重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

(c) Misson has further entered into a contract to purchase plant and equipment from a foreign supplier on 30 June

2007. The purchase price is 4 million euros. A non-refundable deposit of 1 million euros was paid on signing

the contract on 31 July 2006 with the balance of 3 million euros payable on 30 June 2007. Misson was

uncertain as to whether to purchase a 3 million euro bond on 31 July 2006 which will not mature until 30 June

2010, or to enter into a forward contract on the same date to purchase 3 million euros for a fixed price of

$2 million on 30 June 2007 and to designate the forward contract as a cash flow hedge of the purchase

commitment. The bond carries interest at 4% per annum payable on 30 June 2007. Current market rates are

4% per annum. The company chose to purchase the bond with a view to selling it on 30 June 2007 in order

to purchase the plant and equipment. The bond is not to be classified as a cash flow hedge but at fair value

through profit or loss.

Misson would like advice as to whether it made the correct decision and as to the accounting treatment of the

items in (c) above for the current and subsequent year. (10 marks)

更多“(c) Misson has further entered into a contract to purchase plant and equipment from a fore”相关的问题

更多“(c) Misson has further entered into a contract to purchase plant and equipment from a fore”相关的问题

第1题

ds (IFRS) in its financial

statements for the year ended 31 May 2005. The directors of the company are worried about the effect of the move

to IFRS on their financial performance and the views of analysts. The directors have highlighted some ‘headline’

differences between IFRS and their current local equivalent standards and require a report on the impact of a move

to IFRS on the key financial ratios for the current period.

Differences between local Generally Accepted Accounting Practice (GAAP) and IFRS

Leases

Local GAAP does not require property leases to be separated into land and building components. Long-term property

leases are accounted for as operating leases in the financial statements of Handrew under local GAAP. Under the terms

of the contract, the title to the land does not pass to Handrew but the title to the building passes to the company.

The company has produced a schedule of future minimum operating lease rentals and allocated these rentals between

land and buildings based on their relative fair value at the start of the lease period. The operating leases commenced

on 1 June 2004 when the value of the land was $270 million and the building was $90 million. Annual operating

lease rentals paid in arrears commencing on 31 May 2005 are land $30 million and buildings $10 million. These

amounts are payable for the first five years of the lease term after which the payments diminish. The minimum lease

term is 40 years.

The net present value of the future minimum operating lease payments as at 1 June 2004 was land $198 million

and buildings $86 million. The interest rate used for discounting cash flows is 6%. Buildings are depreciated on a

straight line basis over 20 years and at the end of this period, the building’s economic life will be over. The lessee

intends to redevelop the land at some stage in the future. Assume that the tax allowances on buildings are given to

the lessee on the same basis as the depreciation charge based on the net present value at the start of the lease, and

that operating lease payments are fully allowable for taxation.

Plant and equipment

Local GAAP requires the residual value of a non-current asset to be determined at the date of acquisition or latest

valuation. The residual value of much of the plant and equipment is deemed to be negligible. However, certain plant

(cost $20 million and carrying value $16 million at 31 May 2005) has a high residual value. At the time of

purchasing this plant (June 2003), the residual value was thought to be approximately $4 million. However the value

of an item of an identical piece of plant already of the age and in the condition expected at the end of its useful life

is $8 million at 31 May 2005 ($11 million at 1 June 2004). Plant is depreciated on a straight line basis over

eight years.

Investment properties

Local GAAP requires investment property to be measured at market value and gains and losses reported in equity.

The company owns a hotel which consists of land and buildings and it has been designated as an investment

property. The property was purchased on 1 June 2004. The hotel has been included in the balance sheet at 31 May

2005 at its market value on an existing use basis at $40 million (land valuation $30 million, building $10 million).

A revaluation gain of $5 million has been recognised in equity. The company could sell the land for redevelopment

for $50 million although it has no intention of doing so at the present time. The company wants to recognise holding

gains/losses in profit and loss. Local GAAP does not require deferred tax to be provided on revaluation gains and

losses.

