重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

SUPPLEMENTARY INSTRUCTIONS

1. You should assume that the tax rates and allowances shown below will continue to apply for the foreseeable future.

2. Calculations and workings should be rounded down to the nearest HK$.

3. Apportionments need only be made to the nearest month, unless the law and prevailing practice require otherwise.

4. All workings should be shown.

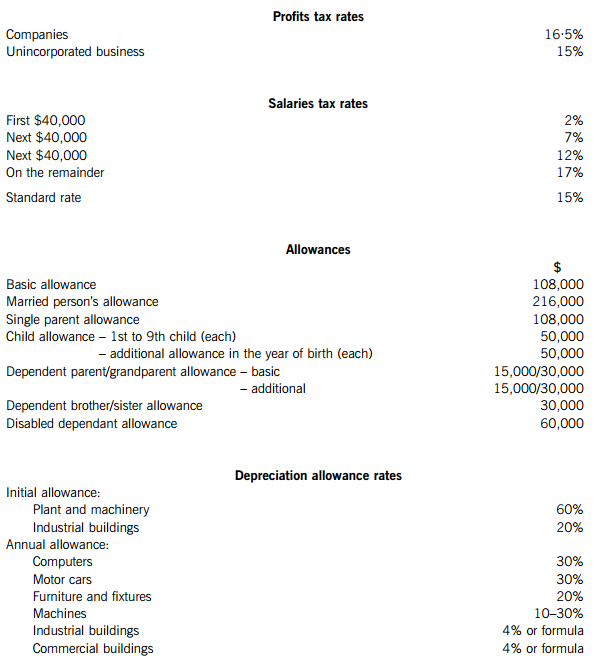

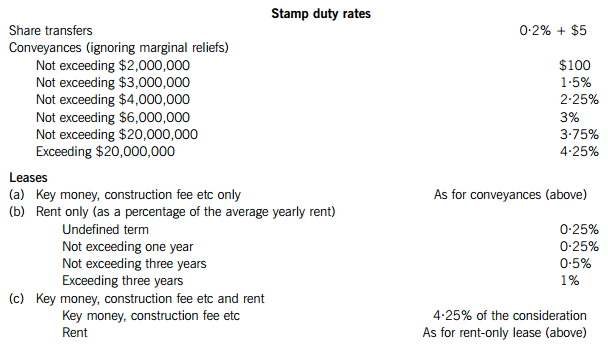

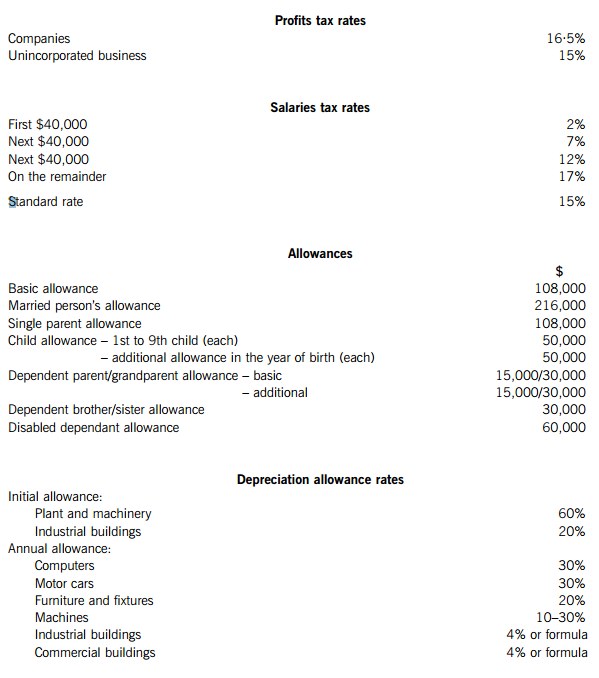

TAX RATES AND ALLOWANCES

The following 2010/11 tax rates and allowances are to be used in answering the questions.

Section A – BOTH questions are compulsory and MUST be attempted

1.

