重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

(a) An important aspect of the International Accounting Standards Board’s Framework for the preparation and presentation of fi nancial statements is that transactions should be recorded on the basis of their substance over their form.

Required:

Explain why it is important that fi nancial statements should refl ect the substance of the underlying transactions and describe the features that may indicate that the substance of a transaction may be different from its legal form. (5 marks)

(b) Wardle’s activities include the production of maturing products which take a long time before they are ready to retail. Details of one such product are that on 1 April 2009 it had a cost of $5 million and a fair value of $7 million. The product would not be ready for retail sale until 31 March 2012.

On 1 April 2009 Wardle entered into an agreement to sell the product to Easyfi nance for $6 million. The agreement gave Wardle the right to repurchase the product at any time up to 31 March 2012 at a fi xed price of $7,986,000, at which date Wardle expected the product to retail for $10 million. The compound interest Wardle would have to pay on a three-year loan of $6 million would be:

This interest is equivalent to the return required by Easyfi nance.

Required:

Assuming the above fi gures prove to be accurate, prepare extracts from the income statement of Wardle for the three years to 31 March 2012 in respect of the above transaction:

(i) Refl ecting the legal form. of the transaction;

(ii) Refl ecting the substance of the transaction.

Note: statement of fi nancial position extracts are NOT required.

The following mark allocation is provided as guidance for this requirement:

(i) 2 marks

(ii) 3 marks (5 marks)

(c) Comment on the effect the two treatments have on the income statements and the statements of fi nancial position and how this may affect an assessment of Wardle’s performance. (5 marks)

更多“(a) An important aspect of the International Accounting Standards Board’s Framework for th”相关的问题

更多“(a) An important aspect of the International Accounting Standards Board’s Framework for th”相关的问题

