重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

Which of the following is most likely a benefit of debt covenants for the borrower?

A.Reduction in the cost of borrowing.

B.Limitations on the company’s ability to pay dividends.

C.Restrictions on how the borrowed money may be invested.

更多“Which of the following is most likely a benefit of debt covenants for the borrower?A.”相关的问题

更多“Which of the following is most likely a benefit of debt covenants for the borrower?A.”相关的问题

第1题

ir value of the leased equipment at inception of the lease is $10,000 and the implicit interest rate is 12 percent.If the present value of the lease payments equals the fair value of the equipment at the inception of the lease, the interest expense (in $) recorded by the lessee in the second year of the lease is closest to:

A.960.

B.1,104.

C.1,200.

第2题

se terms and lower cost financing to a lessee? Because the:

A.Lessor retains the tax benefits of ownership.

B.Lessor avoids reporting the liability on its balance sheet.

C.Lessee is better able to resell the asset at the end of the lease.

第3题

A retail company that leases the majority of its space has:

·total assets of $4,500 million,

·total long-term debt of $2,125 million, and

·average interest rate on debt of 12%.

Note 8 to the 2011 financial statements contains the following information about the company’s future beginning of year lease commitments:

Note 8: Operating leases

After adjustment for the off-balance-sheet financing, the debt-to-total-assets ratio for the company is closest to:

A. 55%.

B. 57%.

C. 65%.

第4题

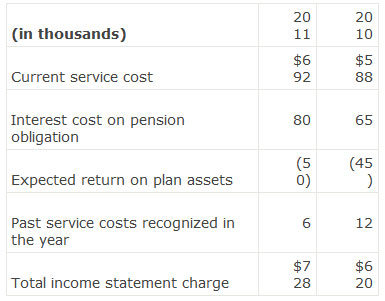

The following information is available from a company’s 2011 financial statements:

Note 6: Employee costs

Note 17: Retirement benefit obligations

Amounts recognized in the income statement for the year

The pension expense (in thousands) reported in 2011 is closest to:

A. $1,525.

B. $2,217.

C. $2,253.

第5题

r the same amount of convertible debt with a 5% coupon rate. Both will be issued at par and have the same maturity. Which statement below best describes the impact on the firm’s debt ratio?

A. The debt ratio would be higher for U.S.GAAP than for IFRS.

B. The debt ratio would be lower for U.S.GAAP than for IFRS.

C. The debt ratio would be the for U.S.GAAP than for IFRS.

第6题

uent financial statements will include a:

A. An increase in tax expense and an increase to the debt-to-equity ratio.

B. An increase in tax expense and a decrease to the debt-to-equity ratio.

C. A decrease in tax expense and an increase to the debt-to-equity ratio.

第7题

c life of 10 years. The company also leases them directly to construction companies with good credit. If Construction Group (CG) leases the equipment from BP, the relevant interest rate is 10% and the lease payments will be $4,000 per month for four years. CG has purchased equipment in the past by financing through Prime Finance. Assuming that CG decides to lease the equipment, BP should treat the lease as a(n):

A. Direct financing lease.

B. Operating lease.

C. Sales-type lease.

第8题

finance lease rather than as an operating lease will be:

A. Unchanged total lease expense over the lease term.

B. Lower operating cash flows during the life of the finance lease.

C. Lower operating profit (margin) in the early years of the finance lease.

第9题

s of $20,541. The present value of the lease liability is approximately $100,000 based on a 10% discount rate. The interest portion of the first payment is closest to:

A. $10,000.

B. $13,340.

C. $14,200.

第10题

year and also has significant number of operating leases. Which of the following statement is the least accurate?

A. The company’s financial statements must be adjusted before the analyst compares this company to other companies in its industry.

B. Despite the off-balance sheet nature of take-or-pay contracts and operating leases, an attempt to determine the actual financial position of the company can be garnered from the footnotes.

C. The take-or-pay contracts and operating leases mean that this company has much higher business risk than similar companies that do not use off-balance sheet financing techniques.

客服

客服

TOP

TOP

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“上学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!