembly

The garments are filled with insulating material and sewn together for the final time.

Stage 3 – Finishing

Labels, fastenings and zips are sewn to the finished garments. Though the process for attaching each of these is similar, machinists prefer to work only on labels, fastenings or zips to maximise the quantity which they can sew each hour.

Jackets are produced in batches of a particular style. in a range of sizes. Throughout production, the components required for each batch of jackets are accompanied by a paper batch card which records the production processes which each batch has undergone. The batch cards are input into a production spreadsheet so that the stage of completion of each batch can be monitored and the position of each batch in the factory is recorded.

There are 60 machinists working in the sewing department, and 40 in each of the assembly and finishing departments. All the machinists are managed by 10 supervisors whose duties include updating the batch cards for work done and inputting this into a spreadsheet, as well as checking the quality of work done by machinists. The supervisors report to the factory manager, who has overall responsibility for the production process.

Machinists are paid an hourly wage and a bonus according to how many items they sew each week, which usually comprises 60% of their total weekly wages.

Supervisors receive an hourly wage and a bonus according to how many items their team sews each week. The factory manager receives the same monthly salary regardless of production output. All employees are awarded a 5% annual bonus if Cuthbert achieves its budgeted net profit for the year.

Recently, a large emergency order of jackets for the Ceeland army was cancelled by the customer as it was not delivered on time due to the following quality problems and other issues in the production process:

– A supervisor had forgotten to input several batch cards and as a result batches of fabric components were lost in the factory and replacements had to be purchased.

– There were machinists available to sew buttons onto the jackets, but there was only one machinist available who had been trained to sew zips. This caused further delay to production of the batch.

– When the quality of the jackets was checked prior to despatch, many of them were found to be sewn incorrectly as the work had been rushed. By this time the agreed delivery date had already passed, and it was too late to produce a replacement batch.

This was the latest in a series of problems in production at Cuthbert, and the directors have decided to use business process reengineering (BPR) in order to radically change the production process.

The proposal being considered as an application of BPR is the adoption of ‘team working’ in the factory, the three main elements of which are as follows:

1. Production lines would re-organise into teams, where all operations on a particular product type are performed in one place by a dedicated team of machinists.

2. Each team of machinists would be responsible for the quality of the finished jacket, and for the first time, machinists would be encouraged to bring about improvements in the production process. There would no longer be the need to employ supervisors and the existing supervisors would join the teams of machinists.

3. The number of batches in production would be automatically tracked by the use of radio frequency identification (RFID) tags attached to each jacket. This would eliminate the need for paper batch cards, which are currently input into a spreadsheet by the supervisors.

You have been asked as a performance management consultant to advise the board on whether business process reengineering could help Cuthbert overcome the problems in its production process.

Required:

(a) Advise how the proposed use of BPR would influence the operational performance of Cuthbert. (14 marks)

(b) Evaluate the effectiveness of the current reward systems at Cuthbert, and recommend and justify how these systems would need to change if the BPR project goes ahead. (11 marks)

