重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

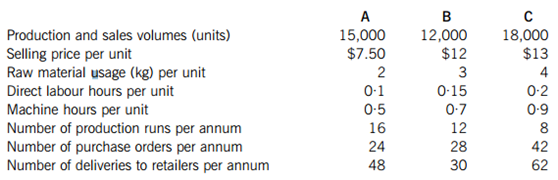

The price for raw materials remained constant throughout the year at $1·20 per kg. Similarly, the direct labour cost for the whole workforce was $14·80 per hour. The annual overhead costs were as follows:

Required:

(a) Calculate the full cost per unit for products A, B and C under traditional absorption costing, using direct labour hours as the basis for apportionment. (5 marks)

(b) Calculate the full cost per unit of each product using activity based costing. (9 marks)

(c) Using your calculation from (a) and (b) above, explain how activity based costing may help The Gadget Co improve the profitability of each product. (6 marks)

更多“The Gadget Co produces three products, A, B and C, all made from the same material. Until”相关的问题

更多“The Gadget Co produces three products, A, B and C, all made from the same material. Until”相关的问题

第1题

s and lotions are sold to a variety of retailers at a price of $23·20 for each jar of face cream and $16·80 for each bottle of body lotion. Each of the products has a variety of ingredients, with the key ones being silk powder, silk amino acids and aloe vera. Six months ago, silk worms were attacked by disease causing a huge reduction in the availability of silk powder and silk amino acids. The Cosmetic Co had to dramatically reduce production and make part of its workforce, which it had trained over a number of years, redundant.

The company now wants to increase production again by ensuring that it uses the limited ingredients available to maximise profits by selling the optimum mix of creams and lotions. Due to the redundancies made earlier in the year, supply of skilled labour is now limited in the short-term to 160 hours (9,600 minutes) per week, although unskilled labour is unlimited. The purchasing manager is confident that they can obtain 5,000 grams of silk powder and 1,600 grams of silk amino acids per week. All other ingredients are unlimited. The following information is available for the two products:

Each jar of cream sold generates a contribution of $9 per unit, whilst each bottle of lotion generates a contribution of $8 per unit. The maximum demand for lotions is 2,000 bottles per week, although demand for creams is unlimited. Fixed costs total $1,800 per week. The company does not keep inventory although if a product is partially complete at the end of one week, its production will be completed in the following week.

Required:

(a) On the graph paper provided, use linear programming to calculate the optimum number of each product that the Cosmetic Co should make per week, assuming that it wishes to maximise contribution. Calculate the total contribution per week for the new production plan. All workings MUST be rounded to 2 decimal places. (14 marks)

(b) Calculate the shadow price for silk powder and the slack for silk amino acids. All workings MUST be rounded to 2 decimal places. (6 marks)

第2题

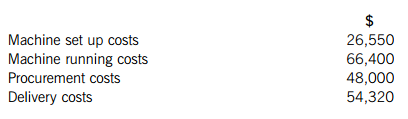

ncy tuition courses in the private sector. It makes up its accounts to 30 November each year. In the year ending 30 November 2009, it held 60% of market share. However, over the last twelve months, the accountancy tuition market in general has faced a 20% decline in demand for accountancy training leading to smaller class sizes on courses. In 2009 and before, AT Co suffered from an ongoing problem with staff retention, which had a knock-on effect on the quality of service provided to students. Following the completion of developments that have been ongoing for some time, in 2010 the company was able to offer a far-improved service to students. The developments included:

– A new dedicated 24 hour student helpline

– An interactive website providing instant support to students

– A new training programme for staff

– An electronic student enrolment system

– An electronic marking system for the marking of students’ progress tests. The costs of marking electronically were expected to be $4 million less in 2010 than marking on paper. Marking expenditure is always included in cost of sales

Extracts from the management accounts for 2009 and 2010 are shown below:

On 1 December 2009, management asked all ‘freelance lecturers’ to reduce their fees by at least 10% with immediate effect (‘freelance lecturers’ are not employees of the company but are used to teach students when there are not enough of AT Co’s own lecturers to meet tuition needs). All employees were also told that they would not receive a pay rise for at least one year. Total lecture staff costs (including freelance lecturers) were $41·663 million in 2009 and were included in cost of sales, as is always the case. Freelance lecturer costs represented 35% of these total lecture staff costs. In 2010 freelance lecture costs were $12·394 million. No reduction was made to course prices in the year and the mix of trainees studying for the different qualifications remained the same. The same type and number of courses were run in both 2009 and 2010 and the percentage of these courses that was run by freelance lecturers as opposed to employed staff also remained the same.