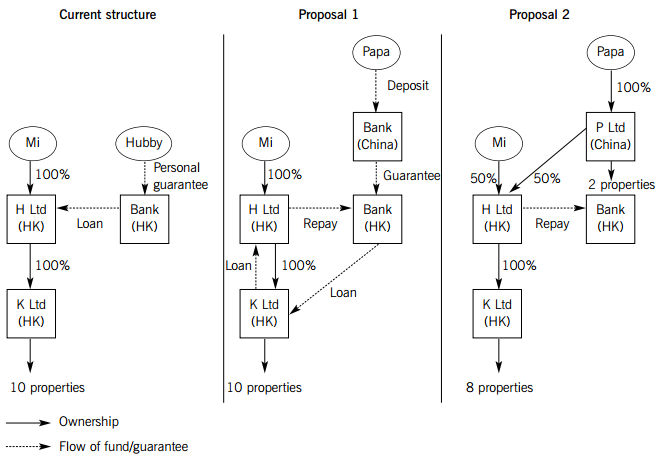

Ms Mi (Mi) is the sole shareholder of H Ltd, which was incorporated in Hong Kong during December 2010 for the purpose of acquiring the shares in K Ltd at the cost of $50 million. K Ltd is a Hong Kong incorporated company holding ten properties in Hong Kong. These properties are classified as ‘trading stock’ in K Ltd’s accounts on the basis that they are held for sale at a profit. The acquisition cost was financed by a bank loan which was secured by a personal guarantee given by Mi’s husband (Hubby). The current structure is illustrated on the left hand side of the diagram below:

You recently met Mi who advised you that she was going to divorce her husband. Thereafter, her husband will withdraw his personal guarantee on the bank loan, leading to the loan to be called back by the bank. Mi has sought help from her father (Papa), who has given two proposals for her consideration. These two proposals, as illustrated in the diagrams above, have the following details:

Proposal 1: A new bank loan will be extended from the bank to K Ltd, which is secured by a deposit placed by Papa with the Bank’s associate in China. K Ltd will on-lend the bank loan money to H Ltd interest free, to enable H Ltd to repay the old bank loan. Papa’s deposit will earn interest at the same rate that K Ltd pays on the new bank loan minus a 0.5% bank fee.

Proposal 2: Papa will invest, via P Ltd, a company incorporated in China, into H Ltd as a 50% shareholder. H Ltd could use the additional fund to repay the bank loan. However, he is neutral as to whether the 50% shareholding is acquired by way of new shares issued by H Ltd to him directly, or the sale of shares in H Ltd from Mi to him. If Mi sells her 50% shareholding to Papa, she will lend the money, interest-free, to H Ltd. Mi anticipates that she will make a significant profit on the sale and since K Ltd is trading in properties, she is concerned that her profit from the sale of the shares will also be taxed. Moreover, under this proposal, Papa also requests that after the shareholding change, K Ltd will sell two properties to P Ltd at cost, which is about 30% below the current market price.

Apart from the above two proposals from Papa, Mi also discussed with you the following alternative:

Proposal 3: K Ltd will change the strategy for holding the properties from trading to investment. These properties will be leased out to earn rental income. K Ltd will then assign its income rights under these leases to an independent party for a lump sum consideration. The lump sum will either be paid up as dividend or lent to H Ltd interest-free, to enable H Ltd to repay the existing bank loan.

As a friend of Mi as well as a professional tax consultant, you have promised Mi to review the above proposals from a Hong Kong tax perspective, and write a report to her.

Required:

Prepare a report for Ms Mi addressing the tax issues set out below, including supporting calculations where appropriate.

(a) Current structure – Comment on the tax effectiveness of the current funding structure in terms of the funding cost incurred by H Ltd. (2 marks)

(b) Proposal 1 – As compared with the current funding structure, advise whether there are any profits tax implications arising from Proposal 1 for:

(i) H Ltd; and (1 mark)

(ii) K Ltd. (4 marks)

(c) Proposal 2 – Advise on:

(i) The profits tax and stamp duty implications for H Ltd and P Ltd, if P Ltd subscribes for new shares to be issued by H Ltd directly to P Ltd; (2 marks)

(ii) The profits tax and stamp duty implications for Ms Mi if she sells 50% of her shareholding in H Ltd to P Ltd. Discuss also whether Ms Mi’s concern that her tax position will be affected by K Ltd’s property trading business is valid; and (15 marks)

(iii) The profits tax and stamp duty implications for K Ltd if it sells the two properties to P Ltd at cost. (8 marks)

(d) Proposal 3 – Advise on the profits tax implications for K Ltd arising from the change of holding strategy for the properties and the subsequent assignment of its income rights under the leases. (4 marks)

Notes:

1. Where appropriate, the effect of the HK–China Double Tax Arrangement (the DTA) on the transactions should be mentioned, but you are not required to discuss the detailed provisions in the DTA.

2. You should ignore provisional tax and overseas tax throughout this question.

3. You are not required to discuss any accounting treatments, and their relevant standards or principles in relation to the transactions in this case.

Professional marks will be awarded in question 1 for the appropriateness of the format and presentation of the report and the effectiveness with which its advice is communicated. (2 marks)

2.