第1题

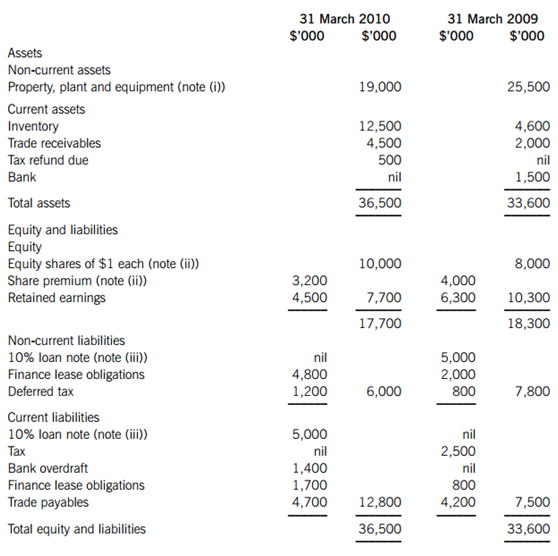

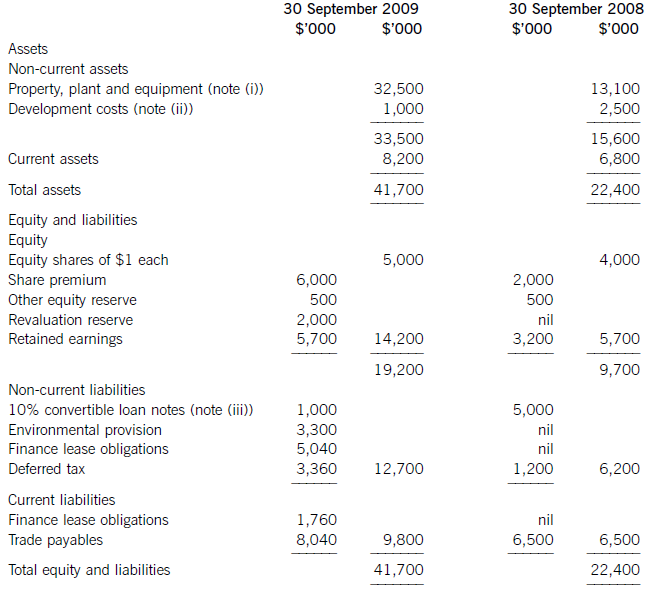

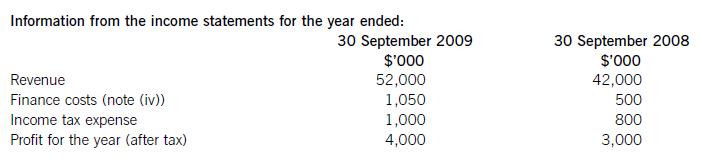

(a) The following information relates to the draft fi nancial statements of Deltoid.

Summarised statements of fi nancial position as at:

Summarised income statements for the years ended:

The following additional information is available:

(i) Property, plant and equipment is made up of:

(ii) On 1 July 2009 there was a bonus issue of shares from share premium of one new share for every 10 held.

On 1 October 2009 there was a fully subscribed cash issue of shares at par.

(iii) The 10% loan note is due for repayment on 30 June 2010. Deltoid is in negotiations with the loan provider to refi nance the same amount for another fi ve years.

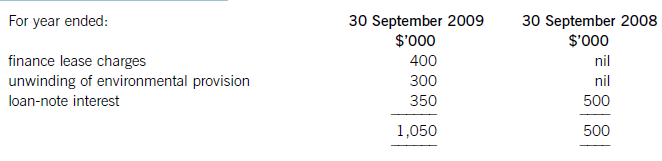

(iv) The fi nance costs are made up of:

For year ended:

Required:

(i) Prepare a statement of cash fl ows for Deltoid for the year ended 31 March 2010 in accordance with IAS 7 Statement of cash fl ows, using the indirect method; (12 marks)

(ii) Based on the information available, advise the loan provider on the matters you would take into consideration when deciding whether to grant Deltoid a renewal of its maturing loan note. (8 marks)

(b) On a separate matter, you have been asked to advise on an application for a loan to build an extension to a sports club which is a not-for-profi t organisation. You have been provided with the audited fi nancial statements of the sports club for the last four years.

Required:

Identify and explain the ratios that you would calculate to assist in determining whether you would advise that the loan should be granted. (5 marks)