The directors have calculated the following ratios based on the local GAAP financial statements for the year ended

The issued share capital of Handrew is 200 million ordinary shares of $1. There is no preference capital. The interest

charge and tax charge in the income statement are $5 million and $25 million respectively. Interest and rental

payments attract tax allowances in this jurisdiction when paid. Assume taxation is 30%.

Required:

Write a report to the directors of Handrew:

(a) Discussing the impact of the change to IFRS on the reported profit and balance sheet of Handrew at 31 May

2005. (18 marks)

(b) Calculate and briefly discuss the impact of the change to IFRS on the three performance ratios. (7 marks)

(Candidates should show in an appendix calculations of the impact of the move to IFRS on profits, taxation and

the balance sheet. Candidates should not take into account IFRS1 ‘First time Adoption of International Financial

Reporting Standards’ when answering this question.)

(25 marks)

第2题

year end of 31 May 2006.

The company sells its products in department stores throughout the world. Prochain insists on creating its own selling

areas within the department stores which are called ‘model areas’. Prochain is allocated space in the department store

where it can display and market its fashion goods. The company feels that this helps to promote its merchandise.

Prochain pays for all the costs of the ‘model areas’ including design, decoration and construction costs. The areas are

used for approximately two years after which the company has to dismantle the ‘model areas’. The costs of

dismantling the ‘model areas’ are normally 20% of the original construction cost and the elements of the area are

worthless when dismantled. The current accounting practice followed by Prochain is to charge the full cost of the

‘model areas’ against profit or loss in the year when the area is dismantled. The accumulated cost of the ‘model areas’

shown in the balance sheet at 31 May 2006 is $20 million. The company has estimated that the average age of the

‘model areas’ is eight months at 31 May 2006. (7 marks)

Prochain acquired 100% of a sports goods and clothing manufacturer, Badex, a private limited company, on 1 June

2005. Prochain intends to develop its own brand of sports clothing which it will sell in the department stores. The

shareholders of Badex valued the company at $125 million based upon profit forecasts which assumed significant

growth in the demand for the ‘Badex’ brand name. Prochain had taken a more conservative view of the value of the

company and estimated the fair value to be in the region of $108 million to $112 million of which

$20 million relates to the brand name ‘Badex’. Prochain is only prepared to pay the full purchase price if profits from

the sale of ‘Badex’ clothing and sports goods reach the forecast levels. The agreed purchase price was $100 million

plus a further payment of $25 million in two years on 31 May 2007. This further payment will comprise a guaranteed

payment of $10 million with no performance conditions and a further payment of $15 million if the actual profits

during this two year period from the sale of Badex clothing and goods exceed the forecast profit. The forecast profit

on Badex goods and clothing over the two year period is $16 million and the actual profits in the year to 31 May

2006 were $4 million. Prochain did not feel at any time since acquisition that the actual profits would meet the

forecast profit levels. (8 marks)

After the acquisition of Badex, Prochain started developing its own sports clothing brand ‘Pro’. The expenditure in theperiod to 31 May 2006 was as follows:

The costs of the production and launch of the products include the cost of upgrading the existing machinery

($3 million), market research costs ($2 million) and staff training costs ($1 million).

Currently an intangible asset of $20 million is shown in the financial statements for the year ended 31 May 2006.

(6 marks)

Prochain owns a number of prestigious apartments which it leases to famous persons who are under a contract of

employment to promote its fashion clothing. The apartments are let at below the market rate. The lease terms are

short and are normally for six months. The leases terminate when the contracts for promoting the clothing terminate.

Prochain wishes to account for the apartments as investment properties with the difference between the market rate

and actual rental charged to be recognised as an employee benefit expense. (4 marks)

Assume a discount rate of 5·5% where necessary.

Required:

Discuss how the above items should be dealt with in the financial statements of Prochain for the year ended

31 May 2006 under International Financial Reporting Standards.

(25 marks)

第3题

on the building industry.