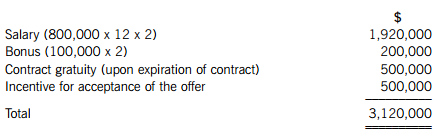

Kelvin King, a Canadian resident, has been offered a new job in a Hong Kong resident company (the Company) under a two-year contract from 1 April 2012 to 31 March 2014. The following draft total remuneration package has been offered for his consideration:

Other major terms of the contract include:

(1) Kelvin is not allowed to work for another company engaged in the same business or industry for 12 months after the cessation or expiration of his contract with the Company.

(2) Subject to application by Kelvin and approval by the Company, a staff quarter can be provided by the Company at a rent equivalent to 5% of Kelvin’s monthly salary. Details of the choices of quarters are available in the Personnel Department upon request.

(3) Kelvin is entitled to benefit from the Company’s medical insurance scheme, which allows him to receive outpatient services at no cost. The annual premium per employee paid by the Company under the scheme is $6,000.

(4) Kelvin is entitled to annual leave of three weeks.

(5) Kelvin is given an option to choose one of two share-based benefits under the Company’s Staff Incentive Scheme:

(i) Share option benefit – Kelvin will be granted an option to purchase 30,000 shares in the Company at a favourable option price. The options are unconditional.

(ii) Share award benefit – Kelvin will be granted 25,000 shares in the Company. Half of the share award has no vesting period, while the other half has a vesting period of 18 months during which Kelvin is required to remain in employment with the Company; and he is only entitled to these shares at the end of the vesting period.

Kelvin does not own a property in Hong Kong, nor does he have any plan to buy one in the short term. It is likely that he will rent a furnished apartment near his workplace as he has been advised that the Company quarter is unfurnished and has no club facilities.

Kelvin plans to return to Canada after the contract expires on 31 March 2014. He is thinking of choosing the share option benefit as he believes that if he exercises the share option after he returns to Canada, no Hong Kong tax will be payable.

The Company will allow Kelvin to restructure his two-year remuneration package as long as the total remuneration package (other than the share-based benefits) at the end of the contract does not exceed $3,120,000.

Required:

As tax consultant to Kelvin King, write a letter to him giving advice on the following:

(a) The Hong Kong salaries tax position of the draft package. Note: you are NOT required to calculate his assessable/chargeable income or tax payable. (20 marks)

(b) How Kelvin should restructure his remuneration package so as to minimise the amount of salaries tax he will have to pay in Hong Kong. (6 marks)

Professional marks will be awarded in question 2 for the appropriateness of the format and presentation of the letter and the effectiveness with which its advice is communicated. (2 marks)

Section B – TWO questions ONLY to be attempted

3.

(a) AB Ltd, a Hong Kong resident company, is organising a pop music concert to be staged in Hong Kong in January 2012. AB Ltd has appointed another Hong Kong resident company, CD Ltd, to procure performances by various overseas artists at the concert. CD Ltd has entered into an agreement with Mr X, the US resident manager of a US resident pop star, for the performance of that pop star at the concert for a fee of $3,000,000. AB Ltd will pay $3,300,000 to CD Ltd, which will then pay $3,000,000 to Mr X. The fee payable by Mr X to the US pop star is $2,700,000.

Required:

Explain the withholding obligations, if any, imposed under the Inland Revenue Ordinance on each of the parties concerned and compute, with explanations, the amount of tax to be withheld. (8 marks)

(b) KK Ltd is carrying on a trading business in Hong Kong, preparing accounts to 31 March each year. On 1 February 2011, it entered into a lease agreement to lease a motor vehicle, which has since been used in KK Ltd’s business, from an unrelated leasing company. The lease agreement is for a term of 24 months, with a monthly lease payment of $45,000 commencing from 1 February 2011. The cash cost of the motor vehicle was $840,000. The agreement provides KK Ltd with an option to acquire the motor vehicle at the end of the lease period upon payment of a small residual amount; and it is expected that the residual value will be higher than the exercise price.

Required:

Explain the tax implications of the lease agreement to KK Ltd, clearly identifying the expenditures it is entitled to claim with respect to the motor vehicle for the year of assessment 2010/11. (9 marks)

4.

MRS (HK) Ltd (MRS-HK) is a Hong Kong-incorporated company, which is resident and carrying on business in Hong Kong. During the month of July 2011, MRS-HK sent a team of five specialist staff to its associated company in China, MRS (China) Ltd (MRS-China), to work for them on a China project for a period of two weeks. All the associated costs including accommodation and meals were settled by MRS-China.