第7题

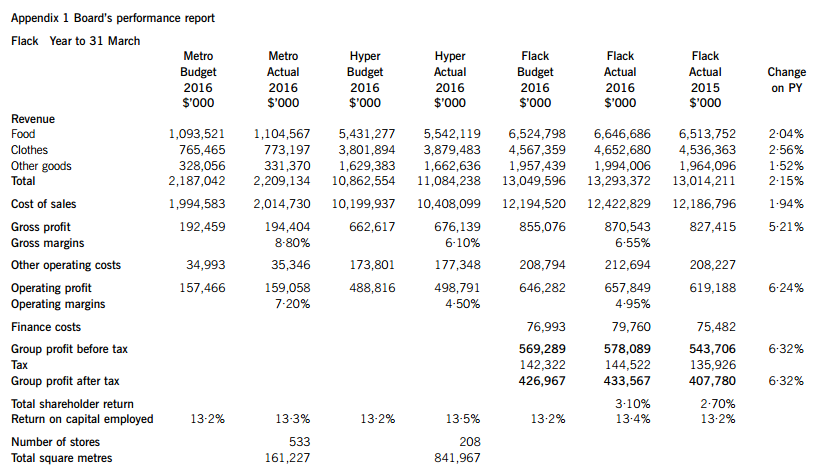

Section A – This ONE question is compulsory and MUST be attempted

Flack Supermarkets (Flack) is a multi-national listed business operating in several developing countries. The business is divided into two divisions: Metro, which runs smaller stores in the densely populated centres of cities and Hyper, which runs the large supermarkets situated on the edges of cities. Flack sells food, clothing and some other household goods.

Competition between supermarkets is intense in all of Flack’s markets and so there is a constant need to review and improve their management and operations. The board has asked for a review of their performance report to see if it is fit for the purpose of achieving the company’s mission of being:

‘…the first choice for customers by providing the right balance of quality and service at a competitive price. We will achieve this through acting in the long-term interests of our stakeholders: earning customer loyalty, utilising all our resources and serving our shareholders’ interests.’

This report is used at Flack’s board level for their annual review. The divisional boards have their own reports. Also, there has been criticism of the board of Flack in the financial press that they are ‘short-termist’ and so the board wants your evaluation of the performance report to include comments on this. A copy of the most recent report is provided as an example at Appendix 1.

The board is considering introducing two new performance measures to address the objective of ‘utilising all our resources’. These are revenue and operating profit per square metre. The CEO also wants an evaluation of these two measures explaining how they might address this aspect of the mission, what those ratios currently are and how they could be used to manage business performance. There is information in Appendix 1 to assist in this work.

There have been disagreements between Flack’s divisional management about capital allocation. The divisions have had capital made available to them. Both sets of divisional managers always seem to want more capital in order to open more stores but historically have been reluctant to invest in refurbishing existing stores. The board is unsure of capital spending priorities given that the press comments about Flack included criticism of the ‘run-down’ look of a number of their stores. The board wants your comments on the effectiveness of the current divisional performance measure of divisional operating profit and the possibility of replacing this with residual income in the light of these problems.

As the company is opening many new stores, the board also wants an assessment of the use of expected return on capital employed (ROCE) as a tool for deciding on new store openings, illustrating this using the data in Appendix 2 on one new store proposal. The focus of comments should be on the use of an expected value not on the use of return on capital employed, as this is widely used and understood in the retail industry.

Finally, the CEO has proposed to the board that a new information system be introduced. She wishes to spend $100m on creating a loyalty card programme with a data warehouse collecting information from customers’ cards regarding their purchases. Her plan is to use this information to target advertising, product range choices and price offers more efficiently than at present.

Required:

Write a report to the board of Flack to:

(i) Evaluate the performance report of Flack, using the example provided in Appendix 1, as requested by the board. (14 marks)

(ii) Evaluate the introduction of the two measures of revenue and operating profit per square metre, as requested by the CEO. (8 marks)

(iii) Assess the proposal to change the divisional performance measure. Note: No calculations of the current values are required. (8 marks)

(iv) Calculate the expected return on capital employed for the new store and assess the use of this tool for decision-making at Flack. (8 marks)

(v) Explain how the proposed new information system can help to improve business performance at Flack. (8 marks)

Professional marks will be awarded for the format, style. and structure of the discussion of your answer. (4 marks)

第8题

market chains in Seeland. The business makes several different flavours of the same basic product. The strategy of the business has been to be a cost leader in order to win the supermarkets’ business. The sales of Godel vary up and down from quarter to quarter depending on the state of the general economy and competitive forces. Most of the sweet manufacturers have been in business for decades and so the business is mature with little scope to be innovative in new product development. The supermarkets prefer to sign suppliers to long-term contracts and so it is difficult for new entrants to gain a foothold in this market. The management style. at Godel is very much command-and-control which fits with the strategy and type of business. Indeed, most employees have been at Godel for many years and have expressed their liking for the straightforward nature of their work.