The company would like advice on how to treat certain items under IAS19, ‘Employee Benefits’ and IAS37 ‘Provisions,

Contingent Liabilities and Contingent Assets’. The company operates the Macaljoy (2006) Pension Plan which

commenced on 1 November 2006 and the Macaljoy (1990) Pension Plan, which was closed to new entrants from

31 October 2006, but which was open to future service accrual for the employees already in the scheme. The assets

of the schemes are held separately from those of the company in funds under the control of trustees. The following

information relates to the two schemes:

Macaljoy (1990) Pension Plan

The terms of the plan are as follows:

(i) employees contribute 6% of their salaries to the plan

(ii) Macaljoy contributes, currently, the same amount to the plan for the benefit of the employees

(iii) On retirement, employees are guaranteed a pension which is based upon the number of years service with the

company and their final salary

The following details relate to the plan in the year to 31 October 2007:

Warranties

Additionally the company manufactures and sells building equipment on which it gives a standard one year warranty

to all customers. The company has extended the warranty to two years for certain major customers and has insured

against the cost of the second year of the warranty. The warranty has been extended at nil cost to the customer. The

claims made under the extended warranty are made in the first instance against Macaljoy and then Macaljoy in turn

makes a counter claim against the insurance company. Past experience has shown that 80% of the building

equipment will not be subject to warranty claims in the first year, 15% will have minor defects and 5% will require

major repair. Macaljoy estimates that in the second year of the warranty, 20% of the items sold will have minor defects

and 10% will require major repair.

第4题

changing the way in which financial statements show particular transactions or events. In many ways, the impact of a new accounting standard requires the same detailed considerations as is required when an entity first moves from local Generally Accepted Accounting Practice to International Financial Reporting Standards (IFRS).

A new or significantly changed accounting standard often provides the key focus for examination of the financial statements of listed companies by national enforcers who issue common enforcement priorities. These priorities are often highlighted because of significant changes to accounting practices as a result of new or changed standards or because of the challenges faced by entities as a result of the current economic environment. Recent priorities have included recognition and measurement of deferred tax assets and impairment of financial and non-financial assets.

Required:

(a) (i) Discuss the key practical considerations, and financial statement implications which an entity should consider when implementing a move to a new IFRS. (7 marks)

(ii) Discuss briefly the reasons why regulators might focus on the impairment of non-financial assets and deferred tax assets in a period of slow economic growth, setting out the key areas which entities should focus on when accounting for these elements. (8 marks)

(b) Pod is a listed company specialising in the distribution and sale of photographic products and services. Pod’s statement of financial position included an intangible asset which was a portfolio of customers acquired from a similar business which had gone into liquidation. Pod changed its assessment of the useful life of this intangible asset from ‘finite’ to ‘indefinite’. Pod felt that it could not predict the length of life of the intangible asset, stating that it was impossible to foresee the length of life of this intangible due to a number of factors such as technological evolution, and changing consumer behaviour.

Pod has a significant network of retail branches. In its financial statements, Pod changed the determination of a cash generating unit (CGU) for impairment testing purposes at the level of each major product line, rather than at each individual branch. The determination of CGUs was based on the fact that each of its individual branches did not operate on a standalone basis as some income, such as volume rebates, and costs were dependent on the nature of the product line rather than on individual branches. Pod considered that cash inflows and outflows for individual branches did not provide an accurate assessment of the actual cash generated by those branches. Pod, however, has daily sales information and monthly statements of profit or loss produced for each individual branch and this information is used to make decisions about continuing to operate individual branches.

Required:

Discuss whether the changes to accounting practice suggested by Pod are acceptable under International Financial Reporting Standards. (8 marks)

Professional marks will be awarded in question 4 for clarity and quality of presentation. (2 marks)

第5题

and basketball teams. It has a financial year end of 31 May 2016. Emcee needs a new stadium to host sporting events which will be included as part of Emcee’s property, plant and equipment. Emcee therefore commenced construction on a new stadium on 1 February 2016, and this continued until its completion which was after the year end of 31 May 2016. The direct costs were $20 million in February 2016 and then $50 million in each month until the year end. Emcee has not taken out any specific borrowings to finance the construction of the stadium, but it has incurred finance costs on its general borrowings during the period, which could have been avoided if the stadium had not been constructed. Emcee has calculated that the weighted average cost of borrowings for the period 1 February–31 May 2016 on an annualised basis amounted to 9% per annum. Emcee needs advice on how to treat the borrowing costs in its financial statements for the year ending 31 May 2016. (6 marks)