After the assignment, MRS-HK intended to issue a debit note to MRS-China seeking to recover the related employment costs of the five specialist staff on this project in the amount of HK$50,000. However, MRS-HK was subsequently advised by MRS-China that recharging these employment costs would result in China individual income tax being payable by the five specialist staff. All five of the specialist staff members are resident in Hong Kong.

Required:

(a) Discuss the Hong Kong salaries tax positions of the five specialist staff of MRS (HK) Ltd in respect of their services performed in China during July 2011.

Note: For the purpose of this part of the question only, you should answer based on the Hong Kong Inland Revenue Ordinance, and ignore the application of the double tax arrangement between Hong Kong and the PRC. (6 marks)

(b) Based on Article 14 of the double taxation agreement (DTA) signed between Hong Kong and the PRC, which is extracted below, explain how the recharge by MRS (HK) Ltd to recover the employment costs from MRS (China) Ltd may affect the exemption from China tax available to the five specialist staff members. You should clearly identify the crucial factors necessary for the DTA exemption to be available.

‘Article 14 Income from Employment

1. Subject to the provisions of Articles 15, 17, 18, 19 and 20, salaries, wages and other similar remuneration derived by a resident of One Side in respect of an employment shall be taxable only in that Side unless the employment is exercised in the Other Side. If the employment is exercised in the Other Side, such remuneration as is derived therefrom may be taxed in that Other Side.

2. Notwithstanding the provisions of paragraph 1 of this Article, remuneration derived by a resident of One Side in respect of an employment exercised in the Other Side shall be taxable only in the first-mentioned Side if all the following conditions are satisfied:

(a) the recipient is present in the Other Side for a period or periods not exceeding in the aggregate 183 days in any 12-month period commencing or ending in the taxable period concerned, and

(b) the remuneration is paid by, or on behalf of, an employer who is not a resident of the Other Side, and

(c) the remuneration is not borne by a permanent establishment which the employer has in the Other Side.’ (6 marks)

(c) Assuming that both Hong Kong salaries tax and China individual income tax will be imposed on the five specialist staff in relation to the services rendered in China, advise on the possible relief or measures that are available to them to avoid double taxation, based on the Hong Kong Inland Revenue Ordinance and Article 21 of the double taxation agreement signed between Hong Kong and the PRC as extracted below.

‘Article 21 Methods for Elimination of Double Taxation

2. In the Hong Kong Special Administrative Region, double taxation shall be avoided as follows:

Subject to the provisions of the tax laws of the Hong Kong Special Administrative Region … Mainland tax paid in the Mainland of China in accordance with the provisions of this Arrangement in respect of any item of income derived from sources in the Mainland of China by a resident of the Hong Kong Special Administrative Region shall be allowed as a credit against Hong Kong Special Administrative Region tax imposed on that resident. However, the amount of the credit shall not exceed the amount of Hong Kong Special Administrative Region tax in respect of that item of income computed in accordance with the tax laws and regulations of the Hong Kong Special Administrative Region.’ (5 marks)

5.

(a) Mr Look carries on a consultancy business in the form. of a sole proprietorship in Hong Kong. He closes his accounts on 31 December each year. In the course of preparing his profits tax computation for the year of assessment 2010/11, Mr Look discovered that an expense of $10,000, being the cost of hiring a member of temporary staff for a special project during the year ended 31 December 2005, had been omitted from his business accounts and thus this deduction was not claimed in the tax return for 2005/06. He wonders whether he can now ask the Inland Revenue Department to revise the assessment for 2005/06.

Required:

Advise Mr Look of his right of action, if any, to revise the assessment for 2005/06 to take into account the cost of hiring the temporary member of staff during the year 2005. (9 marks)

(b) David Pang owns a flat in Regent Court, a residential building in Causeway Bay. The residential building has 150 flats in total. According to the deed of mutual covenants, the roof of the residential building is part of the building common area, and each owner of an individual flat is entitled to the same number of undivided shares in the building common area.

On 1 June 2010, David Pang, as the chairman of the Incorporated Owner of Regent Court, entered into an agreement with a company, granting it the right to erect a neon advertising sign on the roof for a licence fee of $100,000 per annum. The licence fee is to be used to meet the building management expenses.

Recently, David Pang received from the Inland Revenue Department a property tax return for the year of assessment 2010/11. The return was addressed to ‘The Incorporated Owner of Regent Court’. As David Pang considers that the roof is not a flat, the Incorporated Owner of Regent Court is not the owner and the fee is not directly paid to the owners of the flats, he believes that they should not be liable to property tax.