Due to the nature of the business, non-financial performance indicators are also used to assess performance, as detailed below.

Required:

Assess the performance of the business in 2010 using both financial performance indicators calculated from the above information AND the non-financial performance indicators provided.

NOTE: Clearly state any assumptions and show all workings clearly. Your answer should be structured around the following main headings: turnover; cost of sales; gross profit; indirect expenses; net operating profit. However, in discussing each of these areas you should also refer to the non-financial performance indicators, where relevant.

第3题

s and LCD TVs. It operates within a highly competitive market and is constantly under pressure to reduce prices. Carad Co operates a standard costing system and performs a detailed variance analysis of both products on a monthly basis. Extracts from the management information for the month of November are shown below:

Notes

(1) The budgeted total sales volume for TVs was 1,180 units, consisting of an equal mix of plasma screen TVs and LCD screen TVs. Actual sales volume was 750 plasma TVs and 650 LCD TVs. Standard sales prices are $350 per unit for the plasma TVs and $300 per unit for the LCD TVs. The actual sales prices achieved during November were $330 per unit for plasma TVs and $290 per unit for LCD TVs. The standard contributions for plasma TVs and LCD TVs are $190 and $180 per unit respectively.

(2) The sole reason for this variance was an increase in the purchase price of one of its key components, X. Each plasma TV made and each LCD TV made requires one unit of component X, for which Carad Co’s standard cost is $60 per unit. Due to a shortage of components in the market place, the market price for November went up to $85 per unit for X. Carad Co actually paid $80 per unit for it.

(3) Each plasma TV uses 2 standard hours of labour and each LCD TV uses 1·5 standard hours of labour. The standard cost for labour is $14 per hour and this also reflects the actual cost per labour hour for the company’s permanent staff in November. However, because of the increase in sales and production volumes in November, the company also had to use additional temporary labour at the higher cost of $18 per hour. The total capacity of Carad’s permanent workforce is 2,200 hours production per month, assuming full efficiency. In the month of November, the permanent workforce were wholly efficient, taking exactly 2 hours to complete each plasma TV and exactly 1·5 hours to produce each LCD TV. The total labour variance therefore relates solely to the temporary workers, who took twice as long as the permanent workers to complete their production.

Required:

(a) Calculate the following for the month of November, showing all workings clearly:

(i) The sales price variance and sales volume contribution variance; (6 marks)

(ii) The material price planning variance and material price operational variance; (2 marks)

(iii) The labour rate variance and the labour efficiency variance. (7 marks)

(b) Explain the reasons why Carad Co would be interested in the material price planning variance and the material price operational variance. (5 marks)

第4题

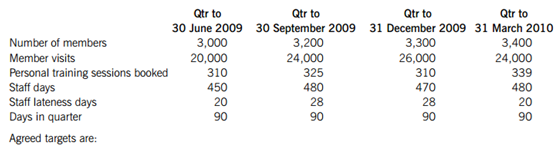

n board. The local managers have a lot of autonomy and are able to vary employment contracts with staff and offer discounts for membership fees and personal training sessions. They also control their own maintenance budget but do not have control over large amounts of capital expenditure.

A local manager’s performance and bonus is assessed relative to three targets. For every one of these three targets that is reached in an individual quarter, $400 is added to the manager’s bonus, which is paid at the end of the year. The maximum bonus per year is therefore based on 12 targets (three targets in each of the four quarters of the year). Accordingly the maximum bonus that could be earned is 12 x $400 = $4,800, which represents 40% of the basic salary of a local manager. Jump has a 31 March year end.

The performance data for one of the sports clubs for the last four quarters is as follows

Agreed targets are:

1. Staff must be on time over 95% of the time (no penalty is made when staff are absent from work)

2. On average 60% of members must use the clubs’ facilities regularly by visiting at least 12 times per quarter

3. On average 10% of members must book a personal training session each quarter

Required:

(a) Calculate the amount of bonus that the manager should expect to be paid for the latest fi nancial year. (6 marks)

(b) Discuss to what extent the targets set are controllable by the local manager (you are required to make a case for both sides of the argument). (9 marks)

(c) Describe two methods as to how a manager with access to the accounting and other records could unethically manipulate the situation so as to gain a greater bonus. (5 marks)

第5题

f the products it sells are bought in from outside suppliers but some are currently manufactured by Hammer’s own manufacturing division ‘Nail’.