(b) Emcee purchases and sells players’ registrations on a regular basis. Emcee must purchase registrations for that player to play for the club. Player registrations are contractual obligations between the player and Emcee. The costs of acquiring player registrations include transfer fees, league levy fees, and player agents’ fees incurred by the club. Often players’ former clubs are paid amounts which are contingent upon the performance of the player whilst they play for Emcee. For example, if a contracted basketball player scores an average of more than 20 points per game in a season, then an additional $5 million may become payable to his former club. Also, players’ contracts can be extended and this incurs additional costs for Emcee.

At the end of every season, which also is the financial year end of Emcee, the club reviews its playing staff and makes decisions as to whether they wish to sell any players’ registrations. These registrations are actively marketed by circulating other clubs with a list of players’ registrations and their estimated selling price. Players’ registrations are also sold during the season, often with performance conditions attached. Occasionally, it becomes clear that a player will not play for the club again because of, for example, a player sustaining a career threatening injury or being permanently removed from the playing squad for another reason. The playing registrations of certain players were sold after the year end, for total proceeds, net of associated costs, of $25 million. These registrations had a net book value of $7 million.

Emcee would like to know the financial reporting treatment of the acquisition, extension, review and sale of players’ registrations in the circumstances outlined above. (10 marks)

(c) Emcee uses the revaluation model to measure its stadiums. The directors have been offered $100 million from an airline for the property naming rights of all the stadiums for three years. There are two directors who are on the management boards of Emcee and the airline. Additionally, there are regulations in place by both the football and basketball leagues which regulate the financing of the clubs. These regulations prevent capital contributions from a related party which ‘increases equity without repayment in return’. The aim of these regulations is to promote sustainable business models. Sanctions imposed by the regulator include fines and withholding of prize monies. Emcee wishes to know how to take account of the naming rights in the valuation of the stadium and the potential implications of the financial regulations imposed by the leagues. (7 marks)

Required:

Discuss how the above events would be shown in the financial statements of Emcee under International Financial Reporting Standards.

Note: The split of the mark allocation is shown against each of the three issues above.

Professional marks will be awarded in question 3 for clarity and quality of presentation. (2 marks)

第6题

Section B – TWO questions ONLY to be attempted

(a) Mehran, a public limited company, has just acquired a company, which comprises a farming and mining business. Mehran wishes advice on how to fair value some of the assets acquired.

One such asset is a piece of land, which is currently used for farming. The fair value of the land if used for farming is $5 million. If the land is used for farming purposes, a tax credit currently arises annually, which is based upon the lower of 15% of the fair market value of land or $500,000 at the current tax rate. The current tax rate in the jurisdiction is 20%.

Mehran has determined that market participants would consider that the land could have an alternative use for residential purposes. The fair value of the land for residential purposes before associated costs is thought to be $7·4 million. In order to transform. the land from farming to residential use, there would be legal costs of $200,000, a viability analysis cost of $300,000 and costs of demolition of the farm buildings of $100,000. Additionally, permission for residential use has not been formally given by the legal authority and because of this, market participants have indicated that the fair value of the land, after the above costs, would be discounted by 20% because of the risk of not obtaining planning permission.

In addition, Mehran has acquired the brand name associated with the produce from the farm. Mehran has decided to discontinue the brand on the assumption that it will gain increased revenues from its own brands. Mehran has determined that if it ceases to use the brand, then the indirect benefits will be $20 million. If it continues to use the brand, then the direct benefit will be $17 million. (8 marks)

(b) Mehran wishes to fair value the inventory of the entity acquired. There are three different markets for the produce, which are mainly vegetables. The first is the local domestic market where Mehran can sell direct to retailers of the produce. The second domestic market is one where Mehran sells directly to manufacturers of canned vegetables. There are no restrictions on the sale of produce in either of the domestic markets other than the demand of the retailers and manufacturers. The final market is the export market but the government limits the amount of produce which can be exported. Mehran needs a licence from the government to export its produce. Farmers tend to sell all of the produce that they can in the export market and, when they do not have any further authorisation to export, they sell the remaining produce in the two domestic markets.