Required:

Advise David Pang whether the Inland Revenue Department is empowered under the Inland Revenue Ordinance to issue a 2010/11 property tax return in the name of ‘The Incorporated Owner of Regent Court’; and whether it is liable to property tax. (8 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

更多“SUPPLEMENTARY INSTRUCTIONS1. You should assume that the tax rates and allowances shown bel”相关的问题

更多“SUPPLEMENTARY INSTRUCTIONS1. You should assume that the tax rates and allowances shown bel”相关的问题

第1题

SUPPLEMENTARY INSTRUCTIONS

1. You should assume that the tax rates and allowances shown below will continue to apply for the foreseeable future.

2. Calculations and workings should be rounded down to the nearest HK$.

3. Apportionments need only be made to the nearest month, unless the law and prevailing practice require otherwise.

4. All workings should be shown.

TAX RATES AND ALLOWANCES

The following 2010/11 tax rates and allowances are to be used in answering the questions.

1.

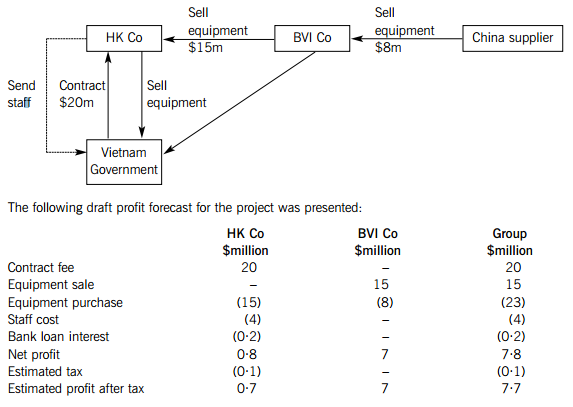

HK Engineering Co Ltd (HK Co), a Hong Kong-incorporated company carrying on business in Hong Kong, was successfully awarded a contract in Vietnam to help the Vietnam government with a new water plant project. A meeting has been scheduled with the Vietnam government’s representatives to discuss the details of the main contract. Prior to the meeting, the project manager, Mr Man, called for a meeting with other senior management staff, the details of which are as minuted below. All amounts are in HK$.

Minutes of Meeting on 1 June 2010 on Project Victory

Attendance:

Man (Project Manager)

FF (Finance Director)

TT (Treasurer)

EE (Chief Engineer)

1. Man briefly explained the scope of the work as required, including:

(a) the contract comprises two elements: supply of heavy equipment and the installation of the equipment on site;

(b) the total contract value is equivalent to $20 million covering both elements; and

(c) the duration of the project is estimated to be six months.

2. EE suggested that the equipment be purchased from one of their existing suppliers in Mainland China. Due to their long established relationship with this supplier, EE has confidence in negotiating the best terms and deal, with all the purchase orders and shipping documentation being dealt with directly in Hong Kong. The purchase cost is estimated to be around $8 million.

However, for the installation services, apart from employing local Vietnamese workers to perform. the on-site work, EE would need to send a team of experienced engineers from Hong Kong to Vietnam to supervise the work. As a result, the total staff costs for the project are estimated to be $4 million.

3. TT suggested that the $8 million purchase cost of the equipment be funded by the company’s current bank loan facility with interest at the rate of 5% per annum.

4. FF proposed the following structure using another member of the HK Co group, incorporated in the British Virgin Islands, BVI Co, in order to maximise the after-tax profit of the group:

5. Man appreciated the proposal explained by FF but questioned whether the structure would be challenged by the Inland Revenue Department as tax avoidance. Moreover, he is considering establishing a local subsidiary in Vietnam to sign the contract, as a start-up to expand HK Co’s business into the Vietnam market. FF agreed to solicit professional tax opinion on these aspects.

Required:

As the tax advisor of HK Engineering Co Ltd (HK Co), prepare a report for Mr Man addressing the tax issues set out below, including supporting calculations where appropriate.

(a) Assuming that a Vietnam subsidiary, wholly owned by HK Co, is established, the contract is to be signed by the Vietnam subsidiary and the equipment and staff are supplied by HK Co as outlined in point 2 of the minutes, advise on:

(i) The Hong Kong profits tax implications for HK Co with respect to the profits arising from the contract, together with any other matters on which you would recommend HK Co to obtain further advice; (4 marks)

(ii) How the supply of the equipment and staff should be dealt with in view of the current transfer pricing practice in Hong Kong. (8 marks)

Note: You are NOT required to comment on the Hong Kong-Vietnam tax treaty.