The prices (a transfer price) that Nail charges to the retail stores are set by head offi ce and have been the subject of some discussion. The current policy is for Nail to calculate the total variable cost of production and delivery and add 30% for profi t. Nail argues that all costs should be taken into consideration, offering to reduce the mark-up on costs to 10% in this case. The retail stores are unhappy with the current pricing policy arguing that it results in prices that are often higher than comparable products available on the market.

Nail has provided the following information to enable a price comparison to be made of the two possible pricing policies for one of its products.

Garden shears

Steel: the shears have 0?4kg of high quality steel in the fi nal product. The manufacturing process loses 5% of all steel put in. Steel costs $4,000 per tonne (1 tonne = 1,000kg)

Other materials: Other materials are bought in and have a list price of $3 per kg although Hammer secures a 10% volume discount on all purchases. The shears require 0?1kg of these materials.

The labour time to produce shears is 0?25 hours per unit and labour costs $10 per hour.

Variable overheads are absorbed at the rate of 150% of labour rates and fi xed overheads are 80% of the variable overheads.

Delivery is made by an outsourced distributor that charges Nail $0?50 per garden shear for delivery.

Required:

(a) Calculate the price that Nail would charge for the garden shears under the existing policy of variable cost plus 30%. (6 marks)

(b) Calculate the increase or decrease in price if the pricing policy switched to total cost plus 10%. (4 marks)

(c) Discuss whether or not including fi xed costs in a transfer price is a sensible policy. (4 marks)

(d) Discuss whether the retail stores should be allowed to buy in from outside suppliers if the prices are cheaper than those charged by Nail. (6 marks)

第6题

and unique fabric (material). Both the tailors and the fabric are in short supply and so the accountant at CS has correctly produced a linear programming model to help decide the optimal production mix.

The model is as follows:

Variables: Let W = the number of work suits produced

Let L = the number of lounge suits produced

Constraints Tailors’ time: 7W + 5L ≤ 3,500 (hours) – this is line T on the diagram

Fabric: 2W + 2L ≤ 1,200 (metres) – this is line F on the diagram

Production of work suits: W ≤ 400 – this is line P on the diagram

Objective is to maximise contribution subject to:

C = 48W + 40L

On the diagram provided the accountant has correctly identifi ed OABCD as the feasible region and point B as the optimal point.

Required:

(a) Find by appropriate calculation the optimal production mix and related maximum contribution that could be earned by CS. (4 marks)

(b) Calculate the shadow prices of the fabric per metre and the tailor time per hour. (6 marks)

The tailors have offered to work an extra 500 hours provided that they are paid three times their normal rate of $1?50 per hour at $4?50 per hour.

Required:

(c) Briefl y discuss whether CS should accept the offer of overtime at three times the normal rate. (6 marks)

(d) Calculate the new optimum production plan if maximum demand for W falls to 200 units. (4 marks)

第7题

ing mainly traditional manual techniques. The manufacturing department is a cost centre within the business and operates a standard costing system based on marginal costs.

At the beginning of April 2010 the production director attempted to reduce the cost of the bats by sourcing wood from a new supplier and de-skilling the process a little by using lower grade staff on parts of the production process. The standards were not adjusted to refl ect these changes.

The variance report for April 2010 is shown below (extract).

The production director pointed out in his April 2010 board report that the new grade of labour required signifi cant training in April and this meant that productive time was lower than usual. He accepted that the workers were a little slow at the moment but expected that an improvement would be seen in May 2010. He also mentioned that the new wood being used was proving diffi cult to cut cleanly resulting in increased waste levels.

Sales for April 2010 were down 10% on budget and returns of faulty bats were up 20% on the previous month. The sales director resigned after the board meeting stating that SW had always produced quality products but the new strategy was bound to upset customers and damage the brand of the business.

Required

(a) Assess the performance of the production director using all the information above taking into account both the decision to use a new supplier and the decision to de-skill the process. (7 marks)

In May 2010 the budgeted sales were 19,000 bats and the standard cost card is as follows:

In May 2010 the following results were achieved:

40,000kg of wood were bought at a cost of $196,000, this produced 19,200 cricket bats. No inventory of raw materials is held. The labour was paid for 62,000 hours and the total cost was $694,000. Labour worked for 61,500 hours.