第2题

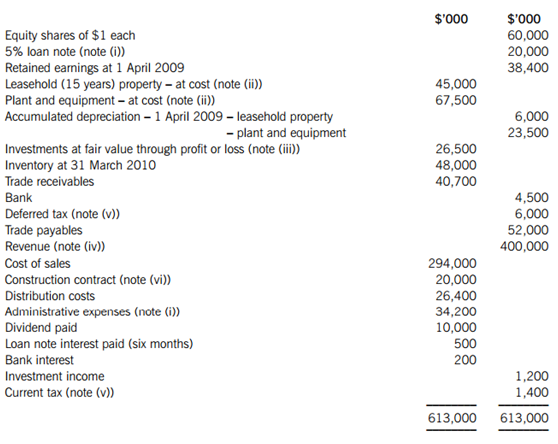

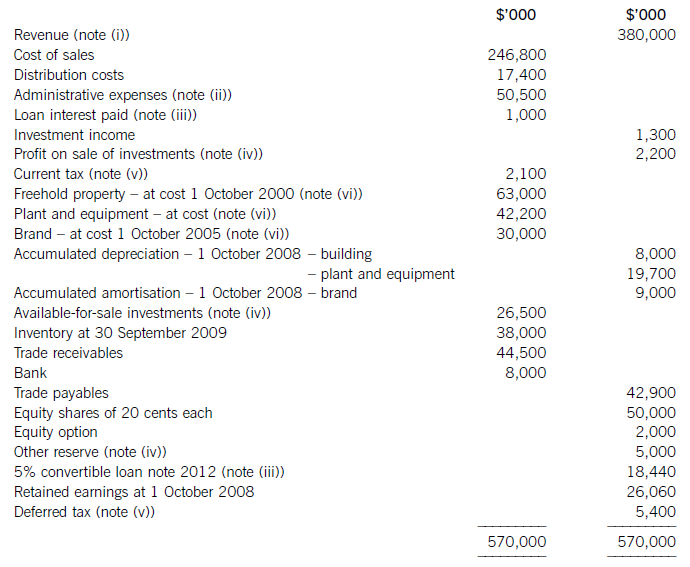

The following trial balance relates to Dune at 31 March 2010:

The following notes are relevant:

(i) The 5% loan note was issued on 1 April 2009 at its nominal (face) value of $20 million. The direct costs of the issue were $500,000 and these have been charged to administrative expenses. The loan note will be redeemed on 31 March 2012 at a substantial premium. The effective fi nance cost of the loan note is 10% per annum.

(ii) Non-current assets:

In order to fund a new project, on 1 October 2009 the company decided to sell its leasehold property. From that date it commenced a short-term rental of an equivalent property. The leasehold property is being marketed by a property agent at a price of $40 million, which was considered a reasonably achievable price at that date. The expected costs to sell have been agreed at $500,000. Recent market transactions suggest that actual selling prices achieved for this type of property in the current market conditions are 15% less than the value at which they are marketed. At 31 March 2010 the property had not been sold.

Plant and equipment is depreciated at 15% per annum using the reducing balance method.

No depreciation/amortisation has yet been charged on any non-current asset for the year ended 31 March 2010. Depreciation, amortisation and impairment charges are all charged to cost of sales.

(iii) The investments at fair value through profi t or loss had a fair value of $28 million on 31 March 2010. There were no purchases or disposals of any of these investments during the year.

(iv) It has been discovered that goods with a cost of $6 million, which had been correctly included in the count of the inventory at 31 March 2010, had been invoiced in April 2010 to customers at a gross profi t of 25% on sales, but included in the revenue (and receivables) of the year ended 31 March 2010.

(v) A provision for income tax for the year ended 31 March 2010 of $12 million is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 31 March 2009. At 31 March 2010 the tax base of Dune’s net assets was $14 million less than their carrying amounts. The income tax rate of Dune is 30%.

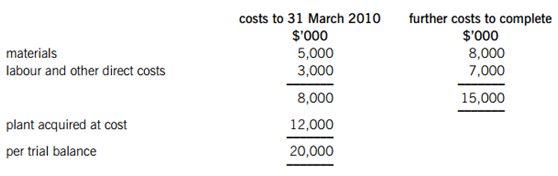

(vi) The details of the construction contract are:

The contract commenced on 1 October 2009 and is scheduled to take 18 months to complete. The agreed contract price is fi xed at $40 million. Specialised plant was purchased at the start of the contract for $12 million. It is expected to have a residual value of $3 million at the end of the contract and should be depreciated using the straight-line method on a monthly basis. An independent surveyor has assessed that the contract is 30% complete at 31 March 2010. The customer has not been invoiced for any progress payments. The outcome of the contract is deemed to be reasonably certain as at the year end.

Required:

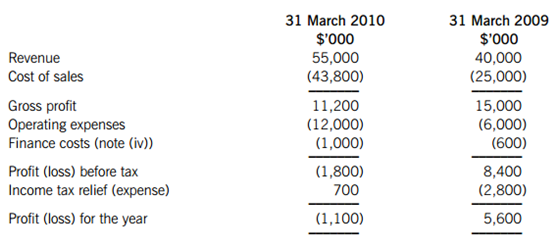

(a) Prepare the income statement for Dune for the year ended 31 March 2010.

(b) Prepare the statement of fi nancial position for Dune as at 31 March 2010.

Notes to the fi nancial statements are not required.

A statement of changes in equity is not required.