(b) Assuming that no Vietnam subsidiary is set up, and the structure proposed by the Finance Director (FF) as outlined in point 4 of the minutes is adopted, advise on:

(i) The Hong Kong profits tax implications for HK Co arising from the contract. You should specifically consider both the taxability of the contract value of $20 million, and the deductibility of the equipment purchase cost, staff costs and loan interest; (17 marks)

(ii) What the Hong Kong profits tax implications will be for BVI Co arising from the sale of the equipment to HK Co. (9 marks)

Professional marks will be awarded in question 1 for the appropriateness of the format and presentation of the report and the effectiveness with which its advice is communicated. (2 marks)

2.

Mr and Mrs Kwok are a married couple with no children. Mr Kwok has been working for a Hong Kong-listed company (the Company) since 1 August 2002. He had the intention to resign on 1 August 2010 but the Company had requested that he stay on for one more year. In recognition of his agreement to stay, the Company agreed to pay him an extra incentive of $50,000 on 1 August 2011. As the time is approaching, Mr Kwok is seeking professional tax advice on his tax position if he resigns effective from 1 August 2011 based on the following information:

Upon ceasing employment on 1 August 2011, Mr Kwok expects to receive the following final payments:

(1) A lump sum incentive payment of $50,000, as agreed in 2010, for Mr Kwok’s agreeing to extend his services for one year.

(2) An estimated amount of $100,000 representing his bonus entitlement in respect of the financial year 2011. This amount is estimated based on last year’s payment. The final figure will only be available in April 2012. Should the final figure exceed the payment of $100,000, the top-up will be paid to him in mid-April 2012. The Company has agreed that if the final figure is lower than $100,000 he will not be asked to pay anything back.

(3) Payment for leave not taken amounting to $20,000, including some leave days brought forward from 2010.

(4) Retirement benefit calculated in accordance with the rules governing the Company’s retirement plan which is duly registered under the Occupational Retirement Schemes Ordinance. Mr Kwok has met with the Company’s personnel manager, and he was asked to make a choice amongst the following options:

(i) leaving the Company by way of resignation (i.e. termination of service) and withdrawing his ‘leaving service benefit’ in the lump sum of $1,000,000;

(ii) leaving the Company by way of early retirement (subject to his supervisor’s consent) and withdrawing his ‘retirement benefit’ in the lump sum of $1,000,000 (same as the ‘leaving service benefit’ under (i) above);

(iii) leaving the Company by way of early retirement (subject to his supervisor’s consent) and withdrawing his ‘retirement benefit’ as a periodic pension in the amount of $10,000 per month commencing 1 August 2011 until his death.

Following his retirement, Mr Kwok will continue to serve the Company in the capacity of an independent consultant for a tenure of two years under the following terms:

(5) Mr Kwok will be obliged to provide services as and when required by the Company at an hourly rate of $1,000; but will be given advance notice of not less than 24 hours.

(6) Mr and Mrs Kwok are allowed to continue to occupy the Company’s staff quarters, subject to him continuing to pay the same rental contribution of $5,000 per month (see (10) below).

(7) At the expiry of the tenure, subject to the Company’s satisfaction with Mr Kwok’s service, Mr Kwok may be entitled to a gratuity of $10,000. Mr Kwok has also provided the following additional information:

(8) His annual taxable income reported in the tax return for the year of assessment 2010/11 is $1,000,000. He understands that when he is demanded to pay tax on his income for 2010/11, he will also be required to pay the provisional tax for 2011/12 based on the full-year income for 2010/11. He is concerned about the additional cash burden in meeting the provisional tax liability after ceasing employment.

(9) His monthly salary is $80,000 but he only receives $76,000 each month after deducting 5% as his contribution to the Company’s retirement plan. He understands that the Company is also obliged to contribute the same amount into the plan.

(10) He and his wife have been living in the Company’s quarter since August 2002. A monthly rental contribution of $5,000 has been deducted from his salary. The market rental of the quarter is $8,000 per month. Mr Kwok understands that he has been paying tax on this housing benefit but he has no idea about how the taxable value is calculated.

(11) His annual bonus for the financial year 2010 in the amount of $100,000 was received in April 2011.

(12) Mrs Kwok owns a property in Hong Kong and has been leasing it out for a monthly rental of $6,000. The property is still under mortgage and the monthly mortgage payment is $3,000, including $1,000 as interest. For tax reporting purposes, Mrs Kwok has each year declared the rental income of $3,000 per month and paid property tax thereon.

Required:

As his tax consultant, write a letter to Mr Kwok giving advice on the following:

(a) The general principles for determining the taxability of each item of final payment received by Mr Kwok upon his cessation of employment on 1 August 2011, assuming that he leaves the Company’s employment by way of resignation; that is, he chooses option (4)(i) above.