It is difficult to obtain information on the volume of trade in the domestic market where the produce is sold locally direct to retailers but Mehran feels that the market is at least as large as the domestic market – direct to manufacturers. The volumes of sales quoted below have been taken from trade journals.

(9 marks)

(c) Mehran owns a non-controlling equity interest in Erham, a private company, and wishes to fair value it as at its financial year end of 31 March 2016. Mehran acquired the ordinary share interest in Erham on 1 April 2014. During the current financial year, Erham has issued further equity capital through the issue of preferred shares to a venture capital fund.

As a result of the preferred share issue, the venture capital fund now holds a controlling interest in Erham. The terms of the preferred shares, including the voting rights, are similar to those of the ordinary shares, except that the preferred shares have a cumulative fixed dividend entitlement for a period of four years and the preferred shares rank ahead of the ordinary shares upon the liquidation of Erham. The transaction price for the preferred shares was $15 per share.

Mehran wishes to know the factors which should be taken into account in measuring the fair value of their holding in the ordinary shares of Erham at 31 March 2016 using a market-based approach. (6 marks)

Required:

Discuss the way in which Mehran should fair value the above assets with reference to the principles of IFRS 13 Fair Value Measurement.

Note: The mark allocation is shown against each of the three issues above.

Professional marks will be awarded in question 2 for clarity and quality of presentation. (2 marks)

第7题

is not easily distinguishable for preparers of financial statements. Some financial instruments may have both features, which can lead to inconsistency of reporting. The International Accounting Standards Board (IASB) has agreed that greater clarity may be required in its definitions of assets and liabilities for debt instruments. It is thought that defining the nature of liabilities would help the IASB’s thinking on the difference between financial instruments classified as equity and liabilities.

Required:

(i) Discuss the key classification differences between debt and equity under International Financial Reporting Standards.

Note: Examples should be given to illustrate your answer. (9 marks)

(ii) Explain why it is important for entities to understand the impact of the classification of a financial instrument as debt or equity in the financial statements. (5 marks)

(b) The directors of Avco, a public limited company, are reviewing the financial statements of two entities which are acquisition targets, Cavor and Lidan.They have asked for clarification on the treatment of the following financial instruments within the financial statements of the entities.

Cavor has two classes of shares: A and B shares. A shares are Cavor’s ordinary shares and are correctly classed as equity. B shares are not mandatorily redeemable shares but contain a call option allowing Cavor to repurchase them. Dividends are payable on the B shares if, and only if, dividends have been paid on the A ordinary shares. The terms of the B shares are such that dividends are payable at a rate equal to that of the A ordinary shares. Additionally, Cavor has also issued share options which give the counterparty rights to buy a fixed number of its B shares for a fixed amount of $10 million. The contract can be settled only by the issuance of shares for cash by Cavor.

Lidan has in issue two classes of shares: A shares and B shares. A shares are correctly classified as equity. Two million B shares of nominal value of $1 each are in issue. The B shares are redeemable in two years’ time at the option of Lidan. Lidan has a choice as to the method of redemption of the B shares. It may either redeem the B shares for cash at their nominal value or it may issue one million A shares in settlement. A shares are currently valued at $10 per share. The lowest price for Lidan’s A shares since its formation has been $5 per share.

Required:

Discuss whether the above arrangements regarding the B shares of each of Cavor and Lidan should be treated as liabilities or equity in the financial statements of the respective issuing companies. (9 marks)

Professional marks will be awarded in question 4 for clarity and quality of presentation. (2 marks)

第8题

ne aspect of its business is to provide low-cost homes through the establishment of a separate entity, known as a housing association. Minco purchases land and transfers ownership to the housing association before construction starts. Minco sells rights to occupy the housing units to members of the public but the housing association is the legal owner of the building. The housing association enters into loan agreements with the bank to cover the costs of building the homes. However, Minco negotiates and acts as guarantor for the loan, and bears the risk of increases in the loan’s interest rate above a specified rate. Currently, the housing rights are normally all sold out on the completion of a project.