The following mark allocation is provided as guidance for this question:

(a) 13 marks

(b) 12 marks

第3题

shares in Picant for every two shares in Sander. The market prices of Picant’s and Sander’s shares at the date of acquisition were $3·20 and $4·50 respectively.

In addition to this Picant agreed to pay a further amount on 1 April 2010 that was contingent upon the post-acquisition performance of Sander. At the date of acquisition Picant assessed the fair value of this contingent consideration at $4·2 million, but by 31 March 2010 it was clear that the actual amount to be paid would be only $2·7 million (ignore discounting). Picant has recorded the share exchange and provided for the initial estimate of $4·2 million for the contingent consideration.

On 1 October 2009 Picant also acquired 40% of the equity shares of Adler paying $4 in cash per acquired share and issuing at par one $100 7% loan note for every 50 shares acquired in Adler. This consideration has also been recorded by Picant.

Picant has no other investments.

The summarised statements of fi nancial position of the three companies at 31 March 2010 are:

(i) At the date of acquisition the fair values of Sander’s property, plant and equipment was equal to its carrying amount with the exception of Sander’s factory which had a fair value of $2 million above its carrying amount. Sander has not adjusted the carrying amount of the factory as a result of the fair value exercise. This requires additional annual depreciation of $100,000 in the consolidated fi nancial statements in the post-acquisition period.

Also at the date of acquisition, Sander had an intangible asset of $500,000 for software in its statement of fi nancial position. Picant’s directors believed the software to have no recoverable value at the date of acquisition and Sander wrote it off shortly after its acquisition.

(ii) At 31 March 2010 Picant’s current account with Sander was $3·4 million (debit). This did not agree with the equivalent balance in Sander’s books due to some goods-in-transit invoiced at $1·8 million that were sent by Picant on 28 March 2010, but had not been received by Sander until after the year end. Picant sold all these goods at cost plus 50%.

(iii) Picant’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose Sander’s share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest.

(iv) Impairment tests were carried out on 31 March 2010 which concluded that the value of the investment in Adler was not impaired but, due to poor trading performance, consolidated goodwill was impaired by $3·8 million.

The following information is relevant:

(v) Assume all profi ts accrue evenly through the year.

Required:

(a) Prepare the consolidated statement of fi nancial position for Picant as at 31 March 2010. (21 marks)

(b) Picant has been approached by a potential new customer, Trilby, to supply it with a substantial quantity of goods on three months credit terms. Picant is concerned at the risk that such a large order represents in the current diffi cult economic climate, especially as Picant’s normal credit terms are only one month’s credit. To support its application for credit, Trilby has sent Picant a copy of Tradhat’s most recent audited consolidated fi nancial statements. Trilby is a wholly-owned subsidiary within the Tradhat group. Tradhat’s consolidated fi nancial statements show a strong statement of fi nancial position including healthy liquidity ratios.

Required:

Comment on the importance that Picant should attach to Tradhat’s consolidated fi nancial statements when deciding on whether to grant credit terms to Trilby. (4 marks)

第4题

mparatives) of Barstead for

the year ended 30 September 2009:

increase in profit after taxation 80%

increase in (basic) earnings per share 5%

increase in diluted earnings per share 2%

Required:

Explain why the three measures of earnings (profit) growth for the same company over the same period can

give apparently differing impressions. (4 marks)

(b) The profit after tax for Barstead for the year ended 30 September 2009 was $15 million. At 1 October 2008 the company had in issue 36 million equity shares and a $10 million 8% convertible loan note. The loan note will mature in 2010 and will be redeemed at par or converted to equity shares on the basis of 25 shares for each $100 of loan note at the loan-note holders’ option. On 1 January 2009 Barstead made a fully subscribed rights issue of one new share for every four shares held at a price of $2·80 each. The market price of the equity shares of Barstead immediately before the issue was $3·80. The earnings per share (EPS) reported for the year ended 30 September 2008 was 35 cents.