Note: You are NOT required to calculate the assessable/chargeable income or tax payable. (11 marks)

(b) The tax consequences, if any, to Mr Kwok if he chooses to leave the Company’s employment by way of retirement; and in this respect, whether his tax position would be different under the options of (4)(ii) and (4)(iii) above.

Note: You are NOT required to calculate the assessable/chargeable income or tax payable. (5 marks)

(c) The estimated tax positions of Mr and Mrs Kwok for the year of assessment 2011/12, and future years if applicable, based on the information available, together with any suggested actions available for Mr and Mrs Kwok’s consideration to help ease the cash burden required to meet their provisional tax liability for 2011/12 and/or improve their overall tax position in future years.

Notes:

(1) You should support your advice with calculations of assessable/chargeable income in so far as the information provided permits but are NOT required to calculate the tax payable.

(2) You should assume that Mr Kwok will keep 31 March as the ending date of his basis period. (12 marks)

Professional marks will be awarded in question 2 for the appropriateness of the format and presentation of the letter and the effectiveness with which its advice is communicated. (2 marks)

Section B – TWO questions ONLY to be attempted

3.

John Yuan is a PRC citizen working in the PRC. His brother, Peter Yuan, is a tax resident living and working in Hong Kong as a registered stockbroker under Part VI of the Securities Ordinance. Since 2008, Peter has been engaged in buying and selling shares listed in both Hong Kong and the US via internet banking. The share-trading is operated through two securities accounts, one in the name of Peter Yuan and the other in the name of John Yuan. Peter usually receives instructions or guidance from John through emails or telephone calls with regard to the identities of shares to buy or sell, the acceptable price range, the period of holding etc. However, at critical moments, he will exercise his discretion to maximise his brother’s interests or minimise his loss. Peter regularly collects updated market news and analysts’ reports and sends them to John. At the end of each month, Peter prepares a transaction summary for John showing the details of the transactions done on John’s account during the month. The average size of John’s portfolio per annum is around $20 million, and the average holding period for the shares is between 10 and 30 days. Since 2008, John’s portfolio has made a profit of around $2 million.

Required:

(a) Discuss whether or not John Yuan is liable to Hong Kong tax in respect of the profits arising from the trading of shares listed in Hong Kong and the US.

Note:

(1) For this part only, you are NOT required to discuss court case decisions in detail. Where applicable, only Departmental Interpretation and Practice Notes issued by the Inland Revenue Department should be relied upon.

(2) You are NOT required to examine in detail the impact of electronic commerce on the determination of source of profits. (10 marks)

(b) Assuming that Hong Kong tax is payable by John Yuan, advise whether the Inland Revenue Department can collect tax from Peter Yuan on behalf of John Yuan, and whether Peter Yuan is protected by the Inland Revenue Ordinance from any claims by John Yuan in respect of any tax paid on his behalf. (5 marks)

4.

(a) ‘It is a fundamental principle that stamp duty is charged on instruments, not on transactions.’

Required:

Comment on the effect of this statement, outlining the ways in which Hong Kong law ensures that certain transactions must be evidenced by a document in writing and giving a concrete example of how this principle can be used to avoid liability to Hong Kong stamp duty. (4 marks)

(b) The management of Tai Cheong Ltd (TCL) is considering acquiring all of the shares in Sun Cheong Ltd (SCL) for $500,000, which is the fair market value of these shares. SCL is a business competitor of TCL that is in financial difficulties; and has a substantial tax loss brought forward. Upon obtaining control of SCL, TCL will transfer part of its profitable retail business to TCL. SCL will then lease TCL’s retail shop in Mongkok from TCL. The term of the lease will be for six years and, under the lease agreement, SCL will pay 1% of the gross revenue from its retail business to TCL as the lease rental, subject to a maximum of $800,000 per annum. The gross revenue from the retail business is expected to be around $9 million per annum for the next few years.

Required:

(i) State the general rules governing the treatment of tax losses for corporations in Hong Kong; (3 marks)

(ii) Advise on the profits tax implications and stamp duty implications for Tai Cheong Ltd and Sun Cheong Ltd if Tai Cheong Ltd decides to acquire the shares of Sun Cheong Ltd and to lease the retail shop to Sun Cheong Ltd. (8 marks)

5.

