重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

During the year to 31 December 20X6, Marek Co sold goods to Rooney Co, giving rise to an unrealised profit in inventory of $550,000 at the year end. Marek Co’s profit after tax for the year ended 31 December 20X6 was $3·2m.

What amount will be presented as the non-controlling interest in the consolidated statement of financial position of Rooney Co as at 31 December 20X6?

A.$1,895,000

B.$1,495,000

C.$1,910,000

D.$1,880,000

更多“Rooney Co acquired 70% of the equity share capital of Marek Co, its only subsidiary, on 1”相关的问题

更多“Rooney Co acquired 70% of the equity share capital of Marek Co, its only subsidiary, on 1”相关的问题

第1题

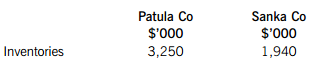

entory had a carrying amount of $600,000 but a fair value of $800,000. By 31 December 20X5, 70% of this inventory had been sold by Sanka Co.

The individual statements of financial position at 31 December 20X5 for both companies show the following:

What will be the total inventories figure in the consolidated statement of financial position of Patula Co as at 31 December 20X5?

A.$5,250,000

B.$5,330,000

C.$5,130,000

D.$5,238,000

第2题

Shiba Co entered into a non-cancellable four-year operating lease to hire a photocopier on 1 January 20X7. The terms of the lease agreement were as follows:

What is the charge in the statement of profit or loss of Shiba Co for the year ended 31 December 20X7 in respect of this operating lease?

A.$2,375

B.$4,000

C.$4,750

D.$5,250

第3题

The following two issues relate to Spiko Co’s mining activities:

Issue 1: Spiko Co began operating a new mine in January 20X3 under a five-year government licence which required Spiko Co to landscape the area after mining ceased at an estimated cost of $100,000.

Issue 2: During 20X4, Spiko Co’s mining activities caused environmental pollution on an adjoining piece of government land. There is no legislation which requires Spiko Co to rectify this damage, however, Spiko Co does have a published environmental policy which includes assurances that it will do so. The estimated cost of the rectification is $1,000,000.

In accordance with IAS 37 Provisions, Contingent Liabilities and Contingent Assets, which of the following statements is correct in respect of Spiko Co’s financial statements for the year ended 31 December 20X4?

A.A provision is required for the cost of both issues 1 and 2

B.Both issues 1 and 2 require disclosure only

C.A provision is required for the cost of issue 1 but issue 2 requires disclosure only

D.Issue 1 requires disclosure only and issue 2 should be ignored

第4题

cently purchased investments in publically-traded equity shares:

Investment 1 – 10% of the issued share capital of Haruka Co. This shareholding was acquired as a long-term investment as Zinet Co wishes to participate as an active shareholder of Haruka Co.

Investment 2 – 10% of the issued share capital of Lukas Co. This shareholding was acquired for speculative purposes and Zinet Co expects to sell these shares in the near future.

Neither of these shareholdings gives Zinet Co significant influence over the investee companies.

Wherever possible, the directors of Zinet Co wish to avoid taking any fair value movements to profit or loss, so as to minimise volatility in reported earnings.

How should the fair value movements in these investments be reported in Zinet Co’s financial statements for the year ended 31 March 20X9?

A.In profit or loss for both investments

B.In other comprehensive income for both investments

C.In profit or loss for investment 1 and in other comprehensive income for investment 2

D.In other comprehensive income for investment 1 and in profit or loss for investment 2

第5题

se of its equipment.

Which of the following correctly reflects what this change represents and how it should be applied?

A.It is a change of accounting policy and must be applied prospectively

B.It is a change of accounting policy and must be applied retrospectively

C.It is a change of accounting estimate and must be applied retrospectively

D.It is a change of accounting estimate and must be applied prospectively

第6题

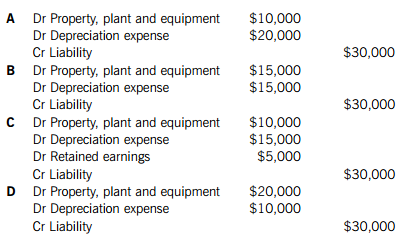

which cost $90,000 and had a useful life of six years. The grant was netted off against the cost of the equipment. On 1 January 20X7, when the equipment had a carrying amount of $50,000, its use was changed so that it was no longer being used in accordance with the grant. This meant that the grant needed to be repaid in full but by 31 December 20X7, this had not yet been done.

Which journal entry is required to reflect the correct accounting treatment of the government grant and the equipment in the financial statements of Gardenbugs Co for the year ended 31 December 20X7?

A.A

B.B

C.C

D.D

第7题

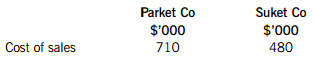

from the individual statements of profit or loss for the year ended 31 March 20X7: Parket Co consistently made sales of $20,000 per month to Suket Co throughout the year. At the year end, Suket Co held $20,000 of this in inventory.