The chief executive officer (CEO) of Godel has asked your firm of accountants to advise him as his finance director (FD) will be absent for several months due to a recently diagnosed illness. As the CEO is preparing for the next board meeting, he has obtained the operating statement and detailed variance analysis from one of the junior accountants (Appendix 1).

The CEO is happy with the operating statement but wants to understand the detailed operational and planning variances, given in Appendix 1, for the board meeting. He needs to know what action should be taken as a result of these specific variances.

The FD had been looking at the budgeting process before she fell ill. The CEO has decided that you should help him by answering some questions on budgeting at Godel.

Currently, the budget at Godel is set at the start of the year and performance is measured against this. The company uses standard costs for each product and attributes overheads using absorption costing based on machine hours. No variations are allowed to the standard costs during the year. The standard costs and all budget assumptions are discussed with the relevant operational manager before being set. However, these managers grumble that the budget process is very time-consuming and that the results are ultimately of limited value from their perspective. Some of them also complain that they must frequently explain that the variances are not their fault. The CEO wants to know your views on whether this way of budgeting is appropriate and whether the managers’ complaints are justified. He is satisfied that there is no dysfunctional behaviour at Godel which may lead to budget slack or excessive spending and that all managers are working in the best interests of the company.

Finally, in the last few months, the FD had been reading business articles and books and had mentioned that there were a number of organisations which were trying to go beyond budgeting. The CEO is concerned that he does not understand what budgeting does for the business and this is why he wants you to explain what are the benefits and problems of budgeting at Godel before considering replacing it.

Required:

(a) Advise the CEO on the implications for performance management at Godel of analysing variances into the planning and operational elements as shown in Appendix 1. (6 marks)

(b) Evaluate the budgeting system at Godel. (11 marks)

(c) Evaluate the proposal to move to a beyond budgeting method of control at Godel, giving a recommendation on whether to proceed. (8 marks)

第9题

ann) in order to design and manufacture high-performance wind turbines which generate electricity. The joint venture is called TandR with each party owning 50%. Turing will design and build the pylons, housing and turbine blades while Riemann will supply the generators to be fitted inside the housing.

Turing is a medium sized firm known for its blade design skills. It is owned by three venture capital firms (VCs) (each holding 30% of the shares), with the remaining 10% being given to management to motivate them. The VCs each have a large portfolio of business investments and accept that some of these investments may fail provided that some of their investments show large gains. Management is an ambitious group who enjoys the business and technical challenges of introducing new products.

On the other hand, Riemann is a large, family-owned company working in the highly competitive electricity generator sector. The shareholders of Riemann see the business as mature and want it to offer a stable, long-term return on capital. However, recently, Riemann had to seek emergency refinancing (debt and equity) due to its thin profit margins and tough competition, both of which are forecast to continue. As a result, Riemann’s shareholders and management are concerned for the survival of the business and see TandR as a way to generate some additional cash flow. Unlike at Turing, the management of Riemann does not own significant shareholdings in the company which has preferred to pay fixed salaries.

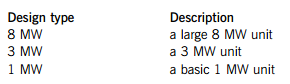

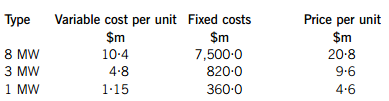

TandR is run by a group of managers made up from each of the JV partners. They are currently faced with a decision about the design of the product. There are three design choices depending on the power which the wind turbines can generate (measured in megawatts [MW]):

The engineering for the 1 MW and 3 MW units is well understood and so design is much simpler than for the 8 MW unit which would be world leading if completed.

The demand for the different types of units will depend on government subsidies of the electricity price charged by the electricity generating companies who will buy the wind turbines and the planning regulations for building such large structures. It is believed that there will be orders for either 1,000 or 1,500 or 2,000 units but there is no clear picture yet of which demand level is more likely than the others.