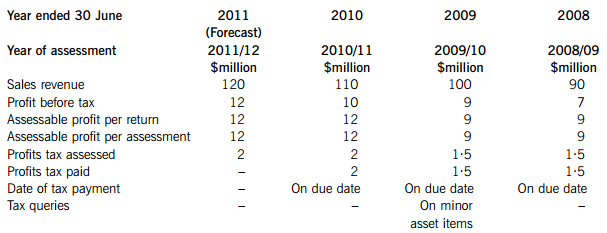

Buying Co Ltd (Buying Co) is interested in acquiring all the shares in Selling Co Ltd (Selling Co) from its current shareholder, Mr Shum. The consideration will be based on Selling Co’s financial position as at 30 June 2011. In the course of conducting the tax due diligence on Selling Co, the finance director of Buying Co obtained the following extracted information:

In drafting the share sale and purchase agreement, the lawyer of Buying Co requested a tax indemnity from Mr Shum to the effect that, after the shareholding change, any extra tax cost suffered by Selling Co in relation to any transactions or events that occurred prior to the shareholding change would be indemnified by Mr Shum. However, this was not agreed to by Mr Shum’s lawyer. Instead, Mr Shum sent a letter to Buying Co advising that he guaranteed that all tax assessments have been finalised and Selling Co has no outstanding tax disputes with the Inland Revenue Department (IRD); and in case any tax queries were raised by the IRD in respect of the years prior to the shareholding change, he was prepared to take full responsibility to deal with the disputes with the IRD on behalf of Selling Co.

Required:

Advise the directors of Buying Co Ltd on any potential tax risks that may be faced by Buying Co Ltd in respect of the acquisition of Selling Co Ltd in terms of tax compliance and whether the guarantee letter from Mr Shum is sufficient and effective to protect Buying Co Ltd in the event of a tax challenge being raised for any prior year.

请帮忙给出每个问题的正确答案和分析,谢谢!

第2题

he new premises in the

year ending 31 March 2009 and explain, using illustrative calculations, how any additional recoverable input

tax will be calculated in future years. (5 marks)

第3题

h the maximum

possible investment, borrowing to finance the subscription and the implications of selling the shares.

(7 marks)

Note: you should assume that Vostok Ltd and its trade qualify for the purposes of the enterprise investment

scheme and you are not required to list the conditions that need to be satisfied by the company, its

shares or its business activities.

第4题

invest in his company,

Vostok Ltd. He also requires advice on the recoverability of input tax relating to the purchase of new premises.

The following information has been obtained from a meeting with Gagarin.

Vostok Ltd:

– An unquoted UK resident company.

– Gagarin owns 100% of the company’s ordinary share capital.

– Has 18 employees.

– Provides computer based services to commercial companies.

– Requires additional funds to finance its expansion.

Funds required by Vostok Ltd:

– Vostok Ltd needs to raise £420,000.

– Vostok Ltd will issue 20,000 shares at £21 per share on 31 August 2008.

– The new shareholder(s) will own 40% of the company.

– Part of the money raised will contribute towards the purchase of new premises for use by Vostok Ltd.

Gagarin’s initial thoughts:

– The minimum investment will be 5,000 shares and payment will be made in full on subscription.

– Gagarin has a number of wealthy business contacts who may be interested in investing.

– Gagarin has heard that it may be possible to obtain tax relief for up to 60% of the investment via the enterprise

investment scheme.

Wealthy business contacts:

– Are all UK resident higher rate taxpayers.

– May wish to borrow the funds to invest in Vostok Ltd if there is a tax incentive to do so.

New premises:

– Will cost £446,500 including value added tax (VAT).

– Will be used in connection with all aspects of Vostok Ltd’s business.

– Will be sold for £600,000 plus VAT in six years time.

– Vostok Ltd will waive the VAT exemption on the sale of the building.

The VAT position of Vostok Ltd:

– In the year ending 31 March 2009, 28% of Vostok Ltd’s supplies will be exempt for the purposes of VAT.

– This percentage is expected to reduce over the next few years.

– Irrecoverable input tax due to the company’s partially exempt status exceeds the de minimis limits.

Required:

(a) Prepare notes for Gagarin to use when speaking to potential investors. The notes should include:

(i) The tax incentives immediately available in respect of the amount invested in shares issued in

accordance with the enterprise investment scheme; (5 marks)

第5题

e UK without

giving rise to a UK income tax liability. (2 marks)

第6题

nd/or provide him with

interest-free loan finance for this purpose without increasing his UK income tax liability; (3 marks)

第7题

ale of the paintings

can be minimised. (2 marks)

第8题

the instalments are

due and identify any further issues relevant to Galileo relating to the payments. (3 marks)

第9题

tax that will be suffered

on both the distributed and non-distributed profits of the non-UK resident investee companies where:

(1) there is a double tax treaty between the UK and the country in which the individual companies are

resident; and

(2) there is no such double tax treaty.

Note: you are not required to explain the position of the overseas resident branches. (6 marks)

第10题

tal treatment to

apply to the transaction. (4 marks)

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!