Parket Co made a mark-up on cost of 25% on all sales to Suket Co.

What is Parket Co’s consolidated cost of sales for the year ended 31 March 20X7?

A.$954,000

B.$950,000

C.$774,000

D.$766,000

第8题

?

(1) The acquisition of 60% of Zakron Co’s equity share capital on 1 March 20X7. Zakron Co’s activities are significantly different from the rest of the Poulgo group of companies

(2) The offer to acquire 70% of Unto Co’s equity share capital on 1 November 20X7. The negotiations were finally signed off during January 20X8

(3) The acquisition of 45% of Speeth Co’s equity share capital on 31 December 20X7. Poulgo Co is able to appoint three of the ten members of Speeth Co’s board

A.1 only

B.2 and 3

C.3 only

D.1 and 2

第9题

Which of the following is NOT a duty of the IFRS Interpretations Committee?

A.To interpret the application of International Financial Reporting Standards

B.To work directly with national standard setters to bring about convergence with IFRS

C.To provide guidance on financial reporting issues not specifically addressed in IFRSs

D.To publish draft interpretations for public comment

第10题

The following trial balance relates to Downing Co as at 31 March 2016:

The following notes are relevant:

(i) Revenue includes an amount of $16 million for a sale made on 1 April 2015. The sale relates to a single product and includes ongoing servicing from Downing Co for four years. The normal selling price of the product and the servicing would be $18 million and $500,000 per annum ($2 million in total) respectively.

(ii) The contract asset is comprised of contract costs incurred at 31 March 2016 of $15 million less a payment of $10 million from the customer. The agreed transaction price for the total contract is $30 million and the total expected costs are $24 million. Downing Co uses an input method based on costs incurred to date relative to the total expected costs to determine the progress towards completion of its contracts.

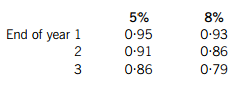

(iii) Downing Co issued 300,000 $100 5% convertible loan notes on 1 April 2015. The loan notes can be converted to equity shares on the basis of 25 shares for each $100 loan note on 31 March 2018 or redeemed at par for cash on the same date. An equivalent loan note without the conversion rights would have required an interest rate of 8%.

The present value of $1 receivable at the end of each year, based on discount rates of 5% and 8%, are:

(iv) Non-current assets:

Due to rising property prices, Downing Co decided to revalue its land and buildings on 1 April 2015 to their market value. The values were confirmed at that date as land $16 million and buildings $52·2 million with the buildings having an estimated remaining life of 18 years at the date of revaluation. Downing Co intends to make a transfer from the revaluation surplus to retained earnings in respect of the annual realisation of the revaluation surplus. Ignore deferred tax on the revaluation.

Plant and equipment is depreciated at 15% per annum using the reducing balance method.

During the current year, the income from royalties relating to the patent had declined considerably and the directors are concerned that the value of the patent may be impaired. A study at the year end concluded that the present value of the future estimated net cash flows from the patent at 31 March 2016 is $3·25 million; however, Downing Co also has a confirmed offer of $3·4 million to sell the patent immediately at that date.

No depreciation/amortisation has yet been charged on any non-current asset for the year ended 31 March 2016. All depreciation/amortisation is charged to cost of sales.

There were no acquisitions or disposals of non-current assets during the year.

(v) The directors estimate a provision for income tax for the year ended 31 March 2016 of $11·4 million is required. The balance on current tax in the trial balance represents the under/over provision of the tax liability for the year ended 31 March 2015. At 31 March 2016, Downing Co had taxable temporary differences of $18·5 million requiring a provision for deferred tax. Any deferred tax movement should be reported in profit or loss. The income tax rate applicable to Downing Co is 20%.

Required:

(a) Prepare the statement of profit or loss and other comprehensive income for Downing Co for the year ended 31 March 2016.

(b) Prepare the statement of changes in equity for Downing Co for the year ended 31 March 2016.

(c) Prepare the statement of financial position of Downing Co as at 31 March 2016.

Notes to the financial statements are not required. Work to the nearest $1,000.

The following mark allocation is provided as guidance for these requirements:

(a) 11 marks

(b) 4 marks

(c) 10 marks

(d) The finance director of Downing Co has correctly calculated the company’s basic and diluted earnings per share (EPS) to be disclosed in the financial statements for the year ended 31 March 2016 at 148·2 cents and 119·4 cents respectively.

On seeing these figures, the chief executive officer (CEO) is concerned that the market will react badly knowing that the company’s EPS in the near future will be only 119·4 cents, a fall of over 19% on the current year’s basic EPS.

Required:

Explain why and what aspect of Downing Co’s capital structure is causing the basic EPS to be diluted and comment on the validity of the CEO’s concerns. (5 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!