The sales price was reduced to protect the sales levels. However, only 18,000 cricket bats were sold at an average price of $65.

Required:

(b) Calculate the materials, labour and sales variances for May 2010 in as much detail as the information allows. You are not required to comment on the performance of the business. (13 marks)

第8题

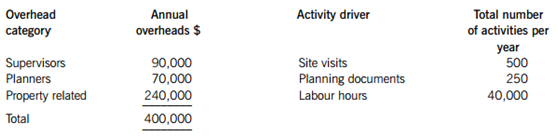

the public. Recently they have been asked to quote for garage conversions (GC) and extensions to properties (EX) and have found that they are winning fewer GC contracts than expected.

BBB has a policy to price all jobs at budgeted total cost plus 50%. Overheads are currently absorbed on a labour hour basis. BBB thinks that a switch to activity based costing (ABC) to absorb overheads would reduce the cost associated to GC and hence make them more competitive.

You are provided with the following data:

A typical GC costs $3,500 in materials and takes 300 labour hours to complete. A GC requires only one site visit by a supervisor and needs only one planning document to be raised. The typical EX costs $8,000 in materials and takes 500 hours to complete. An EX requires six site visits and fi ve planning documents. In all cases labour is paid $15 per hour.

Required:

(a) Calculate the cost and quoted price of a GC and of an EX using labour hours to absorb the overheads. (5 marks)

(b) Calculate the cost and the quoted price of a GC and of an EX using ABC to absorb the overheads. (5 marks)

(c) Assuming that the cost of a GC falls by nearly 7% and the price of an EX rises by about 2% as a result of the change to ABC, suggest possible pricing strategies for the two products that BBB sells and suggest two reasons other than high prices for the current poor sales of the GC. (6 marks)

(d) One BBB manager has suggested that only marginal cost should be included in budget cost calculations as this would avoid the need for arbitrary overhead allocations to products. Briefl y discuss this point of view and comment on the implication for the amount of mark-up that would be applied to budget costs when producing quotes for jobs. (4 marks)

第9题

ir. The standard cost of labour for each pair is $42 and the standard labour time for each pair is three hours. In the last quarter, Glove Co had budgeted production of 12,000 pairs, although actual production was 12,600 pairs in order to meet demand.

37,000 hours were used to complete the work and there was no idle time. The total labour cost for the quarter was $531,930.

At the beginning of the last quarter, the design of the gloves was changed slightly. The new design required workers to sew the company’s logo on to the back of every glove made and the estimated time to do this was 15 minutes for each pair. However, no-one told the accountant responsible for updating standard costs that the standard time per pair of gloves needed to be changed. Similarly, although all workers were given a 2% pay rise at the beginning of the last quarter, the accountant was not told about this either. Consequently, the standard was not updated to reflect these changes.

When overtime is required, workers are paid 25% more than their usual hourly rate.

Required:

(a) Calculate the total labour rate and total labour efficiency variances for the last quarter. (2 marks)

(b) Analyse the above total variances into component parts for planning and operational variances in as much detail as the information allows. (6 marks)

(c) Assess the performance of the production manager for the last quarter. (7 marks)

第10题

ons make a single standardised product. Division L makes component L, which is supplied to both Division M and external customers.

Division M makes product M using one unit of component L and other materials. It then sells the completed

product M to external customers. To date, Division M has always bought component L from Division L.

The following information is available:

Division L charges the same price for component L to both Division M and external customers. However, it does not incur the selling and distribution costs when transferring internally.

Division M has just been approached by a new supplier who has offered to supply it with component L for $37 per unit. Prior to this offer, the cheapest price which Division M could have bought component L for from outside the group was $42 per unit.

It is head office policy to let the divisions operate autonomously without interference at all.

Required:

(a) Calculate the incremental profit/(loss) per component for the group if Division M accepts the new supplier’s

offer and recommend how many components Division L should sell to Division M if group profits are to be

maximised. (3 marks)

(b) Using the quantities calculated in (a) and the current transfer price, calculate the total annual profits of each division and the group as a whole. (6 marks)

(c) Discuss the problems which will arise if the transfer price remains unchanged and advise the divisions on a suitable alternative transfer price for component L. (6 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!