Barstead’s income tax rate is 25%.

Required:

Calculate the (basic) EPS figure for Barstead (including comparatives) and the diluted EPS (comparatives not required) that would be disclosed for the year ended 30 September 2009. (6 marks)

第5题

ed for his study course for giving the definition of a non-current asset as ‘a physical asset of substantial cost, owned by the company, which will last longer than one year’.

Required:

Provide an explanation to your assistant of the weaknesses in his definition of non-current assets when

compared to the International Accounting Standards Board’s (IASB) view of assets. (4 marks)

(b) The same assistant has encountered the following matters during the preparation of the draft financial statements of Darby for the year ending 30 September 2009. He has given an explanation of his treatment of them.

(i) Darby spent $200,000 sending its staff on training courses during the year. This has already led to an

improvement in the company’s efficiency and resulted in cost savings. The organiser of the course has stated that the benefits from the training should last for a minimum of four years. The assistant has therefore treated the cost of the training as an intangible asset and charged six months’ amortisation based on the average date during the year on which the training courses were completed. (3 marks)

(ii) During the year the company started research work with a view to the eventual development of a new

processor chip. By 30 September 2009 it had spent $1·6 million on this project. Darby has a past history

of being particularly successful in bringing similar projects to a profitable conclusion. As a consequence the

assistant has treated the expenditure to date on this project as an asset in the statement of financial position.

Darby was also commissioned by a customer to research and, if feasible, produce a computer system to

install in motor vehicles that can automatically stop the vehicle if it is about to be involved in a collision. At

30 September 2009, Darby had spent $2·4 million on this project, but at this date it was uncertain as to

whether the project would be successful. As a consequence the assistant has treated the $2·4 million as an

expense in the income statement. (4 marks)

(iii) Darby signed a contract (for an initial three years) in August 2009 with a company called Media Today to

install a satellite dish and cabling system to a newly built group of residential apartments. Media Today will

provide telephone and television services to the residents of the apartments via the satellite system and pay

Darby $50,000 per annum commencing in December 2009. Work on the installation commenced on

1 September 2009 and the expenditure to 30 September 2009 was $58,000. The installation is expected

to be completed by 31 October 2009. Previous experience with similar contracts indicates that Darby will

make a total profit of $40,000 over the three years on this initial contract. The assistant correctly recorded

the costs to 30 September 2009 of $58,000 as a non-current asset, but then wrote this amount down to

$40,000 (the expected total profit) because he believed the asset to be impaired.

The contract is not a finance lease. Ignore discounting. (4 marks)

Required:

For each of the above items (i) to (iii) comment on the assistant’s treatment of them in the financial

statements for the year ended 30 September 2009 and advise him how they should be treated under

International Financial Reporting Standards.

Note: the mark allocation is shown against each of the three items above.

第6题

(a) The following information relates to Crosswire a publicly listed company.

Summarised statements of financial position as at:

The following information is available:

(i) During the year to 30 September 2009, Crosswire embarked on a replacement and expansion programme for its non-current assets. The details of this programme are:

On 1 October 2008 Crosswire acquired a platinum mine at a cost of $5 million. A condition of mining the

platinum is a requirement to landscape the mining site at the end of its estimated life of ten years. The

present value of this cost at the date of the purchase was calculated at $3 million (in addition to the

purchase price of the mine of $5 million).

Also on 1 October 2008 Crosswire revalued its freehold land for the first time. The credit in the revaluation

reserve is the net amount of the revaluation after a transfer to deferred tax on the gain. The tax rate applicable to Crosswire for deferred tax is 20% per annum.

On 1 April 2009 Crosswire took out a finance lease for some new plant. The fair value of the plant was

$10 million. The lease agreement provided for an initial payment on 1 April 2009 of $2·4 million followed

by eight six-monthly payments of $1·2 million commencing 30 September 2009.