Minco enters into discussions with a housing contractor regarding the construction of the housing units but the agreement is between the housing association and the contractor. Minco is responsible for any construction costs in excess of the amount stated in the contract and is responsible for paying the maintenance costs for any units not sold. Minco sets up the board of the housing association, which comprises one person representing Minco and two independent board members.

Minco recognises income for the entire project when the land is transferred to the housing association. The income recognised is the difference between the total sales price for the finished housing units and the total estimated costs for construction of the units. Minco argues that the transfer of land represents a sale of goods which fulfils the revenue recognition criteria in IAS 18 Revenue. (7 marks)

(b) Minco often sponsors professional tennis players in an attempt to improve its brand image. At the moment, it has a three-year agreement with a tennis player who is currently ranked in the world’s top ten players. The agreement is that the player receives a signing bonus of $20,000 and earns an annual amount of $50,000, paid at the end of each year for three years, provided that the player has competed in all the specified tournaments for each year. If the player wins a major tournament, she receives a bonus of 20% of the prize money won at the tournament. In return, the player is required to wear advertising logos on tennis apparel, play a specified number of tournaments and attend photo/film sessions for advertising purposes. The different payments are not interrelated. (5 marks)

(c) Minco leased its head office during the current accounting period and the agreement terminates in six years’ time. There is a clause in the operating lease relating to the internal condition of the property at the termination of the lease. The clause states that the internal condition of the property should be identical to that at the outset of the lease. Minco has improved the building by adding another floor to part of the building during the current accounting period. There is also a clause which enables the landlord to recharge Minco for costs relating to the general disrepair of the building at the end of the lease. In addition, the landlord can recharge any costs of repairing the roof immediately. The landlord intends to replace part of the roof of the building during the current period. (5 marks)

(d) Minco acquired a property for $4 million and annual depreciation of $300,000 is charged on the straight line basis. At the end of the previous financial year of 31 May 2013, when accumulated depreciation was $1 million, a further amount relating to an impairment loss of $350,000 was recognised, which resulted in the property being valued at its estimated value in use. On 1 October 2013, as a consequence of a proposed move to new premises, the property was classified as held for sale. At the time of classification as held for sale, the fair value less costs to sell was $2·4 million. At the date of the published interim financial statements, 1 December 2013, the property market had improved and the fair value less costs to sell was reassessed at $2·52 million and at the year end on 31 May 2014 it had improved even further, so that the fair value less costs to sell was $2·95 million. The property was sold on 5 June 2014 for $3 million. (6 marks)

Required:

Discuss how the above items should be dealt with in the financial statements of Minco.

Note: The mark allocation is shown against each of the four issues above.

Professional marks will be awarded in question 3 for clarity and quality of presentation. (2 marks)

第9题

Section B – TWO questions ONLY to be attempted

Aspire, a public limited company, operates many of its activities overseas. The directors have asked for advice on the correct accounting treatment of several aspects of Aspire’s overseas operations. Aspire’s functional currency is the dollar.

(a) Aspire has created a new subsidiary, which is incorporated in the same country as Aspire. The subsidiary has issued 2 million dinars of equity capital to Aspire, which paid for these shares in dinars. The subsidiary has also raised 100,000 dinars of equity capital from external sources and has deposited the whole of the capital with a bank in an overseas country whose currency is the dinar. The capital is to be invested in dinar denominated bonds. The subsidiary has a small number of staff and its operating expenses, which are low, are incurred in dollars. The profits are under the control of Aspire. Any income from the investment is either passed on to Aspire in the form. of a dividend or reinvested under instruction from Aspire. The subsidiary does not make any decisions as to where to place the investments.