The estimated costs and prices for the units are:

Notes:

1. The fixed costs cover the initial design, development and testing of the units.

2. The costs and prices are in real terms with the 8 MW unit likely to take two more years to develop than the others.

Required:

(a) Assess the risk appetites of the two firms in the joint venture and provide a justified recommendation for each firm of an appropriate method of decision-making under uncertainty to assess the different types of wind turbines. (9 marks)

(b) Evaluate the choice of turbine design types using your recommended methods from part (a) above. (8 marks)

(c) Discuss the problems encountered in managing performance in a joint venture such as TandR. (8 marks)

第10题

Section B – TWO questions ONLY to be attempted

Booxe is a furniture manufacturing company based in the large, developed country of Teeland. Booxe is the largest furniture manufacturer in Teeland supplying many of the major retail chains with their own-brand furniture and also, making furniture under its own brand (Meson). In a highly competitive market such as Teeland, Booxe has chosen a strategy of cost leadership.

Booxe has been in business for more than 70 years and there is a strong sense of tradition and appreciation of craft skills in the workforce. The average time which an employee has worked for the firm is 18 years. This has led to a bureaucratic culture; for example, the company’s information systems are heavily paper based. In addition and in line with this traditional culture, the organisation is divided into a set of functional departments, such as production, warehousing, human resources and finance.

In order to drive down costs, the chief executive officer (CEO) decided to re-engineer the processes at Booxe. She decided that there should be a small pilot project to demonstrate the potential of business process re-engineering (BPR) to benefit Booxe and she selected the goods receiving activity in the company’s warehousing operations for this.

The CEO has asked you as a performance management expert to complete the post-implementation review of the pilot project by assessing what it has delivered in financial terms. The project identified that 10 of the warehouse staff spend about half of their time matching goods delivered documents to purchase orders and dealing with subsequent problems. It was noted that 25% of all such matches failed and the staff then had to identify the issue and liaise with the purchasing department in order to get the goods returned to the supplier and a suitable credit note issued. The project introduced a new information system to replace the existing paper-based system. The new system allowed purchase orders to be entered by the purchasing department and then checked online to the goods delivered as they arrived at the warehouse. This allowed warehouse staff to reject incorrect deliveries immediately.

The following are further details provided in relation to the project:

Notes relating to old system:

1 Average staff wage in warehouse $25,000 p.a.

2 Purchasing staff time in handling delivery queries 8·5 days per week

3 Average staff wage in purchasing is $32,000 p.a. for working a 5-day week

Notes relating to new system:

New IT system costs:

The CEO now plans to apply BPR across Booxe and as well as completing the post-implementation review, she also needs to know how BPR will change the accounting information systems and the culture at Booxe. Booxe’s current accounting system is a traditional one of overhead absorption based on labour hours with variances to budget used as control indicators. She has heard that an activity-based approach using enterprise resource planning (ERP) systems is fairly common and wants to know how these ideas might link to BPR at Booxe.

The CEO is concerned that middle management unrest may be a problem at Booxe. For example, the warehouse manager was uncomfortable with the cultural change required in the BPR project and decided to take early retirement before the project began. As a result, a temporary manager was put in place to run the warehouse during the project.

The CEO has also begun to reconsider the human resources system at Booxe and she wants your advice on how the staff appraisal process can improve performance in the company. The existing system of manager appraisal is for the staff member to have an annual meeting with their line superior to review the previous year’s work and discuss generally how to improve their efforts. Over the years, it has become common for these meetings to be informal and held over lunch at the company’s expense. The CEO wants to understand the purpose of a staff appraisal system and how the process can improve the performance of the company. She also wants comments on the appropriate balance between control and staff development as this impacts on staff appraisal at Booxe.

Required:

(a) Assess the financial impact of the pilot business process re-engineering (BPR) project in the warehousing operations. (6 marks)

(b) Assess the impact of BPR on the culture and management information systems at Booxe. (11 marks)

(c) Advise on the appraisal process at Booxe as instructed by the CEO. (8 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!