Plant disposed of during the year had a carrying amount of $500,000 and was sold for $1·2 million. The

remaining movement on the property, plant and equipment, after charging depreciation of $3 million, was

the cost of replacing plant.

(ii) From 1 October 2008 to 31 March 2009 a further $500,000 was spent completing the development

project at which date marketing and production started. The sales of the new product proved disappointing

and on 30 September 2009 the development costs were written down to $1 million via an impairment

charge.

(iii) During the year ended 30 September 2009, $4 million of the 10% convertible loan notes matured. The

loan note holders had the option of redemption at par in cash or to exchange them for equity shares on the

basis of 20 new shares for each $100 of loan notes. 75% of the loan-note holders chose the equity option.

Ignore any effect of this on the other equity reserve.

All the above items have been treated correctly according to International Financial Reporting Standards.

(iv) The finance costs are made up of:

Required:

(i) Prepare a statement of the movements in the carrying amount of Crosswire’s non-current assets for the

year ended 30 September 2009; (9 marks)

(ii) Calculate the amounts that would appear under the headings of ‘cash flows from investing activities’

and ‘cash flows from financing activities’ in the statement of cash flows for Crosswire for the year ended

30 September 2009.

Note: Crosswire includes finance costs paid as a financing activity. (8 marks)

(b) A substantial shareholder has written to the directors of Crosswire expressing particular concern over the

deterioration of the company’s return on capital employed (ROCE)

Required:

Calculate Crosswire’s ROCE for the two years ended 30 September 2008 and 2009 and comment on the

apparent cause of its deterioration.

Note: ROCE should be taken as profit before interest on long-term borrowings and tax as a percentage of equity plus loan notes and finance lease obligations (at the year end). (8 marks)

第7题

The following trial balance relates to Sandown at 30 September 2009:

The following notes are relevant:

(i) Sandown’s revenue includes $16 million for goods sold to Pending on 1 October 2008. The terms of the sale are that Sandown will incur ongoing service and support costs of $1·2 million per annum for three years after the sale. Sandown normally makes a gross profit of 40% on such servicing and support work. Ignore the time value of money.

(ii) Administrative expenses include an equity dividend of 4·8 cents per share paid during the year.

(iii) The 5% convertible loan note was issued for proceeds of $20 million on 1 October 2007. It has an effective interest rate of 8% due to the value of its conversion option.

(iv) During the year Sandown sold an available-for-sale investment for $11 million. At the date of sale it had a

carrying amount of $8·8 million and had originally cost $7 million. Sandown has recorded the disposal of the

investment. The remaining available-for-sale investments (the $26·5 million in the trial balance) have a fair value of $29 million at 30 September 2009. The other reserve in the trial balance represents the net increase in the value of the available-for-sale investments as at 1 October 2008. Ignore deferred tax on these transactions.

(v) The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2008. The directors have estimated the provision for income tax for the year ended 30 September 2009 at $16·2 million. At 30 September 2009 the carrying amounts of Sandown’s net assets were $13 million in excess of their tax base. The income tax rate of Sandown is 30%.

(vi) Non-current assets:

The freehold property has a land element of $13 million. The building element is being depreciated on a

straight-line basis.

Plant and equipment is depreciated at 40% per annum using the reducing balance method.

Sandown’s brand in the trial balance relates to a product line that received bad publicity during the year which led to falling sales revenues. An impairment review was conducted on 1 April 2009 which concluded that, based on estimated future sales, the brand had a value in use of $12 million and a remaining life of only three years.

However, on the same date as the impairment review, Sandown received an offer to purchase the brand for

$15 million. Prior to the impairment review, it was being depreciated using the straight-line method over a

10-year life.

No depreciation/amortisation has yet been charged on any non-current asset for the year ended 30 September

2009. Depreciation, amortisation and impairment charges are all charged to cost of sales.

Required:

(a) Prepare the statement of comprehensive income for Sandown for the year ended 30 September 2009.