Aspire would like advice on how to determine the functional currency of the subsidiary. (7 marks)

(b) Aspire has a foreign branch which has the same functional currency as Aspire. The branch’s taxable profits are determined in dinars. On 1 May 2013, the branch acquired a property for 6 million dinars. The property had an expected useful life of 12 years with a zero residual value. The asset is written off for tax purposes over eight years. The tax rate in Aspire’s jurisdiction is 30% and in the branch’s jurisdiction is 20%. The foreign branch uses the cost model for valuing its property and measures the tax base at the exchange rate at the reporting date.

Aspire would like an explanation (including a calculation) as to why a deferred tax charge relating to the asset arises in the group financial statements for the year ended 30 April 2014 and the impact on the financial statements if the tax base had been translated at the historical rate. (6 marks)

(c) On 1 May 2013, Aspire purchased 70% of a multi-national group whose functional currency was the dinar. The purchase consideration was $200 million. At acquisition, the net assets at cost were 1,000 million dinars. The fair values of the net assets were 1,100 million dinars and the fair value of the non-controlling interest was 250 million dinars.

Aspire uses the full goodwill method. Aspire wishes to know how to deal with goodwill arising on the above acquisition in the group financial statements for the year ended 30 April 2014. (5 marks)

(d) Aspire took out a foreign currency loan of 5 million dinars at a fixed interest rate of 8% on 1 May 2013. The interest is paid at the end of each year. The loan will be repaid after two years on 30 April 2015. The interest rate is the current market rate for similar two-year fixed interest loans.

Aspire requires advice on how to account for the loan and interest in the financial statements for the year ended 30 April 2014. (5 marks)

Aspire has a financial statement year end of 30 April 2014 and the average currency exchange rate for the year is not materially different from the actual rate.

Required:

Advise the directors of Aspire on their various requests above, showing suitable calculations where necessary.

Note: The mark allocation is shown against each of the four issues above.

Professional marks will be awarded in question 2 for clarity and quality of presentation. (2 marks)

第10题

Section A – THIS ONE question is compulsory and MUST be attempted

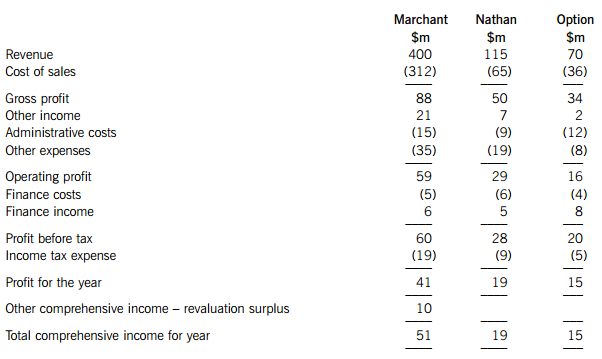

The following draft financial statements relate to Marchant, a public limited company.

Marchant Group: Draft statements of profit or loss and other comprehensive income for the year ended 30 April 2014.

The following information is relevant to the preparation of the group statement of profit or loss and other comprehensive income:

1. On 1 May 2012, Marchant acquired 60% of the equity interests of Nathan, a public limited company. The purchase consideration comprised cash of $80 million and the fair value of the identifiable net assets acquired was $110 million at that date. The fair value of the non-controlling interest (NCI) in Nathan was $45 million on 1 May 2012. Marchant wishes to use the ‘full goodwill’ method for all acquisitions. The share capital and retained earnings of Nathan were $25 million and $65 million respectively and other components of equity were $6 million at the date of acquisition. The excess of the fair value of the identifiable net assets at acquisition is due to non-depreciable land.

Goodwill has been impairment tested annually and as at 30 April 2013 had reduced in value by 20%. However at 30 April 2014, the impairment of goodwill had reversed and goodwill was valued at $2 million above its original value. This upward change in value has already been included in above draft financial statements of Marchant prior to the preparation of the group accounts.

2. Marchant disposed of an 8% equity interest in Nathan on 30 April 2014 for a cash consideration of $18 million and had accounted for the gain or loss in other income. The carrying value of the net assets of Nathan at 30 April 2014 was $120 million before any adjustments on consolidation. Marchant accounts for investments in subsidiaries using IFRS 9 Financial Instruments and has made an election to show gains and losses in other comprehensive income. The carrying value of the investment in Nathan was $90 million at 30 April 2013 and $95 million at 30 April 2014 before the disposal of the equity interest.