(13 marks)

(b) Prepare the statement of financial position of Sandown as at 30 September 2009. (12 marks)

Notes to the financial statements are not required.

A statement of changes in equity is not required.

第8题

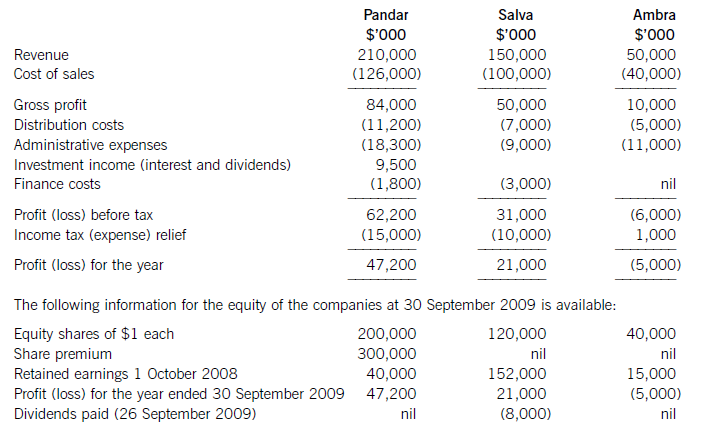

rough a share exchange of three shares in Pandar for every five shares in Salva. The market prices of Pandar’s and Salva’s shares at 1 April

2009 were $6 per share and $3.20 respectively.

On the same date Pandar acquired 40% of the equity shares in Ambra paying $2 per share.

The summarised income statements for the three companies for the year ended 30 September 2009 are:

The following information is relevant:

(i) The fair values of the net assets of Salva at the date of acquisition were equal to their carrying amounts with the exception of an item of plant which had a carrying amount of $12 million and a fair value of $17 million. This plant had a remaining life of five years (straight-line depreciation) at the date of acquisition of Salva. All depreciation is charged to cost of sales.

In addition Salva owns the registration of a popular internet domain name. The registration, which had a

negligible cost, has a five year remaining life (at the date of acquisition); however, it is renewable indefinitely at a nominal cost. At the date of acquisition the domain name was valued by a specialist company at $20 million.

The fair values of the plant and the domain name have not been reflected in Salva’s financial statements.

No fair value adjustments were required on the acquisition of the investment in Ambra.

(ii) Immediately after its acquisition of Salva, Pandar invested $50 million in an 8% loan note from Salva. All interest accruing to 30 September 2009 had been accounted for by both companies. Salva also has other loans in issue at 30 September 2009.

(iii) Pandar has credited the whole of the dividend it received from Salva to investment income.

(iv) After the acquisition, Pandar sold goods to Salva for $15 million on which Pandar made a gross profit of 20%. Salva had one third of these goods still in its inventory at 30 September 2009. There are no intra-group current account balances at 30 September 2009.

(v) The non-controlling interest in Salva is to be valued at its (full) fair value at the date of acquisition. For this

purpose Salva’s share price at that date can be taken to be indicative of the fair value of the shareholding of the non-controlling interest.

(vi) The goodwill of Salva has not suffered any impairment; however, due to its losses, the value of Pandar’s

investment in Ambra has been impaired by $3 million at 30 September 2009.

(vii) All items in the above income statements are deemed to accrue evenly over the year unless otherwise indicated.

Required:

(a) (i) Calculate the goodwill arising on the acquisition of Salva at 1 April 2009; (6 marks)

(ii) Calculate the carrying amount of the investment in Ambra to be included within the consolidated

statement of financial position as at 30 September 2009. (3 marks)

(b) Prepare the consolidated income statement for the Pandar Group for the year ended 30 September 2009.(16 marks)

第9题

【题目描述】

【我提交的答案】:

【参考答案分析】:

为什么increase in insurance claim provision 是减少现金流 ,出现(300),不应该是增加吗?实在很疑惑

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!