3. Marchant acquired 60% of the equity interests of Option, a public limited company, on 30 April 2012. The purchase consideration was cash of $70 million. Option’s identifiable net assets were fair valued at $86 million and the NCI had a fair value of $28 million at that date. On 1 November 2013, Marchant disposed of a 40% equity interest in Option for a consideration of $50 million. Option’s identifiable net assets were $90 million and the value of the NCI was $34 million at the date of disposal. The remaining equity interest was fair valued at $40 million. After the disposal, Marchant exerts significant influence. Any increase in net assets since acquisition has been reported in profit or loss and the carrying value of the investment in Option had not changed since acquisition. Goodwill had been impairment tested and no impairment was required. No entries had been made in the financial statements of Marchant for this transaction other than for cash received.

4. Marchant sold inventory to Nathan for $12 million at fair value. Marchant made a loss on the transaction of $2 million and Nathan still holds $8 million in inventory at the year end.

5. The following information relates to Marchant’s pension scheme:

The pension costs have not been accounted for in total comprehensive income.

6. On 1 May 2012, Marchant purchased an item of property, plant and equipment for $12 million and this is being depreciated using the straight line basis over 10 years with a zero residual value. At 30 April 2013, the asset was revalued to $13 million but at 30 April 2014, the value of the asset had fallen to $7 million. Marchant uses the revaluation model to value its non-current assets. The effect of the revaluation at 30 April 2014 had not been taken into account in total comprehensive income but depreciation for the year had been charged.

7. On 1 May 2012, Marchant made an award of 8,000 share options to each of its seven directors. The condition attached to the award is that the directors must remain employed by Marchant for three years. The fair value of each option at the grant date was $100 and the fair value of each option at 30 April 2014 was $110. At 30 April 2013, it was estimated that three directors would leave before the end of three years. Due to an economic downturn, the estimate of directors who were going to leave was revised to one director at 30 April 2014. The expense for the year as regards the share options had not been included in profit or loss for the current year and no directors had left by 30 April 2014.

8. A loss on an effective cash flow hedge of Nathan of $3 million has been included in the subsidiary’s finance costs.

9. Ignore the taxation effects of the above adjustments unless specified. Any expense adjustments should be amended in other expenses.

Required:

(a) (i) Prepare a consolidated statement of profit or loss and other comprehensive income for the year ended 30 April 2014 for the Marchant Group. (30 marks)

(ii) Explain, with suitable calculations, how the sale of the 8% interest in Nathan should be dealt with in the group statement of financial position at 30 April 2014. (5 marks)

(b) The directors of Marchant have strong views on the usefulness of the financial statements after their move to International Financial Reporting Standards (IFRSs). They feel that IFRSs implement a fair value model. Nevertheless, they are of the opinion that IFRSs are failing users of financial statements as they do not reflect the financial value of an entity.

Required:

Discuss the directors’ views above as regards the use of fair value in IFRSs and the fact that IFRSs do not reflect the financial value of an entity. (9 marks)

(c) Marchant plans to update its production process and the directors feel that technology-led production is the only feasible way in which the company can remain competitive. Marchant operates from a leased property and the leasing arrangement was established in order to maximise taxation benefits. However, the financial statements have not shown a lease asset or liability to date.

A new financial controller joined Marchant just after the financial year end of 30 April 2014 and is presently reviewing the financial statements to prepare for the upcoming audit and to begin making a loan application to finance the new technology. The financial controller feels that the lease relating to both the land and buildings should be treated as a finance lease but the finance director disagrees. The finance director does not wish to recognise the lease in the statement of financial position and therefore wishes to continue to treat it as an operating lease. The finance director feels that the lease does not meet the criteria for a finance lease, and it was made clear by the finance director that showing the lease as a finance lease could jeopardise the loan application.

Required:

Discuss the ethical and professional issues which face the financial controller in the above situation. (6 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!